Investment Summary

The main business of Nissin Foods is the production and sale of instant noodles in Hong Kong and Mainland China. The company's products are mainly positioned in the segment of high-end instant noodle markets. The parent company Nissin Japan Group was established in 1948 by Mr. Momofuku Ando, with a market share of over 70% in the Japanese instant noodle market. Nissin Foods was incorporated in Hong Kong in 1984 and expanded its business to the Mainland in 1994.

The company is also actively expanding its product matrix. In addition to self-developing new products, the company acquired the Hong Kong instant noodle brand "Fuku" in 2012. In the same year, "Cup Noodle" and mini cup noodles were launched under the brand "Cup Noodle" to meet the needs of different consumers. The company also acquired Winner Food from Nissin Japan in 2014. Winner Food mainly produces and sells instant noodles and frozen food products under the "Doll" brand. Listed on the main board of the Hong Kong Stock Exchange in 2017. During the period, the non-instant noodle business was expanded through research and development, acquisitions and joint ventures, such as MCMS, Kagome brand and Granola cereal products.

China's convenience food market is stable

With the increasing individualized needs of consumers, companies continue to improve product differentiation, and put forward higher requirements for the research and development of new products, especially the ability to continuously launch new products, and supply chain cooperation. In recent years, the leaders have continued to deploy in the high-end market.

In terms of product portfolio, different from other domestic instant noodle manufacturers who mainly focus on low-end instant noodles and seize market share through low-price strategies, the company's brand's main high-end product positioning helps the company differentiate itself. It helps avoid direct competition with other domestic brands when expanding the mainland market and enter the red sea market.

Valuation and Investment Recommendation

Affected by the epidemic in 2020, the company performed well in the first three quarters, with a YoY growth of 11.6%. The company has a large market share in the Hong Kong market and can maintain a certain level of revenue. However, the company's room of revenue growth is also limited. We expect that after the epidemic returns, revenue will return to normal levels, and subsequent growth will be lower, about LSD growth YoY. On the contrary, the company's market share in China is low, and in an environment where domestic consumption levels are upgrading, the company has a competitive advantage in the high-end instant noodle market. In the past three years, the company's domestic revenue has recorded double-digit growth in CNY and is expected to maintain in the future.

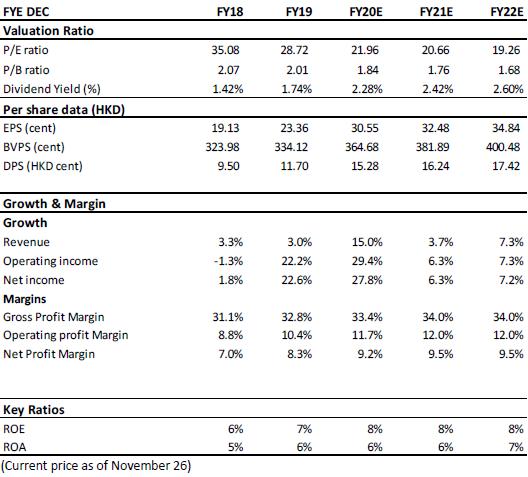

we expect that the company's revenue will record high growth in 2020 and slow down in 2021. We expect that the company's FY20E/FY21E/FY22E net profit attributable to the parent will be 328/349/374 million HKD, and FY20E/FY21E/FY22E EPS will be 30.55/32.48/34.84 cent, giving a twelve-month target price of HKD 8.73, corresponding FY21/FY22 target earnings ratio of 26.88x/25.06x, with a Buy rating.

(Current price as of November 26)

Company Profile

The main business of Nissin Foods is the production and sale of instant noodles in Hong Kong and Mainland China. The company's products are mainly positioned in the segment of high-end instant noodle markets. The parent company Nissin Japan Group was established in 1948 by Mr. Momofuku Ando, with a market share of over 70% in the Japanese instant noodle market. Nissin Foods was incorporated in Hong Kong in 1984 and expanded its business to the Mainland in 1994.

