Investment Summary

FY20 Profit Decreases by 10% yoy, Mainly Due to Impairment

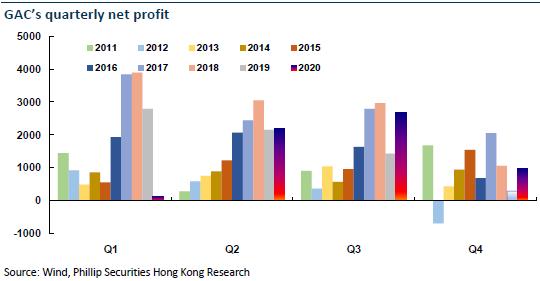

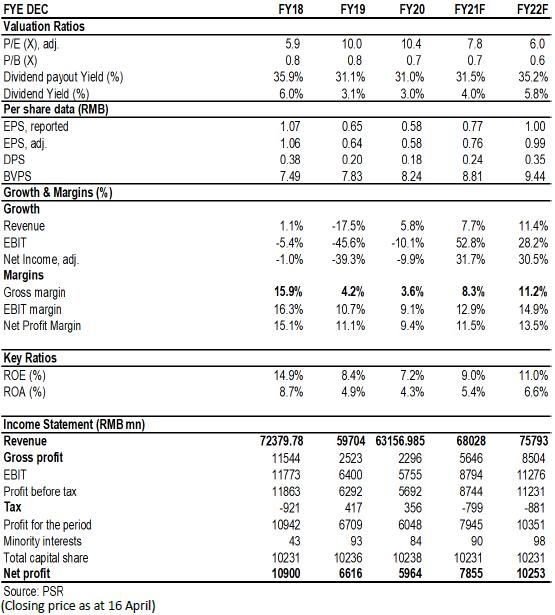

In 2020, GAC recorded operating revenue of RMB63,157 million, up by 5.78% Y-o-Y; net profit attributable to the parent company was RMB5,966 million, down by 9.85% Y-o-Y; in addition to the impact of COVID-19 pandemic, the decline in results was mainly due to the large accrued expenses in the fourth quarter (provision for asset impairment of RMB720 million in a lump sum). After deducting non-recurring gains and losses, net profit attributable to the parent company was RMB4,807 million, up by 25.17% Y-o-Y. Self-owned brands achieved loss reduction. After deducting non-recurring gains and losses and return on investment, net loss attributable to the parent company was RMB5.1 billion, down by 12% Y-o-Y. EPS was RMB0.58, down by 11% Y-o-Y. The final dividend was RMB0.15 per share. Combined with the interim dividend of RMB 0.03 per share, the dividend payout ratio was 31%.

Gross margin decreased by 0.38 ppts Y-o-Y, mainly due to the negative effect of scale caused by the decline in sales volume of self-owned brands. The period expense ratio for the whole year decreased by 2.1 ppts Y-o-Y, mainly because the sales expense ratio fell by 1.86 ppts, and other expense ratios remained flat Y-o-Y. The R&D expenses totaled RMB5.1 billion, of which 17% was expensed. Joint ventures had a good profitability. The annual return on investment was RMB9,911 million, up by 2.96% Y-o-Y. Specifically, the return on investment in associates and joint ventures was RMB9,571 million, up by 1.83% Y-o-Y. At the end of 2020, monetary funds were RMB28.5 billion and interest-bearing liabilities were RMB14.8 billion.

Japanese JVs Remain Strong Momentum While Self-owned Brands Make Continuous Improvement

In 2020, China's automobile market demonstrated a fall-rise pattern, with an overall decline of 1.9%, which is narrower than the previous year. GAC outperformed the industry relying on its strong Japanese brands. It achieved an annual sales volume of 2,043,800 units, down by approximately 0.9% Y-o-Y. Its market share increased to 8.07%. Specifically, Honda and Toyota still remained a strong momentum of growth. GAC Honda sold 805,800 units, up by 2.65% Y-o-Y; GAC Toyota reported an annual sales volume of 765,000 units, up by 12.2% Y-o-Y, far higher than the industry average.

