Investment summary

With the Introduction of Strategic Investor, the Debt Crisis Turns Around and the Lithium Salt Project Is Expected to Advance

Tianqi Lithium announced on December 8, 2020 that its wholly-owned subsidiary Tianqi Lithium Energy Australia Pty Ltd (TLEA) intends to introduce strategic investor IGO Limited (IGO), an Australian listed company, through capital increase and share expansion. For this capital increase, IGO's wholly-owned subsidiary intends to contribute USD1.4 billion in cash to subscribe for the newly increased registered capital of TERA by USD304 million. After the completion of the capital increase, the Company will hold 51% of the registered capital of TLEA, and investors will hold 49% of the registered capital of TLEA. The premium of USD1,096 million will be included in the capital reserve of TLEA.

The Company and its subsidiary will use such money to repay the principal of the syndicated loan of no less than USD1.2 billion. The remainder after the repayment will be used by TLEA as supplementary capital for the operations and commissioning of a lithium hydroxide plant operated by TLEA subsidiary Tianqi Lithium Kwinana Pty Ltd (TLK) in Australia.

After the deal is closed, the Company still has control over TLEA. It can control TLEA's financial and operating decisions through the Board of Directors. There is no change in the scope of consolidated statements. However, this deal still requires pending approval by the syndicate and review organizations of the local government. It is expected to take approximately 4 to 6 months.

In 2018, the Company invested USD4.07 billion in the acquisition of SQM's equity, which generated USD3.5 billion in debt. One of the main reasons for the Company's result losses in 2019 and 2020 is the surge in financial expenses incurred by asset acquisition. The Q3 2020 report shows that the long-term borrowings and non-current liabilities due within one year totaled RMB26.3 billion, including the outstanding acquisition loan of USD3,084 million. If the deal goes well, the Company's debt will significantly drop by nearly 40%, and the asset-liability ratio will drop from 81% to approximately 63%. The debt burden will be greatly eased.

On the other hand, due to reasons such as capital and market, the Company's 48,000-ton lithium hydroxide expansion project in Australia was slower than expected (Phase I project was about to be commissioned, and more than half of the construction costs were invested in Phase II project). After the repayment of the loan, the USD200 million capital injection will accelerate the project. Phase I project is expected to reach capacity target next year.

It is worth mentioning that the investor IGO has many years of experience in mine operations. It will play a very positive role in helping Talison Lithium further reduce operating costs and increase the recovery rate in the future. In addition, it can enhance the Company's operations management capabilities in terms of Australian labor, policies, environmental protection, and local culture.

Lithium Price Reopens the Upward Channel and the Lithium Giant Bails Out

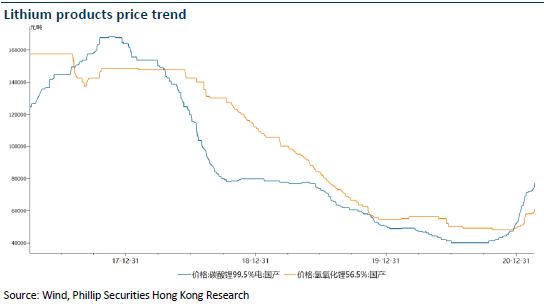

With the recovery of the domestic and European new energy vehicle markets, the installed capacity of power batteries is increasing, and the upstream industry chain closely related to power batteries continues to heat up. On the other hand, the strong growth of 3C digital products, lithium battery energy storage, and two-wheeled electric vehicles has also driven the price of raw materials of lithium salt to climb. According to SMM data, as at January 18, the average price of domestic battery-grade lithium carbonate was RMB67,000 per ton, an increase of approximately 60% from the lowest level since the beginning of 2020; the average price of lithium hydroxide was approximately RMB49,000 per ton, an increase of 15% from the lowest level since the beginning of 2020. In terms of the price trends, due to seasonal restrictions on supply-side capacity, the growth momentum for lithium salt prices is still quite strong. The price is expected to rise to RMB75,000 per ton in the short term. With the support of strong demand, it is expected that lithium salt products will be in a tight supply this year. The price is expected to remain above RMB75,000 per ton.

The Company increased market presence in the world's most high-quality lithium resources. It held shares in Talison Lithium, the owner of spodumene mine at Greenbushs ¡V the world's best hard rock lithium mine, and took a stake in SQM, a producer with the mining right of Atacama salt lake ¡V the world's most high-quality salt lake. In terms of lithium salt, the Company currently has a production capacity of lithium carbonate of 34,500 tons per year and a production capacity of lithium hydroxide of 5,000 tons per year. In addition, the Company has projects under construction that produce 48,000 tons per year of lithium hydroxide and 20,000 tons per year of battery grade lithium carbonate. Amid the industry boom, the Company's production bases are currently saturated for the capacity utilization. We believe that in the subsequent development, the Company's resource advantages will become increasingly prominent. With the gradual resolution of the debt problem, there is a high probability of result turnaround and there is room for an expected upward flexibility.

Valuation and Investment thesis

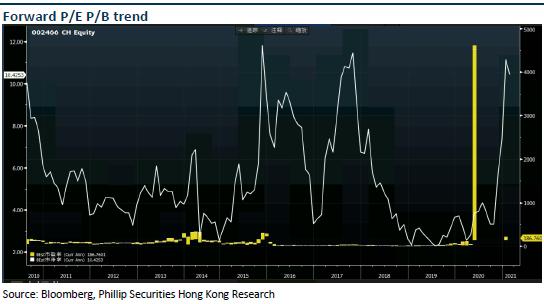

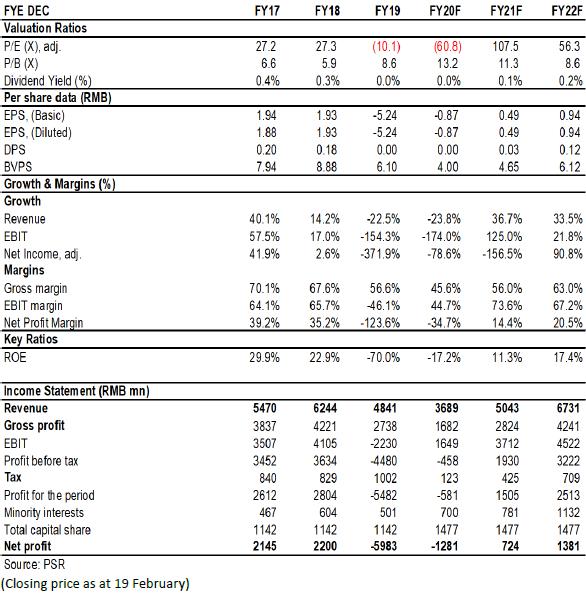

Tianqi Lithium not only holds shares of companies with the world's largest scale and best lithium ore resources in production, but also has the world's largest processing capacity on extracting lithium from ores, which make Tianqi Lithium the best investment object in upstream sectors of domestic new energy vehicle industry chains. We expected diluted EPS/BVPS of the Company to RMB -0.87/0.49/0.94 and 4.0/4.65/6.12 of 2020/2021/2022. And we accordingly gave the target price to 62, respectively 13.3/10.0x P/B for 2021/2022. "Accumulate" rating. (Closing price as at 19 February)

Risk

New business progress slower than expected

Lithium series Product price falling

Financials

Click Here for PDF format...