Investment Summary

Last Year Witnesses 20% Result Growth with the Fourth Quarter Generating Extraordinary Revenue

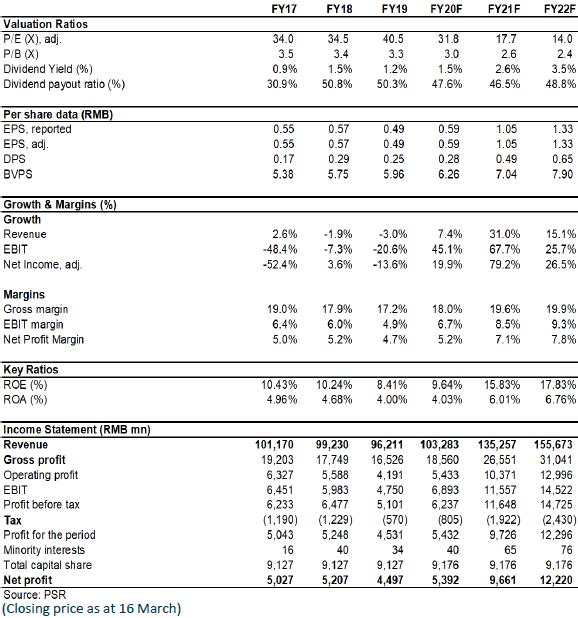

Based on the company's performance bulletin of 2020, Great Wall Motors (GWM or the Company) reported revenue of RMB103.283 billion with a yoy growth of 7.35%, a net profit attributable to the parent company of RMB5.392 billion with a yoy rise of 19.9%, and a basic EPS of RMB0.59. This growth was mainly contributed by increases in whole vehicle sales volume, capacity efficiency, and gross margin. Especially when it comes to the fourth quarter which delivered a great result including revenue of RMB41.1 billion, the highest in company history, representing a yoy increase of 22.4%, and qoq 57%. Also, the net profit was RMB2.81 billion, indicating a yoy growth of 77.5%, a qoq surge of 95%, and bringing it to a second high in history. Though the sales volume of the first quarter decreased by 47% due to the pandemic, the Company's car sales volume in the other three quarters saw strong rebound and sold 1.11 million cars in 2020 with a yoy growth of 5% thanks to the strong new product cycle and the recovering industry.

From the perspective of brands, 750,000 HAVAL, 78,500 WEY, 225,000 PICKUP, and 56,300 ORA cars were sold, respectively. This marked a yoy growth of -2.50%, -21.53%, 51.18% and 44.76%, and a sales percentage of 68%, 7%, 20%, and 5%, respectively. Many car models of the Company flourished, for example, the new platform car model like the third generation HAVAL H6, HAVAL Dagou, Tank 300, ORA Haomao received positive responses upon their launching. More than 20,000 cars of the third generation HAVAL H6 were sold in consecutive months, and more than 10,000 cars of HAVAL Dagou were sold in the first three months after its launching. Sales in the fourth quarter became more and more extraordinary as the car sales volume reached around 430,000, marking a record high. Among them, the sales volume of HAVAL, WEY, PICKUP, and ORA were 305,200, 28,200, 64,700, and 32,300, respectively. This represented a yoy growth of 22.98%, -6.50%. 27.87% and 284.32%, and a sales percentage of 71%, 7%, 15%, and 7%, respectively. It can be seen that with the benefit of new technological platform and strong car model cycle, GWM has extended its business to specific markets by consolidating and maintaining its steady growth of SUV business, and it has made breakthroughs as the new car models have clear competitive margin and may bring higher sales volume in the future.

A Good Start in the New Year, More Advances is Expected

The strong trend was maintained at the beginning of 2021 as the Company's car sales volume in January and February was 139,000 and 89,000, a yoy growth of 73.20% and 788%, respectively. Also, the total sales volume of the first two months rose 153% yoy, a growth of 26% compared to 2019 when there was no pandemic, and this accounted for 19% of the annual sales target. The accumulative sales volume of HAVAL, WEY, PICKUP, and ORA was 155,500, 17,500, 37,400, and 17,600, with a sales percentage of 68%, 7.7%, 16.4%, and 7.7%, respectively.

Specifically, 16,600 HAVAL Dagou and 9616 new car model HAVAL F&L, 18,000 F7, and 24,500 M6 were sold. For WEY, its total sales volume in the first two months was 17,500 of which 9318 were contributed by the brand Tank 300. For PICKUP, it was 37,000, and more than 20,000 was contributed by the brand GWM POER. For ORA, the number was 17,700 of which 10651 Heimao, 3615 Haomao, and 3368 Baimao were sold, respectively.

In 2021, the Company will launch at least 10 new car models equipped with new technology and new power, including HAVAL Chitu, M6 PLUS, Dagou 2.0T, New generation F7, WEY Mocha, Latta, Macchiato, etc., and GWM POER Heidan and two MPVs. Sales effect brought by new platforms and increasing sharing of spare parts will continue to improve the Company's profitability..

Strategic Investment in Automotive Chips

Recently, GWM has finished its strategic investment in a leading intelligent automotive chip maker Beijing Horizon Robotics, marking its entering into the chip industry. The two enterprises will highlight their cooperation in areas like Advanced Driver Assistance Systems (ADAS), Automated Driving, Intelligent Cockpit Multi-modal Interface, etc. Based on the intelligent strategy of "Coffee Intelligent Driving 331", GWM will become the first company in China that can equip automated cars with L3 driving capability for the whole vehicle, massively produce automated cars with lidar and NOH high-speed automatic navigation assistance. We believe that the cooperation with Horizon Robotics will speed up the research and development as well as the implementation of mass production of the Company's intelligent car.

Investment Thesis

Considering the better-than-expected sales and revised financial forecast, we raised our target price to HK$26, equivalent to 20.7/16 x P/E and 3.1/2.8x P/B ratio in 2021/2022. We reaffirm the rating of ¡§Accumulate¡¨. (Closing price as at 16 March)

Risk

New vehicle sales fall short of expectations

The SUV market dramatically worsens

The progress of new energy vehicle/Pickup is poorer than expectations

Financials

Click Here for PDF format...