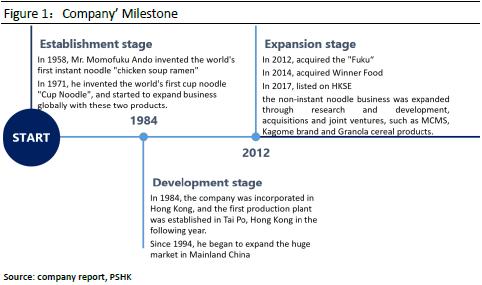

Company development process

The company's development history can be divided into three stages

Establishment stage (1958-1993)

In 1958, Mr. Momofuku Ando invented the world's first instant noodle "chicken soup ramen" and changed the company's name to Nissin Foods Products., Ltd, and began to expand its business all over the world. In 1971, he invented the world's first cup noodle "Cup Noodle", and started to expand business globally with these two products.

Development stage (1994-2011)

In 1984, the company was incorporated in Hong Kong, and the first production plant was established in Tai Po, Hong Kong in the following year. The company successfully seized the Hong Kong market with "Cup Noodle" and "Demae Iccho". Since 1994, he began to expand the huge market in Mainland China, and successively established Nissin in Guangdong, Nissin Shanghai, Nissin Fukujian and Nissin Zhejiang to manage its business in Mainland China.

Expansion stage (2012- current)

The company is also actively expanding its product matrix. In addition to self-developing new products, the company acquired the Hong Kong instant noodle brand "Fuku" in 2012. In the same year, "Cup Noodle" and mini cup noodles were launched under the brand "Cup Noodle" to meet the needs of different consumers. The company also acquired Winner Food from Nissin Japan in 2014. Winner Food mainly produces and sells instant noodles and frozen food products under the "Doll" brand. Listed on the main board of the Hong Kong Stock Exchange in 2017. During the period, the non-instant noodle business was expanded through research and development, acquisitions and joint ventures, such as MCMS, Kagome brand and Granola cereal products.

Company Business

The company's product brand portfolio is diversified, covering a wide range of food categories, including the instant noodle market (including instant cup noodles, bowl noodles and bagged instant noodles); frozen food (mainly including frozen snacks and frozen noodles); and other foods (Including retort pouch products and snack products)

At the beginning of its establishment, the company mainly focused on instant noodle business. Since the company started its business in Hong Kong early, its image has become popular among the people after years of intensive cultivation, and it has taken a leading position in the instant noodle market in Hong Kong. The company's market share in the Hong Kong market exceeds 60%. The company also expanded its product matrix by acquiring Hong Kong brands. In 2012 and 2014, the company acquired the Hong Kong instant noodle brand "Fuku" and the Winner Food from Nissin of Japan.

The company's flagship products include "Cup Noodle" and "Demae Iccho". "Cup Noodle" is the company's flagship brand of cup noodle products. Since its first launch in 1984, it has been widely praised for its excellent quality and taste and has become Hong Kong people's impression of cup noodles. symbols of. "Demae Iccho" focuses on bagged instant noodles, targeting the mass and family markets. It is popular with Japanese raw materials combined with Hong Kong manufacturing. In recent years, in addition to the two flagship products, the company has also launched new product series such as "Ippudo" and "Nissin Raoh", a total of more than ten brands. The continuous launch of innovative products has enabled the company to maintain its leading position in the instant noodle segment.

Frozen food

The company entered the frozen food market under the brand "Doll Dim Sum" in 1990. In 2014, it further acquired Winner Food from Nissin of Japan, and extended its brands such as "Eatwell" and "Ho e Sik". Later, the company also launched frozen udon and dumplings under the main brand "Nissin". Based on its previous experience in the frozen food market, the company expanded its new products and positioned it in the high-end organic product market.

