|

IRC(1029)

Analysis¡G

IRC (1029) reported its maiden underlying profit of US$6 million for the six months ended 30 June 2020, mainly attributable to good production rate, strong iron ore price, weak Russian Rouble and declining interest rate. Although the profit is modest, the milestone is significant. On the demand side, the Chinese government has recently pledged to increase its expenditure on infrastructure as part of its economic stimulus plan, increasing its demand for iron ore to produce steel for infrastructure and other construction projects. With regard to the supply of iron ore, Brazil, one of the major iron ore exporting nations, is experiencing growing numbers of COVID-19 cases which have partially restricted its ability to mine and ship iron ore, thus creating favorable operating environment for IRC`s K&S project. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $0.16, Target Price: $0.18, Cut Loss Price: $0.15

|

GREATWALL MOTOR(2333)

Analysis¡G

GWM sold 145,000 vehicles in November, a yoy increase of 26.1%; from January to November, it sold 961,000 vehicles, a yoy increase of 0.75%. Cumulative sales were the first to turn positive, which was better than industry and market expectations. Great Wall Motor`s 2020Q3 total income was 26.214 billion yuan, +23.64% yoy; net profit attributable to the parent was 1.441 billion yuan, +2.93% yoy. Mainly due to the exchange loss of 510 million incurred by the devaluation of the Ruble, if this factor is excluded, the actual net profit is 1.95 billion yuan, a strong yoy increase of 39%. In 2021, GWM will list at least 10 new models equipped with new technologies and new power, including fuel version, hybrid version and pure electric version. With the continuous increase of platform products, the Company`s new product cycle is beginning.

Strategy¡G

Buy-in Price: $14.90, Target Price: $19.00, Cut Loss Price: $12.40

|

|

Razer (1337.HK) - Razer failed on SG Digital Banking Bid, but the long-term impact is minimum

