Investment Summary

NetEase's 4Q20 revenue slightly beat the market expectation, while the NP is below market expectation

The company's 4Q20 revenue was RMB 19.8 billion (+25.6% yoy /+5.9% qoq), and the 4Q20 revenue exceeded the Bloomberg's consensus. In terms of the breakdowns, the company's revenue for online game sector/ Youdao sector/ innovative and other business sector were RMB 13.4 billion (+15.5% yoy / -3.3% qoq) / RMB 1.11 billion (+169.7% yoy / +23.5% qoq) / RMB 5.25 billion (+41.3% yoy / +34.7% qoq), respectively. The revenue proportion of online game/youdao/innovation and other businesses sector were 67.8%/5.6%/26.6%, respectively.

The company's 4Q20 GP was RMB 9.93 billion (+20.9% yoy / +0.4% qoq), and the GPM was 50.2%, which represented a decrease of 2.0ppts yoy /2.8ppts qoq. The main reason for the decline in GPM was due to the gradual decrease in the revenue proportion of the company's higher GPM sector, namely the online game sector.

The company's 4Q20 operating profit was RMB 3.01 billion (+1.2% yoy / +4.9% qoq), with an operating profit margin of 15.2%, which represents a 3.7ppts yoy /0.2ppts qoq decline. The company's 4Q20 NP was RMB 930 million (-69.8% yoy / -66.5% qoq), and Non-GAAP NP was RMB 1.6 billion (-56.4% yoy / -56.5% qoq). The sharp drop in 4Q20 NP and Non-GAAP NP were mainly attributable to the RMB 270 million investment loss and RMB 1.80 billion exchange loss recorded in 4Q20.

The online game sector is performing stably, and the company will enter a new game launching cycle in 2021

The company's 2020 revenue from online game sector was RMB 54.61 billion (+17.6% yoy) and mobile game revenue accounted for 71.9% of total online game revenue (+5ppts yoy). The growth momentum of online game revenue in 2020 was mainly derived from old games, such as Fantasy Westward Journey (¹Ú¤Û¦è´å), Western Journey Online mobile game (¤j¸Ü¦è´å¤â¹C), Invincible (²v¤g¤§ÀØ) and Life-after (©ú¤é¤§«á) etc. These games all ranked high on the 2020 IOS top grossing chart in China. The company's 4Q20 revenue from online game sector was RMB 13.40 billion (+15.5% yoy / -3.3% qoq). The qoq decline in the revenue of the online game sector in Q4 was mainly due to the company's weak game pipeline in Q4. The launching of the hardcore MMO mobile game, Revalation (¤Ñ¿Ù) was delayed to Jan 2021. The GPM of the online game sector in 4Q20 was 63.1% (+0.0ppts yoy/ 0.5ppts qoq). The small qoq change in GPM was mainly affected by changes in the proportion of mobile games and PC games revenue as well as the changes in the proportion of revenue from self-developed and non-self-developed games.

As for new games, the company's game pipeline is very strong in 2021. Big IP titles such as, Revalation (¤Ñ¿Ù), Diablo® Immortal™ (·t¶Â¯}Ãa¯«¡G¤£¦´), Harry Potter: Magic Awakened («¢§Qªi¯S¡GÅ]ªkı¿ô) and etc are all scheduled to be launched in 2021. The launching of these games will lead the company to enter a new game launching cycle in 2021. Revalation (¤Ñ¿Ù) was already launched in January 2021. Within the first month of launching, it has already reached 9th place on the Sensor Tower Jan 2021 IOS top grossing chart in China. On the other hand, Diablo® Immortal™ (·t¶Â¯}Ãa¯«¡G¤£¦´) and Harry Potter: Magic Awakened («¢§Qªi¯S¡GÅ]ªkı¿ô) have both received launching approval and are expected to be launched globally in 2021.

The revenue growth of Youdao has accelerated and margin has increased significantly

The revenue of Youdao in 4Q20 was RMB 1.11 billion (+169.7% yoy / +23.3% qoq). Among different sector of Youdao, the revenue growth of learning service sector and learning products sector were the most significant. The revenue of Youdao learning service sector/ Youdao learning products sector in 4Q20 were RMB 730 / 240 million, up by 198.8%/253.8% yoy respectively. In terms of Youdao learning services, the gross billing of Youdao online course was RMB 1.12 billion (+222.8% yoy) and the gross billing of Youdao premium course was RMB 1.04 billion (+268.8% yoy). The gross billing of Youdao K-12 premium course, the signature product of the Youdao premium course, was RMB 767 million (+354.6% yoy) and has reached a new record high. Regarding the learning products sector, the company has launched Youdao Dictionary Pen 3.0 in 4Q20.

