Investment Summary

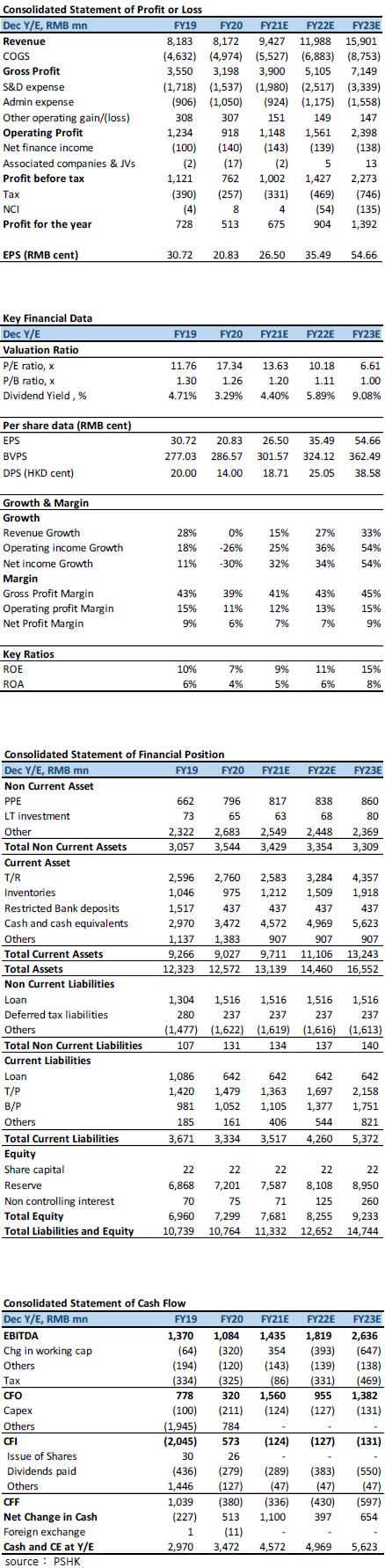

Xtep Int`l announced on March 18 the company's annual results for the year ended December 31, 2020. The company's revenue in 2020 was basically flat at RMB 8.17 billion (2019: RMB 8.18 billion). In line with expectations, the full-year net profit was RMB 513 million, a YoY decrease of 29.5% (2019: RMB 728 million), which was approximately 13% higher than our expectation, mainly due to the reduction in promotion expenses during the period. Excluding the one-off gains from the disposal of subsidiaries in 2019 and the disposal of the Supra brand in 2020, the company's net profit in the 2H20 increased by 23.9% YoY. The company declared a final dividend of 7.5 HK cents per share. Together with the interim dividend, the dividend payout ratio for the year remained at 60.0%.

The main brand's revenue declined, and the operating performance was well controlled

Xtep's annual revenue was RMB 8.17 billion, which was basically the same as last year's revenue, decreased by 0.13% from last year. In terms of revenue by brand nature, the company's mass sports/Athleisure /professional sports revenue was CNY7.10 billion /1.00 billion /0.07 billion, and the YoY changes were -7.9%/+114.4%/+608.6% respectively. Among them, the decline in revenue from Mass Sports (the main brand of Xtep) is mainly due to three reasons. 1) In 1Q20, the company repurchased inventory from distributors and destocked at a larger discount; 2) Actively reduced orders in 3Q20 and 4Q20 in order to maintain a healthy terminal inventory level; 3) The company has made changes in its accounting in 2020, deducting the rebate given to the distributors from the income, and the amount involved is about CNY 170 million , if the impact of related accounting adjustments is excluded, the company's actual revenue increased by 1.9% YoY, and the main brand revenue decreased by approximately 5.6% YoY. The growth of other brands is mainly due to the annual accounting in 2020 and the lower base in 2019.