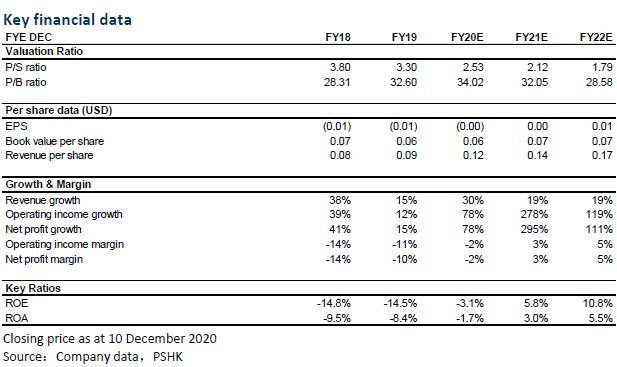

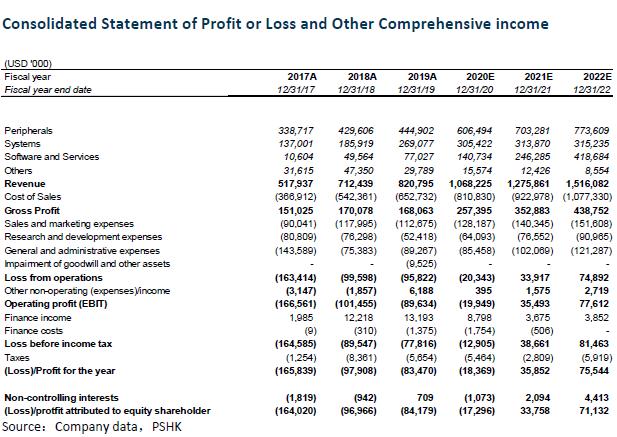

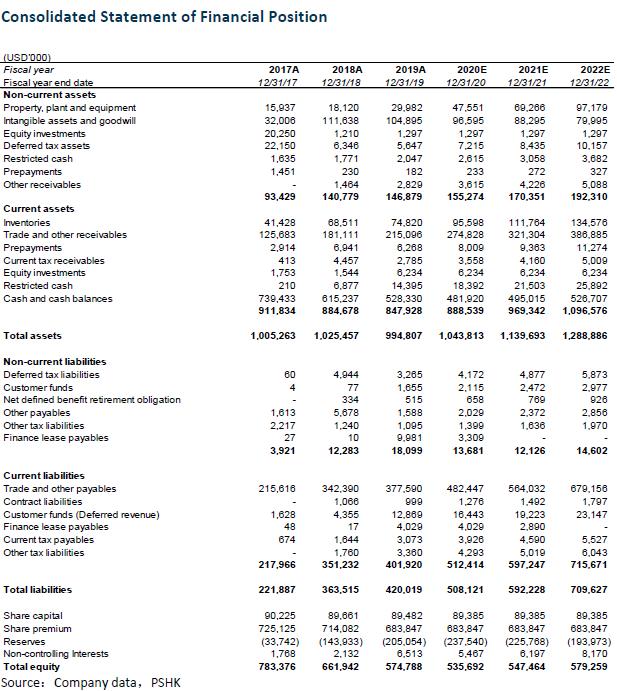

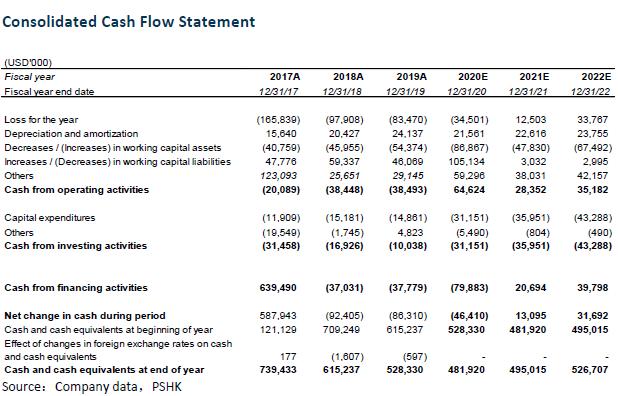

Investment SummaryThe Monetary Authority of Singapore (MAS) announced on December 4, 2020 that four successful digital bank applicants. The Monetary Authority of Singapore expects that the digital bank will be operational as early as 2022. Among four licenses, two are "Digital Wholesale Bank"(DWB) licenses, which are respectively granted to an entity wholly-owned by Ant Group and a consortium comprising Greenland Finance Holdings Group Co.Ltd, Linklogis Hong Kong Ltd, and Beijing Co-operative Equity Investment Fund Management Co. Ltd. The other two licenses are the "Digital Full Bank License", which are granted to a consortium comprising Grab Holding Inc. and Singapore Telecommunications Ltd. (Singtel), and an entity wholly-owned by Sea Limited. Razer (the ¡§Company¡¨) financial technology branch "Razer Fintech" once applied for a Singapore digital bank license, but the first round of the list failed. The Company's management stated that although it failed the Singapore Digital Bank, its long-term development of technology and financial business strategy will be firmly implemented. The management said that regional countries such as Malaysia or the Philippines also have a lot of opportunity. The long-term attractiveness of the Southeast Asian market lies in its demographic advantage. There are about 600 million young people in the region and the region's middle-class population is growing rapidly. Favorable policies such as large infrastructure construction, these factors are conducive to the continued economic growth of the region, and bring huge business opportunities to companies operating in the region. According to e-Conomy SEA, more than a third of consumers are new to digital services in Malaysia and the Philippines which presents a huge market opportunity for us to be the first providers in the area of Fintech and digital financial services for them. We believe that although the Company has failed in the Singapore digital banking license, the Company intend to roll our Razer Youth Bank where Razer and Razer Fintech have already established a strong user base and local business presence, be it in regional countries such as Malaysia and the Philippines where digital banking application processes are expected to kickstart in the near term or other regions, such as Europe, Middle East or Latin America where regulators are similarly supportive of innovation in the banking sector to better serve the unbanked and underserved segments of the economy. It can be seen that the Company's determination to develop financial technology business and the long-term value of Fintech business remained unchanged. Valuation and Investment RecommendationIn summary, we believe that although the Company has failed on the Singapore Digital Banking Bid, it has little impact on its core business operations. The "Home Economy" business continues to grow. In addition, we believe that the Company's determination to develop the Fintech business remains unchanged. Razer relies on its strong brand with more than 100 million fans worldwide, we believe that the Company's financial technology business in other regions can develop rapidly. We maintain the Company's 2020/2021/2022 revenue per share of US $0.12/0.14/0.17, twelve-month target price of HKD3.27, corresponding to 2020/2021/2022 P/S ratio of 3.58x/3.00x /2.52x. We maintain Buy rating.(Exchange rate: 7.78 USD/HKD) (Current price as of 10 December 2020) Risks 1) COVID-19 outbreak again 2) E-sports growth not as expected 3) The Company's products fail to cater the user trends Financial statements

Click Here for PDF format...

| Recommendation on 15-12-2020 | | Recommendation | BUY | | Price on Recommendation Date | $ 2.370 | | Suggested purchase price | N/A | | Target Price | $ 3.270 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2020 Phillip Securities (HK) Ltd. All Rights Reserved.

|