Among the best-selling models, the Accord and Camry ranked first and second in the middle and high-end sedan segment in terms of the terminal sales. Star models such as Levin, Vezel, Breeze, Trumpchi GS4, Yaris L, Crider, Highlander, Fit, Avancier, Aion S and Odyssey are among the best in their respective segment.

Compared with Honda and Toyota, the annual sales volume of GAC FCA and GAC Mitsubishi in the joint ventures witnessed sharp declines of different magnitudes. In 2020, GAC FCA sold 41,000 units, down by 45% Y-o-Y; GAC Mitsubishi sold 75,000 units, down by 44% Y-o-Y.

In terms of self-owned brands, GAC Trumpchi reported an annual sales volume of 354,000 units, down by 8% Y-o-Y. The rate of decline has narrowed significantly (-28.14% in 2019). GAC Trumpchi's theme for 2019 was to update products and actively reduce dealer inventory. We have noticed that since July last year, GAC Trumpchi has achieved positive growth in monthly sales volume for six consecutive months, and continued to maintain an improvement trend. In addition, breakthroughs were made in MPV models.

New Factory Project Is Advancing Steadily

At the end of 2020, the Company's total automobile production capacity was 2,733,000 units per year. GAC Toyota's new plant is expected to be put into production in July this year. By that time, GAC Toyota's design production capacity will be increased from the current 600,000 units to 800,000 units. GAC Honda's new plant is under construction. A production line of 120,000 units per year has been put into production in February last year. Another production line of 120,000 units per year is expected to be completed and put into production by the end of next year. By that time, GAC Hongda's design production capacity will reach approximately 900,000 units. The combined new production capacity of Honda and Toyota will increase by nearly 30% compared with the current production capacity, which will accumulate potential energy for the next stage of development.

In terms of new models, the models planned to be launched in 2021 include: GAC Trumpchi EMP0W55, GS4 medium redesign, GS8 new-gen, GA4 medium redesign, GAC Aion Y, GAC Honda Accord medium redesign, Crider medium redesign, Breeze plug-in hybrid version, Odyssey hybrid version medium redesign, EA6, GAC Toyota Camry medium redesign, Highlander new-gen, C-HR medium redesign, PHEV, GAC FCA Jeep Commander PHEV, and GAC Mitsubishi pure electric A-class SUVLE. Specifically, new energy models are occupying an increasingly important share.

Investment Thesis

In the first quarter of 2021, GAC recorded a sales volume of 497,000 units, which was basically the same as in 2019. The sales volume of GAC Toyota, GAC Hongda and self-owned brands increased by 25% and decreased by 12% and 22%, respectively compared with that in 2019. In the first quarter, the sales volume of its new energy vehicles increased by 103% to 21,576 units Y-o-Y, of which 17,649 units were contributed by GAC Aion. As a high-end new energy sub-brand, GAC Aion will enter its first year of development in the true sense this year. In addition to accelerating the promotion of new iterations of products, GAC Aion will start to carry multiple important technological achievements such as sponge silicon negative plate battery technology, super fast charging battery technology, and ADiGO4.0 intelligent driving interconnected ecosystem in mass production vehicles. Its future performance is anticipating.

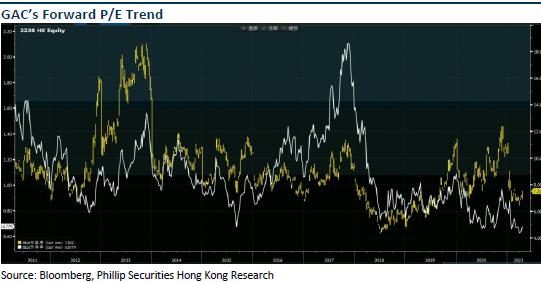

We revised the Company's 2021/2022 earnings forecast. We give the "Buy" rating with the target price to HKD 9.5, equivalent to 10.4/8.0x P/E and 0.9/0.8x P/B ratio in 2019/2020/2021. (Closing price as at 16 April)

Financials

Click Here for PDF format...