The company's annual gross profit was CNY 3.20 billion, a YoY decrease of 9.9%, and GPM was 39.1%, a YoY decrease of 4.3 ppts, which is in line with our previous expectations (expected: 39.0%). The main reason was the decline in the GPM of the main brand. In Q1, the recovery of 300 million inventory of the main brand and the use of e-commerce to destock reduced the GPM by 1 ppts; the accounting adjustment decreased by 2.5 ppts; the main brand pricing multiplier adjustment decreased by 1.5 ppts; The increase in the proportion increases the GPM by 0.7ppts. The company's net profit for the year was RMB 513 million, which beat our previous expectations (previously expected to be RMB 452 million). Among them, it is mainly due to the fact that the company was affected by the epidemic during the year. The reduction in promotion cost of sponsoring the marathon was higher than we expected. SG&A was RMB 2.59 billion (previously expected: RMB 2.64 billion).

The main brand's performance in 2021 further improves

In the first two months of 2021, the main brand's retail sales turnover increased by 50% YoY, mainly due to the low base in the same period last year, which also saw a single-digit growth compared with the same period in 2019. The retail discount is 30% off, returning to the level of 2019. The retail inventory turnover level remains below five months. Management expects to improve to the level of 4-4.5 months before the end of the year. As of December 31, 2020, the number of Xtep brand stores was 6,021, a YoY decrease of 358, but the total sales floor area is similar to last year. It is expected that there will be a net opening of 200-300 stores in 2021, which will be mainly large stores. Management expects that in the next 5 years, Xtep's main brand revenue will grow at a CAGR of 15%, and the proportion of revenue from online channels will further rise to 30% (2020: 25%).

Overview of New Brand Development

Affected by the epidemic, the development of the new brand has been postponed for more than half a year. On December 31, 2020, Saucony and Merrell have 32 and 6 self-operated stores in first- and second-tier cities in Mainland China respectively; K-swiss has 43 self-operated stores in the Asia-Pacific Region and Palladium has 57 self-operated stores in Asia Pacific and Europe, of which 3 are located in Europe. Due to the continued epidemic in oversea, the business of K-swiss and Palladium in the Americas and Europe have been affected. The operating loss in 2020 will be RMB 104 million. It is expected that it will narrow in 2021 as the business resumes. The company plans to add 30-50 stores in professional sports and fashion sports in 2021, mainly Saucony and Palladium. The K-swiss store opening plan in China will start after the rebranding and is expected to be completed in 2022.

Valuation model adjustment

In summary, the difference between 2020 result and our previous expectations is mainly due to changes in promotion expenses during the period. We maintain our original revenue forecasts for the company for 2021 and 2022, which are RMB 9.43 billion and RMB 11.99 billion, respectively, with a growth rate of 14%. And 27%. It is expected that the company's main brand revenue in 2021 will return to the level of 2019 and is expected to further increase. We raised the company's sales and promotion expense ratio to 21% (previously: 20%) to further reflect the company's resources for promoting new brands. In addition, since the company is expected to further expand its channels in the professional sports sector in 2021, it is expected that the associated company will record a loss in 2021, and adjustments will also be made here. Overall, we lowered our 2021 and 2022 net profit forecasts to 675 million yuan and 904 million yuan (previously 704 million and 943 million yuan).

Valuation and investment advice

The company's revenue last year was in line with our expectations, while the profit side was slightly better than our expectations. Under the influence of the epidemic last year, the development of new brands was delayed, and the main brand also recorded a decline in revenue due to channel management. However, the impact of the epidemic on the company continued to be digested in 2020, and the sales and inventory levels of the main brand continued to improve quarterly, while maintaining better performance than other peers. It is expected that the company will be able to cultivate its new brands more effectively after the opening of the new operation center in Shanghai in 2021. As new brands develop and the company expands its market share, the valuation discount between the company and other leading peers is expected to be further narrowed. The company's EPS for FY21/FY22 is expected to be RMB 26.50/35.49 cents, and the company's target price is raised to HK$4.99 (previously RMB 4.25), which is equivalent to 16x the 2021 fiscal year forecast P/E, corresponding to the FY21E/FY22E P/E of 16.00x /11.95x, downgraded the rating to Accumulate.

(Current price as of March 22)

Financial

Click Here for PDF format...