Investment Summary

The operating performance of the Anta brand in Q4 is slightly lower than expected

The company announced on January 13 the operating performance of the 4Q20 and the whole year. In the Q4, the retail sales of Anta's main brand, FILA and other brands recorded a LSD /25%-30%/55% - 60% growth YoY. In term of the whole year, the retail sales of Anta's main brand, FILA and other brands were negative growth in MSD, positive growth in MDD and positive growth of 35%-40%, respectively.

Increase efforts to eliminate seasonal inventory, major brand recorded LSD growth in Q4

The Anta brand's overall turnover recorded a LSD positive growth in a single quarter. Among them, Anta's adult and children's clothing both recorded LSD growth in Q4, which was lower than we expected (Previous expectation was LDD growth). Company's Q1/Q2/Q3 year-on-year growth of 20% + negative growth/negative Low single digit/positive growth. In terms of channels, Anta's offline retail sales still recorded a negative growth YoY. In terms of discounts and inventory-to-sales ratios, as the company repurchased some seasonal products from distributors while DTC conversion. In order to speed up destocking, in the fourth quarter, the company increased retail discounts. The Anta brand discount rate increased 2-3ppt to 30% off. The inventory-to-sales ratio improved further from 6 in the first three quarters to 5, which was in line with the company's target.

Overall, the annual retail sales of Anta's main brands were recorded negative growth in MSD, mainly due to the impact of the epidemic and the DTC transformation during the year. The company focused on destocking and reduced some Q4 product orders. At the end of December, the company's inventory-to-sales ratio and the sales rate have improved, and the company has made remarkable achievements in inventory management. The transformation of the DTC model of Anta's main brand is progressing smoothly. As of the end of December, the company has completed 82% of store handovers, which is faster than the company expected. The company is expected to complete the handover in the first quarter of next year.

The multi-brand strategy brought growth to the company under the epidemic

FILA as a whole achieved 25%-30% growth in Q4, online sales continued to exert strength, and FILA's online pipeline growth rate exceeded 70%. In term of the product line, FILA Core's retail sales volume grew by MDD, FILA KID grew by more than 20%, and FILA Fusion grew significantly, with retail sales growth exceeding 50%. In the whole year, FILA's turnover growth rate was in double digits. In terms of inventory-to-sales ratio and discounts, FILA's regular price discount returned to about 8.3%, and the inventory-to-sales ratio was more than 6 times in the Q4. The overall offline store performance is better than before the epidemic.

Other brands recorded a 55%-60% increase in overall sales in Q4, in line with expectations. Among them, sales from the Descente brand increased by more than 80% year-on-year, and Kolon Sport also recorded a year-on-year growth of more than 40%. The cumulative retail sales of other brands throughout the year increased by 35%-40% year-on-year.

In 4Q20 results, the main brand sales were lower than market expectations, but the FILA brand and other brands maintained high growth during the period. In the fourth quarter, Amer Group made a positive contribution to the company's profit, and its annual loss narrowed, which is expected to offset the negative growth of the main brand. The company's long-term investment logic remains unchanged, focusing on the growth brought about by the company's main brand channel upgrade and the cultivation of new brands. We adjusted the company's profit forecast for 2020 by lowering the annual revenue growth of the main brand to -5% (previously expected to be flat). In addition, we have also reduced the JV's expected loss for the company. We expect the company's EPS in 2020/2021/2022 to be CNY 1.74/3.08/4.12 (Previous: CNY 1.76/3.08/4.12). Maintain the 12-month target price of HK$144.94 corresponding to the expected P/E of 70.80/40.00/29.61 times for 2020/2021/2022, and maintain the Accumulate rating.

Risk

1) Mainland encounter second wave of COVID-19

2) Growth of newly acquired brands is not as expected

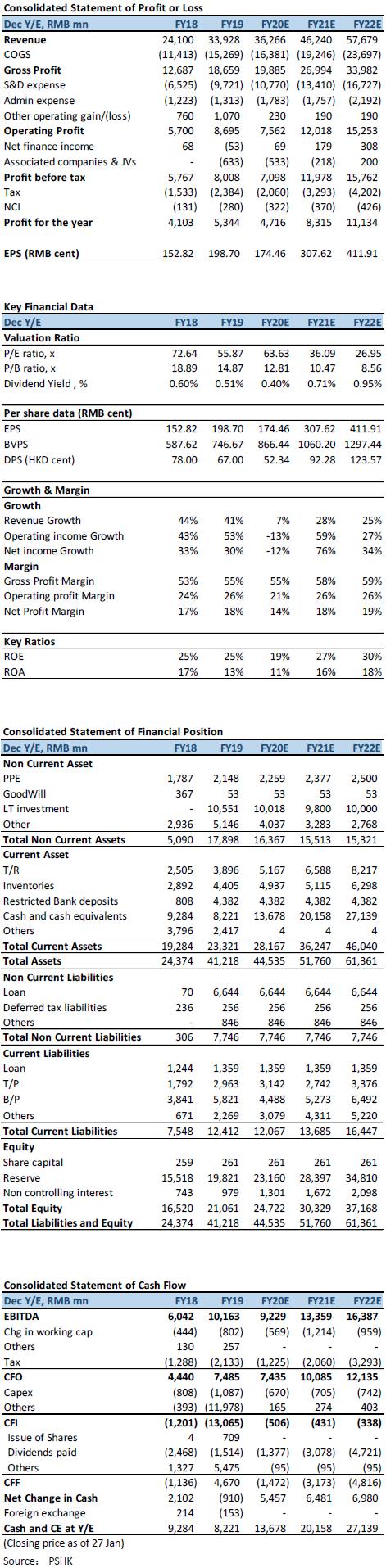

�Financials

Click Here for PDF format...