Investment Summary

Archosaur Games is a leading mobile game developer in China

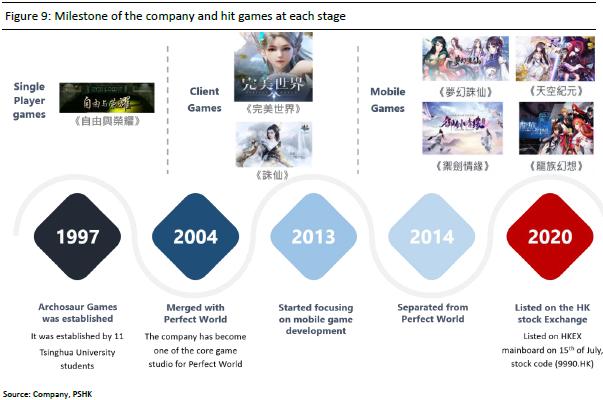

Archosaur Games was established in 1997, and is a leading mobile game developer in China. The company has intensive experience in developing web games, client games and mobile games. The company was once merged with Perfect world (A-shares) in 2004 and has become its core game studio. After the merger, the company started focusing on MMORPG games development and has developed multiple hit games such as Perfect World (§¹¬ü¥@¬É) and Zhuxian (¸Ý¥P). The company has begun to deploy in the field of mobile games in 2013 and was separated from Perfect World in 2014. Since 2014, the company has successively launched popular MMORPG games domestically/ globally, such as Fantasy Zhuxian (¹Ú¤Û¸Ý¥P), Love & Sword (±s¼C±¡½t), The Castle in the Sky (¤ÑªÅ¬ö¤¸), Dragon Raja (Às±Ú¤Û·Q) .

The company is a leading MMORPG game developer in China

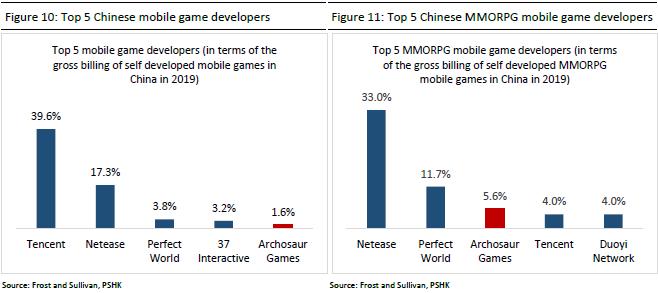

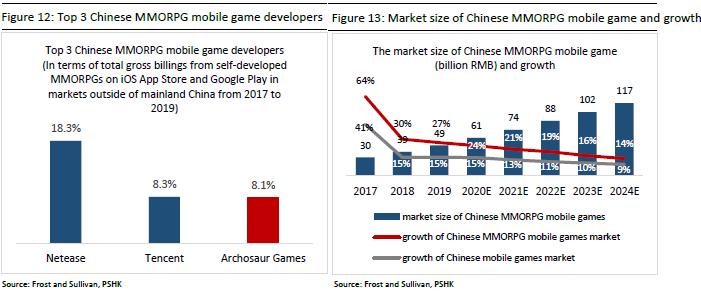

The company has strong game development capabilities, especially in MMORPG games. According to Frost and Sullivan, in terms of the total gross billings from self-developed MMORPGs in mainland China in 2019, the company actually ranks 3rd in the country, with market share of 5.6%. It is only slightly behind Netease's 11.7% market share and is higher than Tencent's market share of 4.0%. The company's hit game Dragon Raja (Às±Ú¤Û·Q) also has the highest MAUs in China in 2019. The above data and figures can clearly show that the company is one of the market leader in the MMORPG game sector.

The company's mobile game reserve

The company has ample reserves of game projects, and currently there are 8 games in the development stage. Among them, 3 of them are SLG strategic games. The growth potential of SLG genre game market is huge. The company's business expansion to SLG game genre can potentially become a huge growth driven in the future and can also enrich the game categories of the company's game portfolio for new user expansion. We believe that MMORPG games are more difficult to develop than SLG games as well as there are many similarities between two game genres from the R&D perspective. Therefore, we expect that the company's professional R&D team to be competent in the development of SLG games.

The first to successfully introduce UE4 into mobile game development in China

The company is one of the first developers to successfully introduce Unreal Engine 4 into China's mobile game development industry and conduct secondary development. The game Dragon Raja (Às±Ú¤Û·Q) in 2019 is China's first true 3D MMORPG mobile game powered by the Unreal Engine 4. The company spends significant resources of R&D and its R&D expenses ratio is among the top comparing to its peer. The company's strong mobile game R&D capabilities and high R&D investments have created a strong economic moat for the company and enables the company to survive and grow in the gradually refined Chinese mobile game sector.

Valuation

The company has a leading advantage in MMORPG games genres and has constituted a strong economic moat. The company has already laid a solid foundation in MMORPG games genres and is starting is expand businesses to SLG game genres (MMORPG and SLG are the two games genres with the highest growth potential). The target price of Archosaur Games is HKD 33.6, corresponds to 2020/2021 adjusted PE of 38.1x/22.0x PE. We are initiating with a ¡§Buy¡¨ rating.

