Investment Summary

Q1 Records Outstanding Performance, a Substantial Growth of over 50%

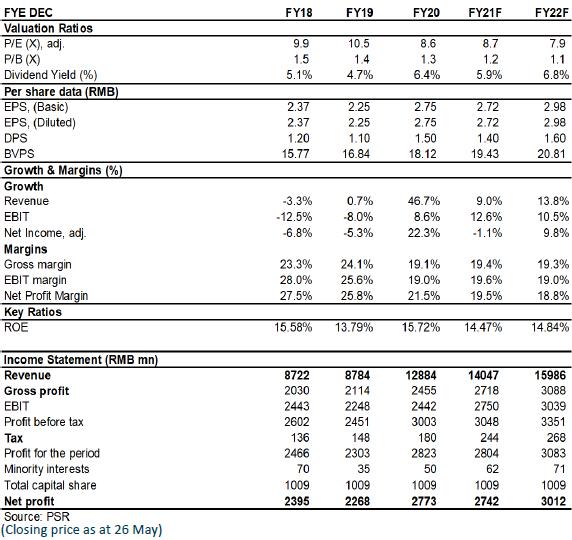

In the first quarter of 2021, Weifu High-Technology Group Co., Ltd. reported a revenue of RMB4.7 billion, up by 69.6% yoy; the net profit attributable to the parent company was RMB862 million, up by 56.7% yoy; the net profit attributable to the parent company excluding non-recurring items was RMB930 million, up by 88% yoy. The quarterly revenue and the net profit from deduction both hit a new high. The outstanding performance was mainly attributable to the continuation of high prosperity in the commercial vehicle market and the low base caused by the pandemic over the same period last year. According to the data of China Association of Automobile Manufacturers, the sales volume of domestic passenger vehicles and heavy trucks in the first quarter of 2020 rose sharply by 76.6% and 93.9% yoy, respectively, which drove its associated companies Bosch Automotive Diesel Systems Co., Ltd. and Zhonglian Electronics Factory Co., Ltd. to record strong growth, thereby contributing RMB510 million in investment returns, up by 70.2% yoy.

Gross Margin Declines Slightly and Expenses Are Well Controlled

The gross margin during the period was 17.98%, down by 0.83 ppts yoy and down by 4.7 ppts mom. The main reason was the increased proportion of post-processing business revenue with a low gross margin and the rising cost due to rising raw material prices. The Company performed well in cost control. The period expense ratio was 6.7%, down by 2.1 ppts yoy and down by 16.5 ppts mom, and the sales, administration and R&D expense ratio was down by 0.6pct, 1.7pct and 0.2 ppts yoy, respectively. The Company had a strong balance sheet. The proportion of interest-bearing debts in the total invested capital was only 3.73%. Besides, the Company had sufficient funds, with RMB10.62 billion of cash, cash equivalents and other current assets in the first quarter, an increase of 3.3% compared with the end of 2020.

Share Incentive Plan Demonstrates the Company's Confidence and Facilitates Long-term Development

Last October, the Company issued the draft share incentive plan, with an intention to grant 19,596,000 restricted shares to 602 incentive objects, accounting for approximately 1.942% of the Company's total shares at the time when the draft plan was announced. The grant price was RMB15.48 per share, which was about a 35% discount to the latest closing price, indicative of a significant incentive effect. It was required by the unlocking conditions that the proprietary profit for 2021 to 2023 should not be less than RMB845 million, RMB892 million and RMB958 million, respectively, the return on net assets for 2021 to 2023 should not be lower than 10%, and the cash dividend should not be lower than 50% of the profit available for dividend the same year. We believe that the announcement of this share incentive plan reflects the confidence of the management in the future development prospects of our proprietary business and improved business visibility. This move is also conducive to uniting the Company's management and core technical personnel, binding interest, stimulating business vitality, further consolidating industry competitiveness, and laying a foundation for the Company's long-range development.

Emission Standard Upgrade in H2 to Raise Profitability, New Business Landscape to Bring New Growth Momentum

The upgraded China VI vehicle emission standards will be comprehensively implemented from July 1, 2021, and off-road diesel machinery is expected to implement the China IV vehicle emission standards from the end of 2022. At present, the phaseout of diesel vehicles with the China IV vehicle emission standards is encouraged in some cities. "Carbon peaking" will push the internal combustion engine industry to upgrade key and core technologies in energy conservation and emission reduction and will benefit leading manufacturers of diesel engine core parts like Weifu High-Technology, which can expect raised profitability.

For the past few years, the Company has launched new businesses with hydrogen fuel cell and intelligent network as two main strategic directions through active epitaxial M&As, to build the core competitiveness of sustainable development. So far, the two new businesses have both achieved rapid growth. The Company's smart seats have won projects from some mainstream vehicle enterprises and entered the phase of small-batch supply. In 2020, the Company recorded a sales revenue of RMB77,397,000 in the core components of hydrogen fuel cells..

Valuation

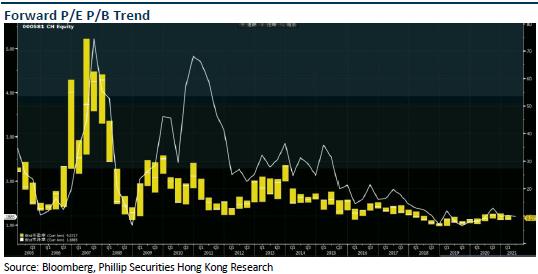

The company holds abundant cash flow and wealth management plans, with stable operation style, providing a foundation for the future merger and acquisition transformation and high dividend. As analyzed above, we expected diluted EPS of the Company to RMB 2.72 and 2.98 for 2021/2022. And we accordingly gave the target price to 27.3, respectively 10/9.1x P/E 1.4/1.3 x P/B for 2021/2022. "Accumulate" rating. (Closing price as at 26 May)

Financials

Click Here for PDF format...