Investment Summary

Prosperity of Premium Cars Continues to Improve in H2, and New Car Sales Grow Strongly

The latest sales show that Zhongsheng's new-car-sales momentum continued to be strong in H2 of last year benefiting from the explosion of demand for premium cars after the COVID-19 pandemic. The Company achieved an approximately 20% growth rate in new car sales in 2020Q3. Amid the continuous prosperity of the auto market in 2020Q4, the Company's new car sales showed positive growth compared to Q3, with an estimated yoy growth rate of more than 30%. On the whole, new car sales are expected to achieve a yoy growth rate of 30% in 2020H2. Specifically, the sales of premium cars performed better than the overall. The yoy sales growth in Q3 and Q4 is expected to exceed 25% and 35%, respectively. The sales of premium cars will grow by more than 30% in 2020H2.

Low Inventory Level, and Price Discounts Are Further Narrowed to Boost Profitability

Due to the overseas pandemic affecting the supply of some imported models and its excellent inventory management, the Company's inventory is at a historically low level. Currently, it is only maintained at a level of approximately 0.6 months, better than the industry average. The Company aims to maintain the inventory at a level of less than one month.

With a short supply of premium cars, the gross margin of new car sales continued to improve in Q4. Even though the period of promotion season is approaching, the price of new cars remains high, and discounts for some hot-selling models are very limited.

In terms of new orders, the momentum of new car sales has not diminished since January 2021, with a yoy increase of nearly 40%. Terminal discounts have also been very stable. The overall operation has improved significantly over the same period of last year. We expect the Company's profitability will significantly benefit from the further narrowing of price discounts and the continuous optimization of the sales structure.

After a brief slowdown during the pandemic period, after-sales business has rebounded rapidly since H2 of last year. The after-sales entrance and after-sales revenue recorded a yoy growth rate of 25-30%. We believe that the main reasons are the expansion of base customers of premium cars and the increase in the penetration of extended warranty. The Management offers an optimistic outlook for the after-sales business this year, with an expected growth of more than 20%.

Network Optimization and Multi-business Arrangements Are Expected to Become New Engines

In H1 of last year, the Company tended to be cautious about the capital expenditures due to the pandemic. As at June 30, 2020, the number of car dealerships reached 365, of which 21 were opened and 16 were closed, with a net increase of 5. Specifically, the dealerships of premium car brands numbered 210, accounting for 58%. The dealerships of mid- and high-end car brands accounted for 42%. In the second half of the year, the company acquired eight 4S stores at a consideration of 7.2 trillion yuan. The newly purchased 4S stores were mainly luxury brands, further improving its brands mix. The Management's 2021CAPEX target is set at approximately RMB2 billion, including 20 new stores and external M&A opportunities.

In terms of new energy vehicles, the Company last year sold approximately 2,000 units of new energy vehicles, which currently account for a small proportion. The Management stated that in the future, the Company will seek partners to expand the sales network of new energy vehicles, in an effort to increase their proportion in premium cars.

In addition, second-hand cars have been an important development sector for the Company in recent years. The transaction volume of second-hand cars in 2020H1 reached 40,676 units, a yoy increase of 33.9%. Premium cars and Japanese cars enjoy a high value-preserving rate and are expected to benefit from the release of policy dividends in the future.

On the whole, we expect that network optimization and multi-business arrangements will become the new engines for the Company's future business growth.

Investment Thesis

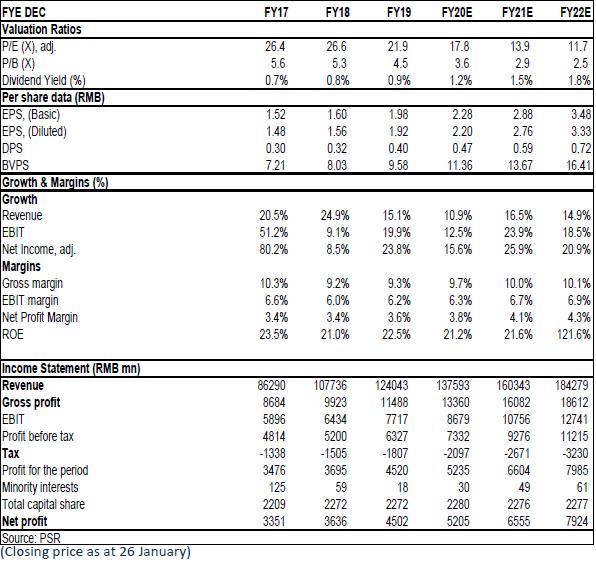

We expect the company's EPS for 2020/2021/2022 to reach RMB2.28/2.88/3.48 yuan and the target price of HK$70, corresponding to 2020/2021/2022 26/20/17x P/E (considering its leader position and better mix). We gave a BUY rating. (Closing price as at 26 January)

Financials

Click Here for PDF format...