Other products

After the company expanded its non-instant noodle business, in 2018, it started operating in a joint venture with Kagome Co Ltd. to distribute "Kagome" brand vegetable juice and fruit juice beverage products in Hong Kong. The company invested HK$35 million and owned 70% of the entity rights and interests. In addition, the company also invested HK$30 million to set up a new ¡§Granola¡¨ grain production line in Tai Po, Hong Kong in 2018. The company also sells other products including retort pouch products, wagashi and potato chips.

Other business

In addition to the food production business, the company completed the acquisition of 51% equity in MCMS in 2017 and began to conduct distribution business in Hong Kong and Macau through MCMS, mainly through distribution to retailers and other direct customers. Its agency brands are not only included Nissin products, also includes beverages, sauces and processed foods from other brands such as EVIAN, VOLVIC and Kewpie. The company's distribution experience in MCMS also provides guidance for its expansion of domestic distribution channels in China. In January 2020, the company established a joint venture company in Shanghai, mainly engaged in the import and sale of Japanese branded food and beverage products.

Production

In terms of production lines, the company currently has 9 production plants, four of which are located in Hong Kong, while the other five are located in Shunde, Zhuhai, Dongguan, Xiamen and Pinghu. Among the four factories in Hong Kong, two are responsible for the production of instant noodles, one is responsible for the production of frozen food and the other is responsible for the production of packaging materials and grain products.

Industry analysis

China's convenience food market is stable

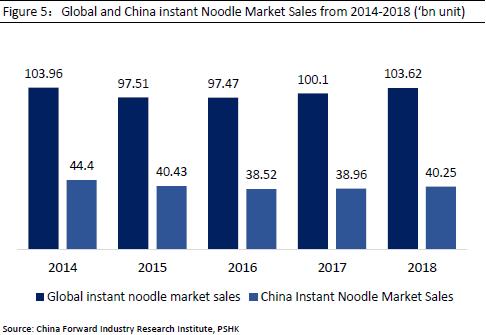

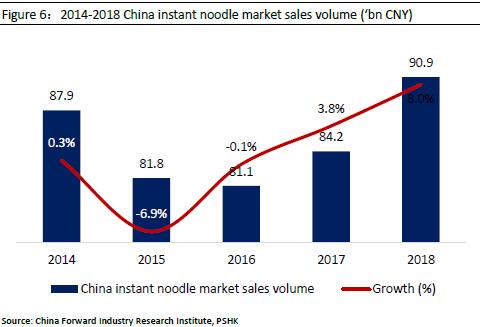

In 2019, the market size of China's convenience food industry is expected to exceed RMB 450 billion, of which the instant noodle market is approximately RMB 100 billion. Under the epidemic situation, the sales of instant noodles have skyrocketed, As China is the world's largest convenience food market, its market has not progressed steadily like other countries. It has declined since 2015. In the past two years It also rebounded slightly, and the market is gradually picking up. According to a report from the China Forward Industry Research Institute, China's instant noodle market sold 44.4 billion units in 2014, and it began to decline gradually in 2015. By 2016, 38.52 billion units were sold, which was nearly 5 billion units. Beginning in 2018, China's instant noodle market sales have rebounded significantly. In 2019, China's instant noodle sales are expected to rebound back to 2014 levels. Similar to the changing trend of instant noodle sales, the retail sales of instant noodles also continued to rise. According to Nielsen data, in 2018, the overall convenience market sales grew 3.2% year-on-year, and sales grew 8.0% year-on-year.

