Investment Summary

FY20 Results Significantly Fall Short of Expectations and Profitability Is under Pressure

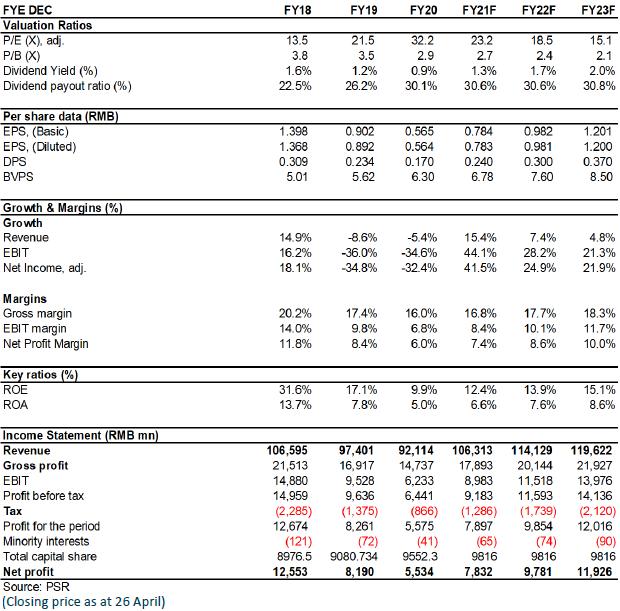

Geely's total revenue in 2020 fell to RMB92.11 billion, down by 5% Y-o-Y. The profit attributable to shareholders was RMB5.53 billion, down by 32% Y-o-Y. The gross margin was 16%, down by 1.4 ppts over the same period last year. The EPS was RMB0.56. The DPS was proposed to be HK$0.20, with a dividend payout ratio of approximately 30%.

The results significantly fell short of market /our expectations by approximately 23% and 26%, respectively. The main reasons include not only 1) the COVID-19 pandemic, but also 2) the increase in depreciation and amortization expense ratio due to the overall decline in sales volume, 3) the gross profit margin being eroded by the rising costs of some raw materials, 4) the price-off promotion as some old models are approaching the end of their lifecycle, and 5) large investment of R&D expenses and sales and administration expenses in the new car cycle of the 4.0 era. As a result, the Company's annual gross margin was 1.2 ppts lower than our expectation, while the sales and administration expense ratio was 1.5 ppts higher than we expected. Finally, the profitability was under pressure. The net profit margin dropped by 2.4 ppts to 6.0%, hitting a low since the Company's overall listing.

In 2020, Geely sold 1,320,200 units accumulatively, down by 3% Y-o-Y. From a regional perspective, the Chinese market contributed 94.5% of sales volume, with a total of 1,247,500 units, down by 4% Y-o-Y. The Chinese market contributed RMB85,597 million in sales revenue, down by 7.6% Y-o-Y. On the other hand, overseas markets have achieved positive returns after several years of cultivation. Last year, 73,000 units were sold accumulatively, up by 25% Y-o-Y. Overseas markets contributed RMB6,517 million in revenue, up by 37% Y-o-Y. However, the overall proportion remained small, which was less than 10%.

For the overall sales volume, the brand LYNK&CO has become a bright spot. It sold 175,000 units accumulatively throughout the year, up by approximately 37% Y-o-Y. It contributed RMB260 million to investment return; in addition, Genius Auto Finance Co., Ltd. contributed RMB580 million to return, driving the Company's investment return to a substantial increase by 32 % to RMB875 million, which partially offset the adverse effects.

Operating cash flow was under pressure in H1, mainly due to the financial support for suppliers to extend the billing period during the pandemic. As the billing period returned to normal in H2, the operating cash flow was turned from negative to positive. The Company recorded a net inflow of RMB1.6 billion in the year. The cash balance at the end of the reporting period was RMB19 billion. The Company had abundant cash in hand, laying a solid foundation for the next stage of development.

Looking Forward to Bailing the Results out of Slump Driven by New Brand and New vehicle-Cycle

At present, Geely has developed four basic modular architectures of BMA, CMA, SPA, and SEA. Its products cover pure electric, hybrid and fuel vehicles. In 2021, the Company will launch at least five new models: Xingyue L, a new generation of Emgrand, the first model based on the SPA architecture of LYNK&CO, a new model of the brand Geometry, and the first model based on the SEA structure of the brand Zeekr.

On the new energy vehicle track, as the Blue Geely Action Plan II, Geely launched the 001, the first model of the brand-new pure electric vehicle sub-brand Zeekr, at the 2021 Auto Shanghai, empowering the high-end intelligent pure electric vehicles. Judging from the latest orders, the pre-sales of new models were hot due to its advantages in technology configuration, space, interior, appearance, power system, and endurance mileage.

We believe that the successive launch of the models of new architecture (SEA and SPA), new brand (Zeekr) and new cycle (4.0 era) on the market will help the Company change the current situation of tepid sales volume of new energy vehicles, make up for the shortcomings in new energy models and increase brand premiums. The year 2021 will be the first year for Geely's technological upgrade and the development of intelligent electric vehicles. The improvement in results is anticipating.

Investment Thesis

We believe that the current domestic auto market is starting a new round of recovery cycle, and the wave of vehicle intelligence and global vehicle electrification led by consumption upgrades is in the ascendant. All of these will provide support for the Company's new level of development. In addition, Geely's plan to return to the STAR Market to raise RMB20 billion was approved recently. The merger negotiations with Volvo are expected to restart. The equity design of Zeekr also maintains flexibility for the future introduction of strategic investors/seeking overseas listings. The integration and synergy at the capital level are worth anticipating, which may become a valuation catalyst.

We revised our target price to HK$26, equivalent to 28/22/18x P/E ratio in 2021/2022/2023, and we give the rating of Buy. (Closing price as at 26 April)

Financials

Click Here for PDF format...