|

CSPC PHARMA(1093)

Analysis¡G

CSPC Pharmaceutical Group (1093) announced that CSPC Shanghai, a wholly-owned subsidiary of the Group, has entered into a product licensing and commercialization agreement with Beta Pharma in relation to the exclusive product licensing and commercialization of BPI-7711 Capsules, a third generation irreversible EGFR-TKI for the treatment of non-small cell lung cancer. The inclusion of such product will further enrich the Group's oncology products portfolio. The Group firmly believes in the importance of investing in research and development. At present, there are more than 300 projects in the pipeline, primarily focusing on the therapeutic areas of oncology, autoimmunity, psychiatry and neurology, digestion and metabolism, cardio-cerebrovascular system and anti-infectives. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $8.60, Target Price: $9.70, Cut Loss Price: $8.00

|

ANTA SPORTS(2020)

Analysis¡G

In 1H20 results, the company's total revenue fell 1% from the same period last year to RMB 14.67 billion. The results for the first half of the year reflect the company's resilience and ability to respond to the market. It is expected that the company can respond quickly after the epidemic. In mid-2020, the company proposed to transform the business model of the Anta brand from a wholesale distribution model to a direct-to-consumer model (DTC), enabling the company to mobilize resources more flexibly in retail, channel, merchandise, finance, and human resources, and improve operational efficiency. In 4Q20 results, the main brand sales were lower than market expectations, but the FILA brand and other brands maintained high growth during the period.

Strategy¡G

Buy-in Price: $115, Target Price: $138, Cut Loss Price: $104

|

|

Semir Garment (002563.SZ) - Profitability improved significantly after the divestment of Kidiliz, and Q4 profit beat expectation

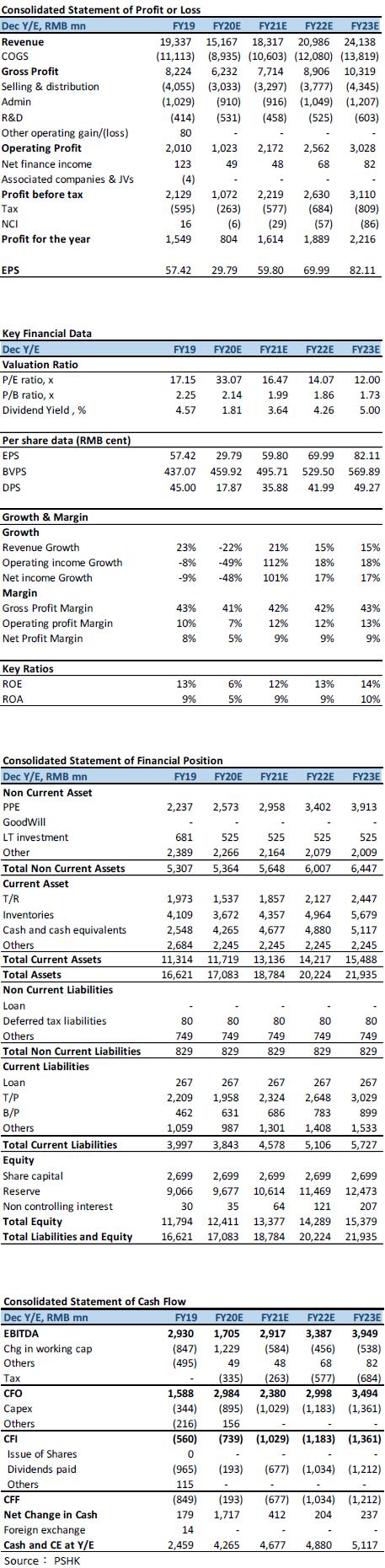

Investment SummaryThe company announced the 2020 annual results preview on February 27. The revenue in 2020 is about 15.17 billion yuan, a YoY decrease of 21.56%. Operating profit is about RMB 1.15 billion, a YoY decrease of 46.47%. The net profit attributable to the parent is about RMB 0.80 billion yuan, a YoY decrease of 48.21%. The company's revenue under our expectation, however, the profitability beat expectations. Looking closer to quarterly result, the company's revenue from 20Q1 to 20Q4 was 2.74/3.00/3.72/5.72 billion yuan, and YoY changes were -33.51%/-26.95%/-26.30%/-5.90%. In terms of revenue, the company's revenue has continued to improve in the past four quarters, and the decline has been significantly narrowed, but it is relatively low compared to our previous estimate of revenue, mainly due to the negative impact of excluding the French subsidiary Kidiliz from the consolidated statement is greater than expected. Excluding the impact of divestiture of subsidiaries, on revenue, the company is expected to record HSD growth in 20Q4. In terms of profit, the company's profit in the Q4 improved significantly. The operating profit and net profit attributable to the parent in the Q4 were 820 million yuan and 590 million yuan, an increase of 95.2%/142.3% YoY. Operating profit margin and net profit margin both have significantly improved, 14.3% and 10.3%, respectively, mainly due to the reduction of the negative impact on the company's profitability after the divestiture of the subsidiary. Valuation model adjustmentIn our previous valuation model, we expected the company's children's wear/leisure wear growth to be 0%/-5% YoY in 2020, and the overall revenue growth rate will be -11.8% YoY. The company's business recovery in the fourth quarter was slower than we expected. The company's whole-year revenue fell 21.56% YoY, which was lower than our expectations. However, in terms of profitability, we previously predicted that under the epidemic situation, the company's profitability will be affected by inventory pressure and discount promotion. The overall NPM is 3.3%, but the company's overall cost control greatly exceeds our expectations. The actual NPM is 5.3%. It offset the negative impact of the slower business recovery rate, the actual net profit for FY2020 was RMB 800 million, beat our expectations. As there is significant decrease in company expenses after the divestiture of Kidiliz, we lowered the company's sales and administrative expenses estimates for the next three years to 18% and 5% (previously 20% and 6%), and FY21/F22's EPS were raised to RMB 59.80 cent/69.99 cent (previously 53.38 cent and 62.21 cent). Financial forecast and valuationSemir Apparel has taken a leading position in the domestic children's and casual wear markets. The acquisition of Kidiliz business in 2018 brought significant revenue growth to the company, but at the same time it also caused a substantial increase in the company's cost. In addition, the European epidemic situation has not improved. Kidiliz's loss to the company expanded. In Q4, it shows the divestiture has a significant negative impact on the company's revenue, but the company's profitability has risen. In the future, the company is expected to improve its profitability after divesting Kidiliz. Based on 1) After the divestment of Kidiliz, it will have a short-term impact on the company's children's clothing segment revenue, but the company has its own brand of Balabala in the children's clothing business to continue to provide growth, and it is expected that the children's clothing business will be stabilized and expanded. 2) After the divestment of Kidiliz, the company has improved its expenses of the period management, and its overall profitability has increased. The Q4 reflects the actual impact of Kidiliz's divestiture on the company. Based on this, we raised the company's profit forecast. The profit is RMB 59.80/69.99 cents, and the twelve-month target price is raised to RMB 11.96, corresponding to the FY20/FY21E/FY22E earnings ratio of 40.1x/20.0x/17.1x. (Closing price as of March 4) Risk1) The impact of COVID-19 continues 2) Overlapping positioning between brands Financials

Click Here for PDF format...

| Recommendation on 11-3-2021 | | Recommendation | Buy | | Price on Recommendation Date | $ 9.850 | | Suggested purchase price | N/A | | Target Price | $ 11.960 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2021 Phillip Securities (HK) Ltd. All Rights Reserved.

|