Consumption upgrade, high-end has become the development direction of the industry

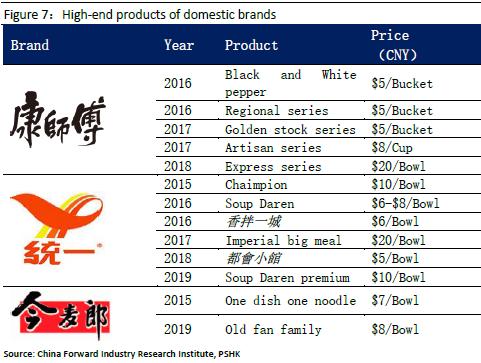

With the increasing individualized needs of consumers, companies continue to improve product differentiation, and put forward higher requirements for the research and development of new products, especially the ability to continuously launch new products, and supply chain cooperation. In recent years, the leaders have continued to deploy in the high-end market. Since 2015, leading companies such as Master Kong and Uni-President have continued to deploy high-end instant noodles priced at RMB 5 or more. Master Kong has successively launched high-end products such as black and white pepper series, regional flavors, golden soup series, and super high-end products represented by Express Noodles. The ¡§Soup Daren¡]´ö¹F¤H¡^¡¨ under Uni-President have a large market share. Jinmailang also launched one-dish noodles in 2015, and later launched old Fan family instant noodle.

Hong Kong and China instant noodle market distribution channels

Hong Kong and China instant food manufacturers usually sell their products through four channels, namely traditional trade channels (including individual or family-owned and operated grocery stores that usually sell groceries, non-chain convenience Stores and other sales outlets), modern retail channels (including shopping malls, supermarkets and chain convenience stores generally located in central areas of large cities and smaller cities operated by group companies), special channels (including catering, air transportation, and Internet Coffee shops, gas stations and KTV) and e-commerce channels.

Online and offline pipelines are equally important and indispensable. Online consumers are mostly those in high-tier cities, with a relatively high proportion of young people; consumers are more likely to be driven by content marketing. The closed loop of e-commerce data is complete, allowing companies to quickly test and adjust products and marketing methods, and it is easy to produce "hit products". The immediacy of offline channels is a natural scenario for convenient food sales. However, the Chinese market is vast, the offline pipelines are widely distributed, the distribution system is complex, and the construction and operation of offline channel is a time-consuming and labor-intensive part of the brand, and it is also a test and inspection of the team's operational capabilities.

The rise of takeaway platforms has become a major challenge in the instant noodle market

From 2015 to 2016, with the rapid development of the mobile Internet, domestic and foreign takeaway platforms such as Ele.me and Meituan rose rapidly. Their use of price subsidies to obtain the market prompted takeaway to become one of the important lifestyles of the masses. Fresh, fast and delicious takeaways gradually replaced "junk food" instant noodles in consumers` hearts, leading to a decline in the overall industry sales of instant noodles.

However, in the past two years, the food delivery market has gradually entered a mature stage of oligopoly competition. Its ¡§burning subsidy¡¨ model is unsustainable. The average price of food delivery has also been rising. It has gradually withdrawn from the market of 10-20 yuan. The online food delivery industry market The scale growth rate has gradually slowed down; coupled with the food safety issues of takeaway platforms that have been gradually exposed in the past two years, instant noodles that are cheap, fast, rich in variety, better taste, and mature in industrial production have naturally become the first choice to fill the gap in the takeaway market. Get the favorite of consumers.

Company competitive advantage

In terms of product portfolio, different from other domestic instant noodle manufacturers who mainly focus on low-end instant noodles and seize market share through low-price strategies, the company's brand's main high-end product positioning helps the company differentiate itself. It helps avoid direct competition with other domestic brands when expanding the mainland market and enter the red sea market. The company's well-known Cup noodle and Demae Iccho products are positioned at high-end, with an average product price of about 5-10 yuan. The high-end brand images are deeply rooted in the hearts of the people, thus cutting into the expanding high-end instant noodle market in the Mainland. The company is the only domestic manufacturer that only deploys high-end instant noodles. Unlike major domestic competitors such as Master Kong and uni-president multi-price strategy, the company's rich experience in high-end product development helps the company to take advantages in high-end instant noodle market.

