Investment Summary

Results in 21Q1 Soar Again, up 289%

Benefiting from the continuation of the industry's high boom and the launch of new production lines, Flat Glass recorded operating revenue of RMB2,057 million in the first quarter of 2021, up by 70.95%yoy. The net profit attributable to the parent company was RMB838 million, up by 289.38% yoy and up by 2.6% qoq, hitting new record high again.

Profitability Indices Hit New High

In the first quarter, the price of photovoltaic glass remained in a high range between RMB40 and RMB32 per square meter, which was approximately RMB11 to RMB14 higher than the same period in previous years. It is a prerequisite for photovoltaic glass manufacturers to maintain high profitability. In terms of product mix, the proportion of thin glass with high gross margin increased to over 30% by 19 ppts yoy. The continued optimization of the product mix increased the gross margin. The Company recorded a 58.2% gross margin in the first quarter, an increase of 18.4 ppts yoy, and a slightly decrease of 0.3 ppts qoq.

The Company displayed good performance in period expense ratio. The sales, administrative, R&D and financial expense ratios changed by -1.5 ppts, +0.7 ppts, +0.9 ppts, and -2.1 ppts, respectively. The administrative expenses increased, mainly due to the rise in share incentives and employee salaries. The R&D expenses climbed mainly because of more R&D projects. The main reason for the decrease in financial expenses was the decrease in interest expenses and the growth in exchange gains.

The final net profit margin was 40.74%, up by 22.9 ppts yoy and up by 4.33 ppts qoq. The profitability indices all hit record highs. After the completion of the RMB2.5 billion A-share private placement, the Company's balance sheet has become strong. Meanwhile, the Company increased the reserves and inventories of some raw materials to prepare for future fluctuations.

Cost Advantages Will Be Prominent as the Price of Photovoltaic Glass Falls

In February, the Company announced proposed issuance of no more than 76 million H shares for replenishing working capital. This will help the Company further strengthen its asset structure.

On March 29, the Company announced that it would invest RMB5.8 billion to add six new production lines with production capacity of 1,200 tons per day (two production lines in Jiaxing + four production lines in Anhui). The production lines are expected to be put into production in 2022-2023. At the end of 2020, the Company's production capacity was approximately 6,400 tons per day. The current production capacity is 8,600 tons per day. By the end of this year, the production capacity is expected to reach 12,200 tons per day. After full production, the Company's total production capacity is expected to reach 19,400 tons per day, with its leading position more stabilized.

In terms of costs, the Company will construct a pipeline project of direct supply of natural gas with the terminal as the Anhui production line, to further strengthen its future control of costs and consolidate its cost advantages.

From the end of March to early April, with the rapid release of industry supply, the downstream gradually entered the off-season, and the demand growth rate slowed down. The Company took the initiative to significantly lower product prices by approximately 30%. It is expected to ease downstream cost pressures and increase demand. On the other hand, it will also help restrain the excessive expansion of the industry production capacity and optimize the industry supply. Benefiting from the advantages in technology, scale, capital and customers, the Company's cost advantages will become more prominent as market price falls. Its market share is expected to increase.

Investment Thesis

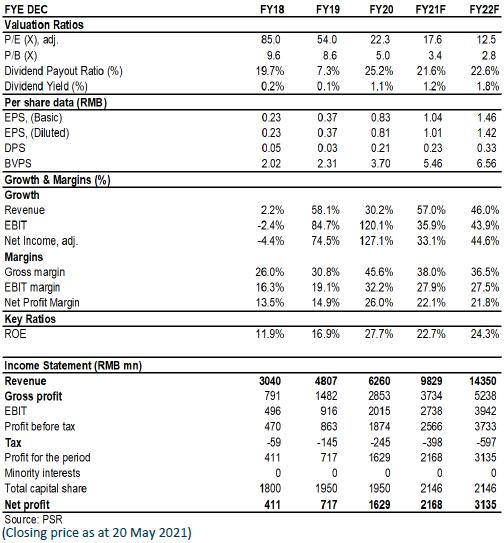

Despite the recent price drop, the photovoltaic industry remains enthusiasm in the long run. We are optimistic about the company's future expectations. Taking into account the market price adjustment and the construction of new production capacity, we adjusted our profit forecast and adjusted the target price to HK$ 33, equivalent to 2021/2022 E 26.3/18.8x P/E and 12.5/9/6.8x P/B, BUY rating. (Closing price as at 20 May 2021)

Financials

Click Here for PDF format...