The GPM of Youdao in 4Q20 was 47.5%, (+17.7ppts yoy / +1.6ppts qoq). The increase in Youdao GPM was mainly attributable to 1) the enhancement of scale effect 2) the further optimization of teacher salary structure 3) the significant increase in sales of Youdao dictionary pens, which has higher GPM. In addition, although the S&M expenses of Youdao in 4Q20 was still at a relatively high level, with expense ratio of 73%. Nonetheless, it has dropped significantly comparing to the 123% in 3Q20. On the whole, we believe that with the high revenue growth and the further enhancement of Youdao's brand imagine, Youdao is expected to achieve stronger scale effect.

The revenue of Innovative and other business segment showed high growth in 4Q20, the monetization ability of cloud music is expected to be further strengthen in the future

The revenue of the innovative and other business segment in 4Q20 was RMB 5.25 billion (+41.3% yoy / +34.6% qoq), and the high growth was mainly driven by the cloud music sub-sector. At present, the revenue source of the cloud music sub-sector can be divided into three parts: membership, advertising, and live broadcast value-added services. The company's management mentioned that the quality of the music content on the cloud music platform will be continued to be enhanced in the future. Hence, we believe that the membership revenue will be the major revenue source of the cloud music sub-sector. With the further development of the paying habits of China music platform users as well as the further increase in the penetration rate of paying music platform in China, we believe that the monetization ability of Netease Cloud Music will be strengthen.

Valuation

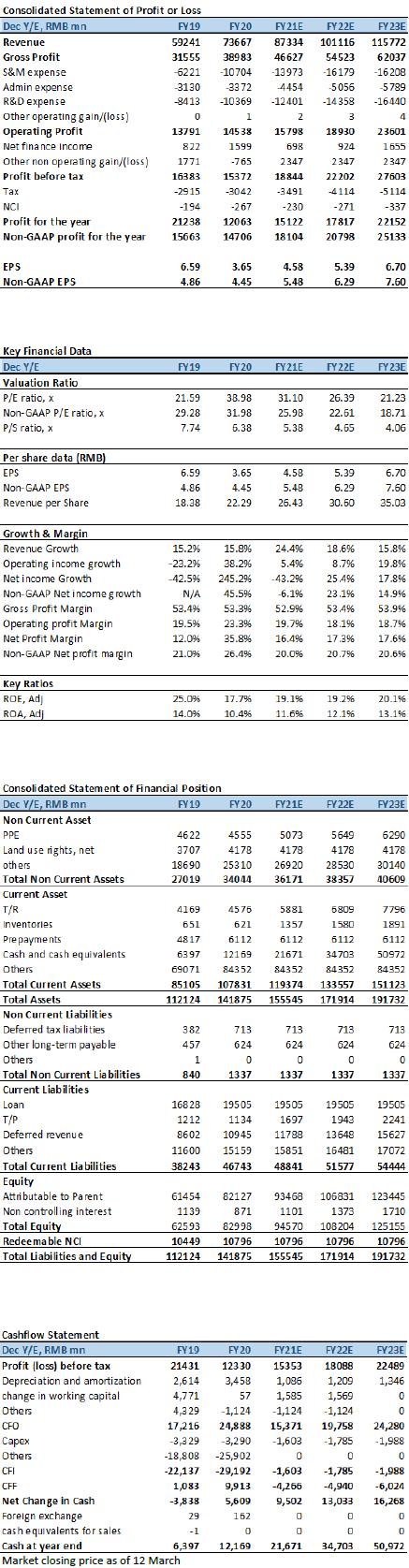

After considered that 1) the company is entering a new game launching cycle in 2021-2022 2) revenue growth of Youdao beat our previous forecast 3) the monetization ability of the company's innovative and other business sector is expected to be further strengthen, we revise our 2021/2022 revenue forecast upward to RMB 87.3/101.1 billion (our previous forecast was RMB 83.3/96.3 billion) and we introduce our 2023 revenue forecast of RMB 115.8 billion. However, since 1) we expect Youdao to continue to spend high in customer acquisition for the following years 2) The S&M expense of games tend to be higher at the beginning of their life cycles, we revised our 2021/2022 Non-GAAP NP forecast downward to RMB 18.1/20.8 billion (our previous forecast was RMB 19.9/22.6 billion). We have rolled-over our SOTP valuation to 2022 and maintain target PE of 25x for online game sector, raise target PS to 5x for the Youdao as well as the innovative and other business sectors. We raise TP to HKD 202.50 (+17.2%), with corresponding 2021/2022/2023 Non-GAAP PE at 31.4x/27.4x/22.6x. We maintain Buy rating. (Market closing price as of 12 March) (exchange rate: RMB 0.85/HKD)

Risk

1) The tightening on Game regulations

2) The Games underperform comparing to expectation

3) The growth of Youdao is worse than expected

4) Failure in monetization for innovative businesses

Financial Statements

Click Here for PDF format...