Investment Summary

Sales Volume in October Increases Rapidly, up 26% yoy

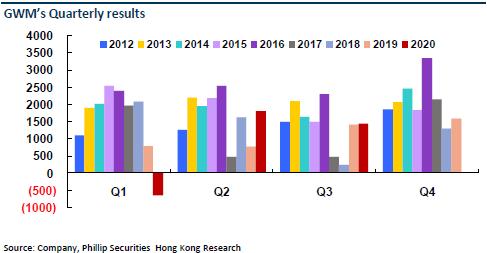

Great Wall Motors recently released sales data for October 2020. In November, the Company reported a sales volume of 145,200 vehicles, an increase of 26.12% yoy and an increase of 7.14% qoq. The cumulative sales volume in the first ten months reached 961,500 vehicles, a cumulative increase of 0.75% yoy, recording a positive growth rate yoy. Great Wall Motors continued the rapid sales growth in November, which was stronger than market expectations.

Haval and GWM Pickup Perform Outstandingly and the Company Remains Optimistic about the Market Outlook

In terms of sub-brands, Haval and GWM Pickup displayed outstanding performance.

1) Haval recorded a sales volume of 101,812 vehicles this month, an increase of 22.1% yoy. The increase mainly came from Haval H6, Haval Big Dog, Haval M6 and Haval H9. In particular, driven by the third-generation Haval H6, the sales volume of Haval H6 has outstripped 50,000 vehicles for two consecutive months, setting a new monthly high this year. After its launch in the market for three months, the sales volume of Haval Big Dog continued to climb, contributing 8,555 vehicles. Haval First Love, Haval Big Dog 2.0T, and the third-generation Haval H6 2.0T are to be launched. While continuing to improve the product map, the Company is expected to continue to improve its model structure and profit margin.

2) The WEY brand was sold by 9,122 vehicles, a decrease of 12.7% yoy. At the end of November and early December, the Company began to accept orders of the WEY Tank 300 officially. The order exceeded 10,000 vehicles in two weeks. The WEY Tank 300 is the first model of the Company's new modular vehicle platform "Tank". It is positioned as a smart luxury off-road SUV, with a price range of RMB176,000 to RMB214,000, which is slightly higher than the WEY VV7. After the launch of several new models, we look forward to a boost in sales volume of the WEY brand in 2021.

3) GWM Pickup reported a sales volume of 22,610 vehicles, up 18.6% yoy, exceeding 20,000 vehicles for two consecutive months. In particular, GWM Pao Pickup was sold by 12,100 vehicles, continuing to dominate the domestic high-end pickup market. With the addition of modified models such as its Rescue Pao and Brigade Pao, we continue to be optimistic that GWM Pickup will maintain strong sales performance.

4) The ORA brand was sold by 11,592 vehicles, a surge of 414.7% yoy, exceeding 10,000 vehicles for the first time. In particular, the sales volume of ORA Black Cat was 9,463 vehicles, an increase of 373% yoy and an increase of 51% qoq. The ORA Good Cat, which is positioned as the "new generation electric car", has been launched recently, with a price range of RMB103,900 to RMB143,900. It is expected to complement with the original model in a mismatched manner, and further enrich the product layout of the ORA brand.

Investment Thesis

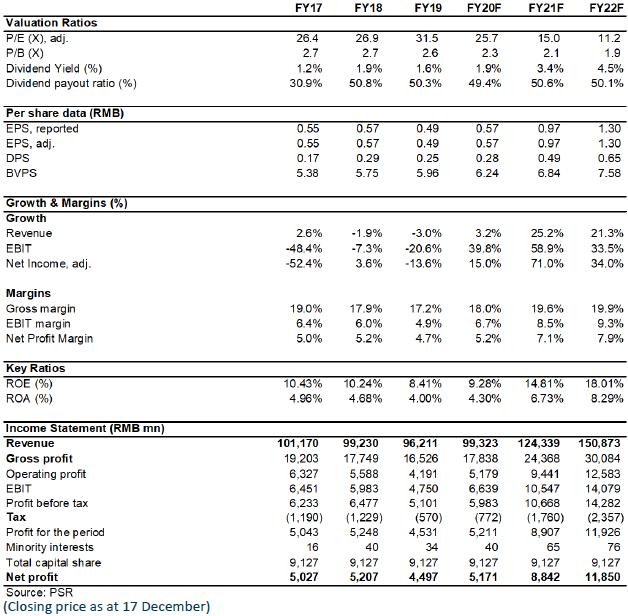

Considering the better-than-expected Nov sales and revised financial forecast, we raised our target price to HK$19.7, equivalent to 29/17/12.8x P/E and 2.7/2.4/2.2x P/B ratio in 2020/2021/2022. We reaffirm the rating of ¡§Accumulate¡¨. (Closing price as at 17 December)

Risk

New vehicle sales fall short of expectations

The SUV market dramatically worsens

The progress of new energy vehicle/Pickup is poorer than expectations

Financials

Click Here for PDF format...