Investment Summary

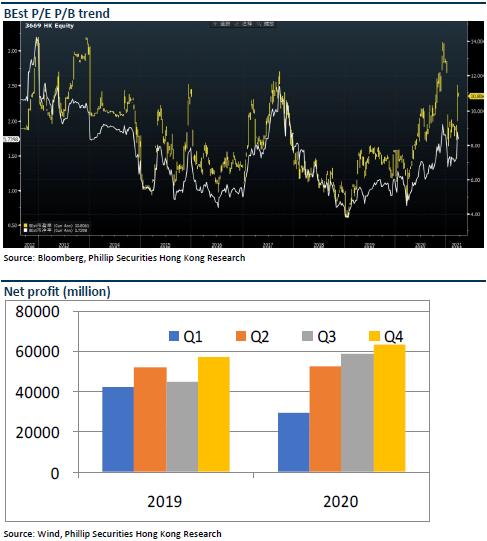

FY2020 Revenue Increased by 10% and Profit Continuously Increased by 50+% in 20Q4

The Company reported a revenue of RMB69.633 billion at a YoY growth rate of 9.1% in 2020. The gross margin was 9.29%, which was generally equivalent to that for 2019, and slightly reduced by 0.06 ppts. Net profit attributable to the parent company recorded RMB1.63 billion at a YoY growth rate of 10.3%, which generally met our previous expectation. Among these, the quarterly profit was, respectively, RMB60/470/480/620 million, at a respective YoY growth rate of -83%/+21%/+41%/54%. DPS was RMB0.288 at the dividend payout ratio of 35%. After-sale business contributed RMB4.376 billion to gross profit, grew 6.3% YoY, and made up 58.63% of total gross profit. New vehicle sales contributed RMB1.555 billion to gross profit, jumped 25% YoY, and made up a higher rate of 20.83% of total gross profit. The comprehensive gross profit margin generally remained the same and slightly reduced by 0.18 ppts YoY to 10.72%, for the main reason that the growth rate of new vehicle sales business with slightly lower margin was higher. The gross margin of new vehicle sales increased by 0.32 ppts YoY to 2.67%, and the gross margin of after-sale business slightly reduced by 0.36 ppts YoY to 46%.

The Proportion of Premium Car Further Increased

We hold that the profit in Q4 achieved new high because 1) there was strong demand for the Premium models (especially Porsche and BMW), 2) after-sale business steadily increased, and 3) the accumulative financing cost greatly dropped. In Q4, driven by the main brands, the gross profit of new car sales and after-sale grew at 32% and 18% yoy, respectively. BMW and Porsche's new vehicle sales revenue in 2020H2 increased at 18.4% and 29.9%, respectively, YoY to RMB14.33 billion and RMB5.084 billion. The contribution to gross profit respectively increased from 39.5%/38.3% in 2019 to 42.3%/41.6% in 2020. The growth rates of sales volume and ASP of Premium cars were higher than average, which helping the proportion of new car sales revenue/gross profit for Premium car increased by 1.3/2.5 ppts to 84%/98.7%.

Moreover, the Company conducted the placement financing of RMB980 million in the middle of the year, and optimized the debt structure. Net gear ratio in H2 reduced by 44.6 ppts YoY to 54.1%, and the financing cost reduced by 24.2% YoY/17.8% HoH to RMB305 million.

Operational Efficiency Was Continuously Improved

The Company continuously conducted an array of improvement measures that aimed to increase operational efficiency and speed up inventory turnover, and greatly increased inventory turnover efficiency through strengthening sales prediction, order matching management, shortening delivery period, and conducting refined assessment. The new car/parts turnover days reduced by 6.1 days YoY to 30.4/37.1 days. Operating cash flow was also significantly improved, and cash flow from operating activities increased by 39% YoY to RMB5.73 billion.

Network Structure Was Continuously Optimized

The Company continuously optimized the network structure, and endeavored to focus on luxury brand expansion. The Company added 20 authorized 4S shops in the year, including 13 self-built branches and 7 procured branches. The Company focused on key luxury brands, such as BMW/Porsche/Lexus, and increase the outlets of other luxury brands (Volvo/Aston Martin). Moreover, the Company also proactively cooperated with mainstream new-energy vehicle OEMs, such as Tesla/Weltmeister/Xpeng, explored new business mode, and closed 13 outdated outlets. As of the end of 2020, the Company operated 238 branches, including 25 unauthorized branches and 213 authorized branches, 7 more than that in 2019. Because the 7 new 4S shops were procured at year-end, it is expected that they will continue contributing to the operating results in 2021.

Pre-owned Cars and New Energy Vehicles Will Become Future Key Development Programs

Thanks to the gradually lax restrictive policy, domestic Pre-owned car market is expected to undergo a period of rapid development. Last year, the Pre-owned car transaction scale of the Company increased by 27% YoY to 52,280 vehicles. The gross profit increased by 27% YoY to RMB175 million. In the future, the Company will continue shifting the used car business in traditional agency mode to proprietary trading mode, and give play to the complementary and coordination effect of the dual channels featuring online & offline sales and new & pre-owned cars.

The Company took the lead to arrange business in new-energy vehicles, and sold 10,271 new-energy vehicles at a YoY growth rate of 14%. Except for new-energy vehicle business in traditional brands, the Company also sped up the arrangement in emerging mainstream new-energy vehicle brands, such as Tesla, Weltmeister and Xpeng. Currently, the Company is negotiating over the cooperation with NIO, SAIC VOLKSWAGEN ID, Ford Mustang, and Geely SMART, and plans to establish new organizational structure and independent team to expand new-energy vehicle business. The Company also tries plenty of innovative business models, such as supermarket and vehicle delivery commission system, and after-market service models, including authorized repair/sheet metal /painting in batch center, so as to proactively adapt to the future industry development trend.

Investment Thesis

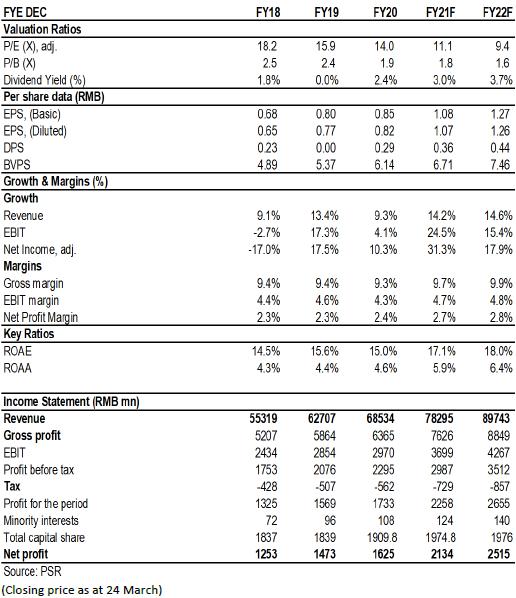

The main business of the Company will continue benefiting from the upgrade trend of domestic vehicle consumption, and will be further improved for operational efficiency. We are optimistic about the future development potential of the Company.We expect the company's EPS for 2021/2022EPS to reach 1.08/1.27 yuan and the target price of HK$16.5, corresponding to 2021/2022 13/11x P/E. We give Accmulate rating. (Closing price as at 24 March)

Financials

Click Here for PDF format...