Investment Summary

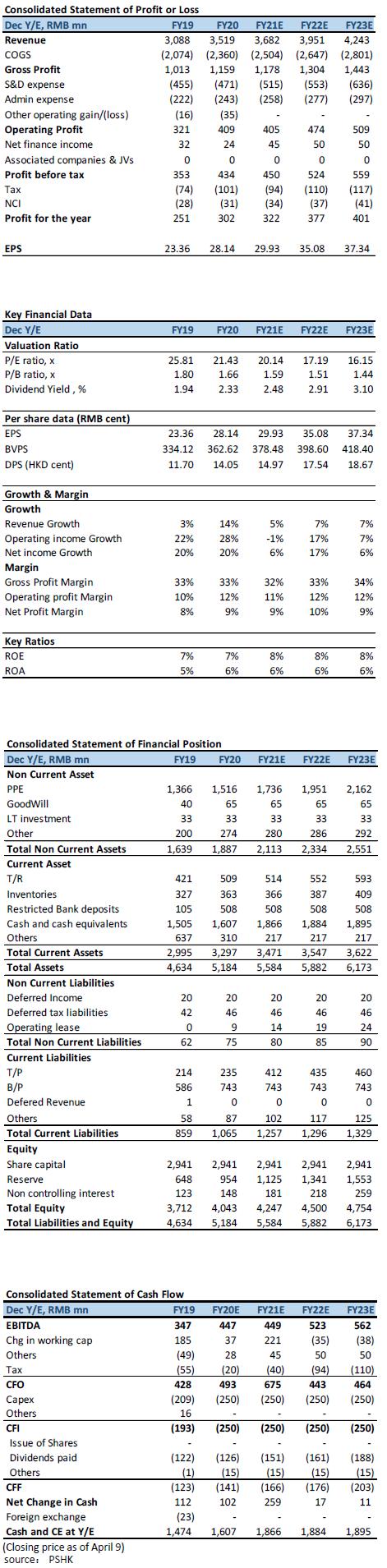

Nissin Foods announced its annual results for the year ended December 31, 2020 on March 18. The company's revenue in 2020 was HK$3.52 billion (2019: HK$3.09 billion), a year-on-year increase of 14.0%, in line with our expectation. The net profit was HK$302 million, a year-on-year increase of 20.3%, which is lower than expected, mainly because the company's GPM is lower than our expectation. The company's annual GPM is 32.9%, which is similar to last year's level (2019: 32.8%). The company's net profit margin was 8.6%, an increase of 0.5 ppts year-on-year. The company's EPS were 28.11 HK cents, an increase of 20.33% over the same period last year. The company declared a final dividend of 14.05 HK cents per share, with a dividend payout rate of 50%.

Regarding the source of income, the company's revenue from Hong Kong business was HK$1.42 billion, an increase of 9.1% year-on-year (2019: RMB 1.30 billion), accounting for 40.3% of the company's total revenue. This was mainly due to the epidemics last year. The demand for longer and easy to store products, such as instant noodles and frozen foods, has risen sharply. In the fourth quarter, with the relaxation of government policies, the growth rate also began to slow down significantly. In 20Q4, Hong Kong business revenue increased by 2.2% year-on-year, which was lower than the annual average. In 2020, revenue from China business recorded HK$2.1 billion, accounting for 59.7% of the company's full-year revenue. Revenue increased by 17.5% year-on-year compared to 2019. If calculated in RMB, it was 18.6%. The growth exceeded our expectations. Starting from 20Q2, the company The new joint-venture distribution business in Shanghai started operating and contributed to the group's revenue.

Business normalization in 2021 is expected, revenue growth to slow down under high base

With the proper prevention and control of the domestic epidemic, there is little chance that the Covid-19 will break out again. In addition, Hong Kong people's anxiety about the epidemic has eased, and there is little chance of large-scale food hoarding. It is expected that demand will return to normal level. With a high base in 2020, the expected growth rate will slow down, which will put pressure on the company's revenue growth. In addition, the company faces continuous increases in the prices of raw materials such as palm oil and flour. The company's current palm oil inventory is sufficient for the company to use until March. In the future, it may control costs by adjusting product portion and mass purchases to ease the pressure of rising costs.

Valuation model adjustment

In terms of the revenue model, we maintain our previous forecast of the company's revenue. Considering the high base in 2020, we expect that the company's business in Mainland China and Hong Kong will change to +7.7%/flat in 2021, respectively. Taking into account the increase in product raw material prices, we lowered the company's expected GPM in 2021 to 32% (previously 34%) to reflect the company's cost pressure, and the expected impact will ease in the next year. In addition, the company's sales-expense ratio has also been lowered due to lower distribution costs in Shanghai. The company's overall net profit in 2021/2022 was adjusted to 322 million / 377 million Hong Kong dollars.

Valuation and investment advice

Affected by the epidemic in 2020, the company's annual revenue performance was excellent, and its Hong Kong business revenue increased by 9.1% year-on-year. Under the current anti-epidemic control in Hong Kong, it is expected that in 2021, the company's business income in Hong Kong will return to a normal scale. The company has a large market share in the Hong Kong market and can maintain a certain level of income, but the company's income will grow Space is also limited. On the contrary, the company's main competitors in the industry are Uni-President Foods and Kangshi Chuan, etc., which is different from its main competitors in the domestic market, which have established a stable position in the domestic market. The future growth expectation is low. Nissin Foods is in its infancy in the country. At this stage, the domestic market share in China is low, and in an environment where domestic consumption levels are upgraded, the company has a competitive advantage in the high-end instant noodle market. In the past three years, the company's domestic revenue has recorded double-digit growth in RMB terms. Overall, we expect the company's revenue growth to slow in 2021. We expect that the company's FY21/FY22 net profit attributable to the parent will be HK$322/ HK$377 million, and FY21/FY22 EPS will be 29.93/35.08 HK cent. According to our DCF valuation model, the target price is adjusted from HKD 8.73 to HKD 7.54, which corresponds to the FY21/FY22 target market. Earnings ratio is 25.19x/21.49x, maintain Buy rating.

(Current price as of 9 April)

Key Financial

Click Here for PDF format...