In the Hong Kong market, the company has a leading position in the instant noodle market. Future growth cannot rely solely on existing products. The company continues to develop new products in addition to the original products, and brings growth to the company by enriching the product matrix. For instant noodle products, the company continues to develop innovative flavors and improve the quality of instant noodles. In addition, the company is also committed to the development of non-instant noodle business, including cereal products, Kagome brand products, potato chips and other products. In addition, with different market positioning, the company also uses the Hong Kong market as a testing ground when launching new products and businesses, conducts preliminary tests, and introduces products to the Chinese market after adjustments.

Financial Analysis

Revenue analysis

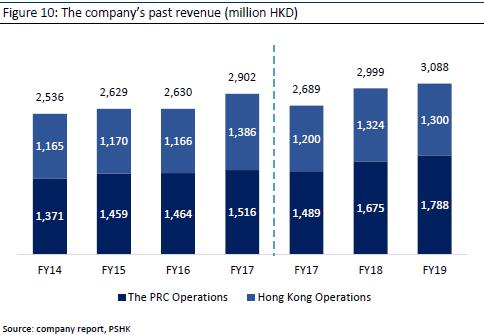

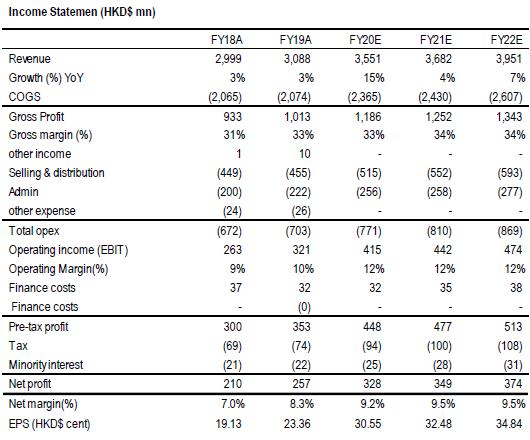

The company's revenue has increased steadily in the past four years, increasing at a CAGR of 4.02%, from HK$2.54 billion in 2014 to HK$3.09 billion in 2019. The business segmentation is mainly divided by region. The China business and the Hong Kong business contribute similarly to revenue, and the proportion of revenue from the Chinese business has been increasing in recent years. In FY19, revenue from China business accounted for 59.2% of total revenue, an increase of approximately 5.1 pct from FY14.

�

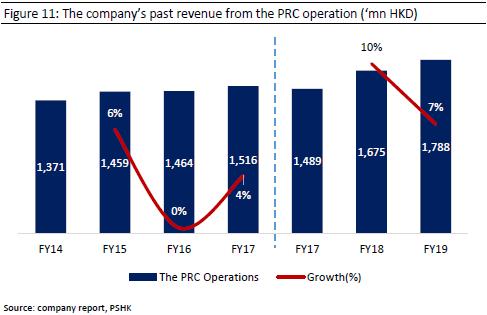

In terms of geographic breakdown, revenue from China business has increased YoY, from HK$1.37 billion in FY14 to HK$1.79 billion in FY19, an increase of nearly 30.4%. If calculated in local currency, the company achieved double-digit revenue growth in FY18 and FY19. If converted to Hong Kong dollars, the company's FY19 revenue from China operations increased by 6.7% from FY18's HK$1.68 billion to FY19's HK$1.79 billion. Mainly due to channel expansion in southern, northern and western China. The original main operation in East China has also expanded to markets such as Shanghai.

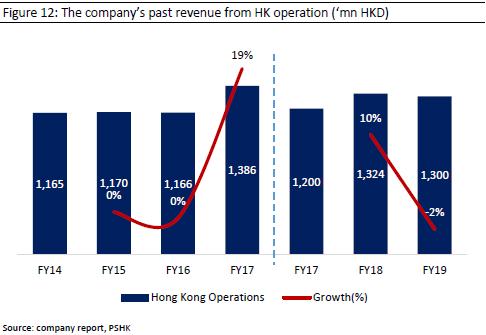

The company's income from Hong Kong business is relatively stable, mainly due to the company's high market share in the Hong Kong market and hence limited revenue growth. The company recorded HK$1.39 billion in FY17, an increase of nearly 18.9% compared to FY16. Contribution to revenue from the acquisition of MCMS 's distribution business in March 2017. However, in 2019, due to changes in the product portfolio of Hong Kong MCMS 's distribution business, the distribution of some products was terminated, resulting in a decline in revenue.

Profitability

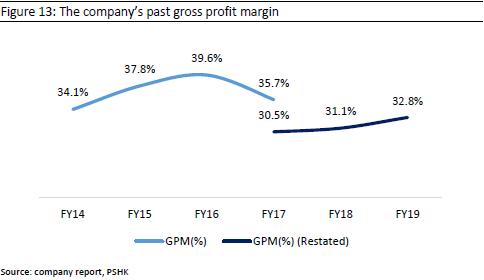

The company's GPM continued to increase from FY14 to FY16, from 34.1% in FY14 to 39.6% in FYF16, mainly due to the impact of raw material prices and self-produced packaging materials, which led to a reduction in the purchase of packaging materials. After the company acquired MCMS in 2017, due to the low GPM of the distribution business, it has a negative impact on the company's GPM after being consolidated to company, with a year-on-year decrease of 4 pct.

In addition, since January 1, 2018, the company began to apply HKFRS 15, regarding sales rebates as part of transaction costs and reduce the company's revenue, which is different from the company's past recognition of customer sales rebates is sales expense. After restating the 2017 GPM, the company's GPM began to gradually recover in 2018, increasing by 2.3pct from 30.5% (restated) in 2017, mainly due to fixed cost control of depreciation and indirect costs of production plants.

Expenses for the period

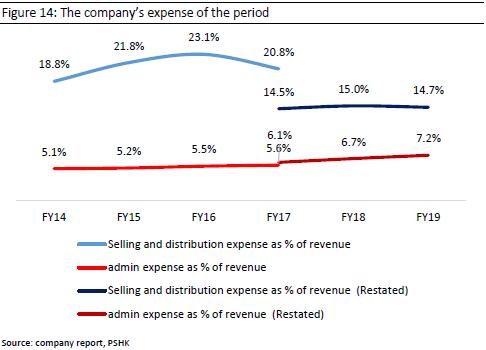

In the company's sales and distribution costs, promotion costs account for most of them, followed by salaries and allowances, freight and storage. While expanding sales channels, the company's sales and sales costs are also rising. In FY17, due to the company's acquisition of MCMS, the revenue contributed did not incur additional distribution costs, and the proportion of S&D expenses to revenue decreased by 2.3 pct to 20.8%. In addition, after the company applied HKFRS 15, sales rebates were not included in the distribution expenses. After the restated, the sales expense ratio in FY17 was 14.5%, which was maintained at a similar level in FY17-FY19. In terms of administrative expenses, the company's administrative expenses have continued to rise in the past six years, mainly due to recruitment while expanding its business.

Forecast and Company valuation

Affected by the epidemic in 2020, the company performed well in the first three quarters, with a YoY growth of 11.6%. The company has a large market share in the Hong Kong market and can maintain a certain level of revenue. However, the company's room of revenue growth is also limited. We expect that after the epidemic returns, revenue will return to normal levels, and subsequent growth will be lower, about LSD growth YoY. On the contrary, the company's market share in China is low, and in an environment where domestic consumption levels are upgrading, the company has a competitive advantage in the high-end instant noodle market. In the past three years, the company's domestic revenue has recorded double-digit growth in CNY and is expected to maintain in the future.

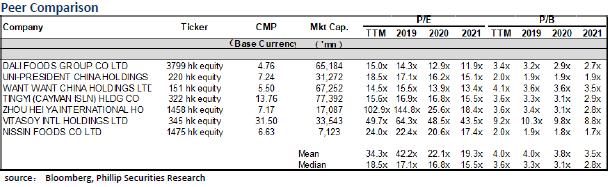

The company's main competitors in the industry are Uni-President Foods and Master Kong. Unlike major domestic competitors that have established a stable position in the domestic market and are expected to grow at a relatively low level in the future, Nissin Foods is still in its infancy in China, and its business is expected to maintain a low double-digit growth. In the past, the company's average valuation was 26.24x earnings ratio, which was higher than the industry average. The current price corresponds to the FY2020E earnings ratio of approximately 21.96x, which is lower than the previous average.

�

Absolute valuation method

We divide the company's future into two phases:

The first stage: the company continues to expand in China business, maintains LDD growth

The second stage: enter the stage of continuous growth.

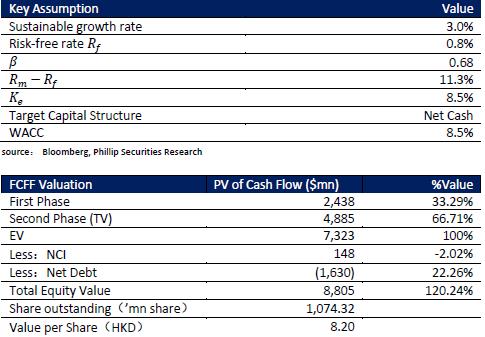

Key assumptions:

1. Sustainable growth rate: We expect the long-term growth rate to be 3.0% after the company enters a stable growth stage

2. Risk-free Rate: Hong Kong 10-year government bond yield level

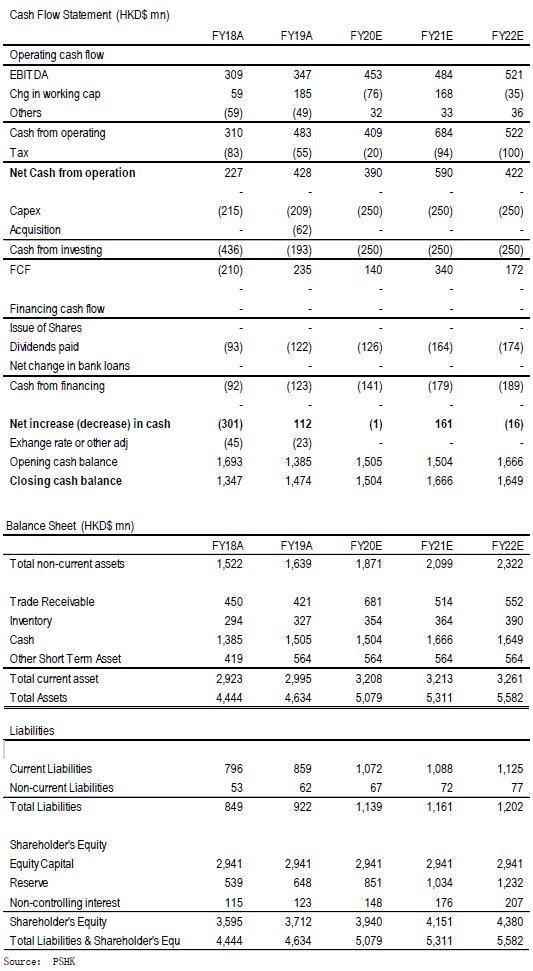

According to the absolute valuation method, we believe that the company's current intrinsic value per share is $8.20, and the current stock price is below a reasonable level.

In summary, we expect that the company's revenue will record high growth in 2020 and slow down in 2021. We expect that the company's FY20E/FY21E/FY22E net profit attributable to the parent will be 328/349/374 million HKD, and FY20E/FY21E/FY22E EPS will be 30.55/32.48/34.84 cent, giving a twelve-month target price of HKD 8.73, corresponding FY21/FY22 target earnings ratio of 26.88x/25.06x, with a Buy rating.

(Current price as of November 26)

Financials

Click Here for PDF format...