Industry Review and Forecast

The mobile game market has the highest growth potential in Chinese game market

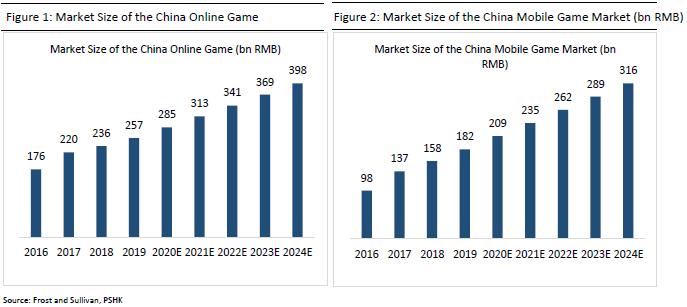

Since 2015, China has been the world's largest market of online games in terms of gross billings. One of the main reasons for the boom of China's online game market was the intensified demand for entertainment. According to Frost and Sullivan, China's online game market reached a size of RMB257 billion in 2019, and is expected to reach RMB398 billion in 2024, representing a CAGR of 9.1%. With the advancement of hardware and internet technology, the graphics, content and response speed of online games are being constantly upgraded, the development of online games are more tailored to player preference. Mobile game sector is the main sub-segment in the game sector with its growth higher than other sub-segments (client game sub-segment and web game sub-segment). China's mobile game market expanded from RMB98 billion in 2016 to RMB181.7 billion in 2019, and is expected to reach RMB316 billion in 2024, representing a CAGR of 11.7%. We believe that with the ongoing development of gaming online broadcast and the e-sport industry, as well as the increase proportion of mobiles in population, the mobile game sub-segment is likely to slowly replace the other sub-segments.

The size of the game market in the rest of the world

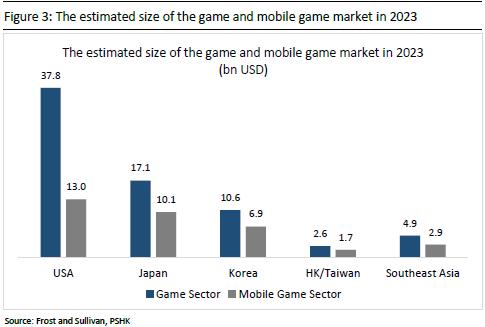

The United States had the second largest game market by revenue in the world in 2018. According to Frost & Sullivan, the size of the U.S. game market has reached USD 28.7 billion in 2018, and the size of the mobile game segment is about USD 9 billion. It is estimated that in 2023, the size of the online game market and the mobile game market will reach USD 37.8 billion and USD 13 billion respectively, with a CAGR of 5.7% and 7.5% in 2018-2023. In addition to the United States, the Asian mobile game market is also expected to continue to grow in the future. According to Frost & Sullivan, the 2018-2023 CAGR of the mobile game market size of Japan/Korea/Hong Kong and Taiwan/Southeast Asia are 6.5%/ 7.4%/ 10.6%/ 11.5% respectively.

The market for PRC Mobile Games Overseas

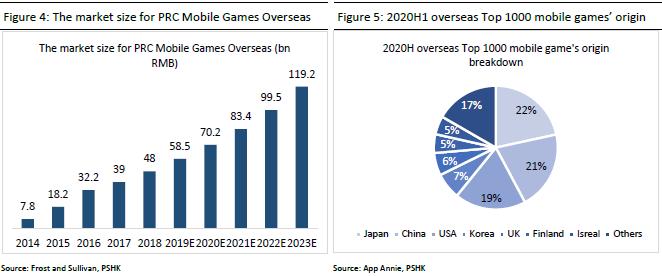

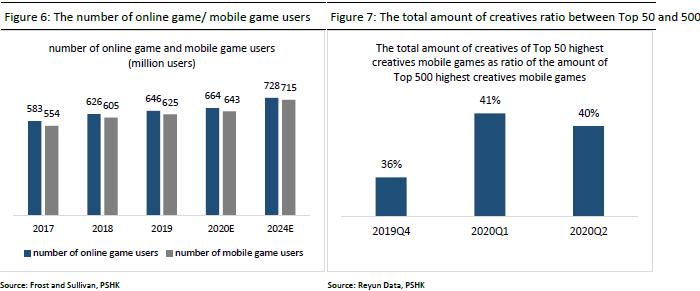

In recent years, many mobile game companies have been focusing on their overseas market business, mainly because the mobile game markets in many overseas regions (especially Southeast Asia) are still in the early stage of development and has great growth potential. In contrast, the Chinese mobile game market is already in the mature stage and its growth has significantly slowed down. Secondly, the Chinese game market is indeed hugely affected by policies. Relevant national departments issued a number of game supervision measures (including tightening supervision on underage gamers and restricted their game time) in 2018-2019, and suspended the pre-approval for games in 2018. Although the current pre-approval procedure has resumed, nonetheless there are still significant policy risks in China's mobile game market. On the contrary, games in majority of overseas markets are only supervised through the "game classification system", where games are classified by the age of suitable players. It can be seen that the regulatory intensity of the overseas game market is obviously lower than that of the Chinese market. As a result, expanding overseas markets will help Chinese mobile game industry participants to reduce this policy risk. According to Frost & Sullivan, the China's overseas mobile game market recorded a significant growth at a CAGR of 57.5% from 2014 to 2018, and is expected to grow at a CAGR of 20.0% from 2018 to 2023. The Chinese mobile games have already achieved good results in overseas market. According to the statistics of the Overseas Research Institute (®ü¥~¬ã¨s°|), in the US Google Play Store Top 100 free list and Top 100 best-selling list, apps from China have occupied 15 and 20 places respectively. Further, there are 30 Chinese mobile games in the Top 100 best-selling Korean mobile games in 2019. Further, according App Annie data, the market share of Chinese mobile games in overseas markets was up by 2.9ppt yoy in 1H20, and reached 21.2%, which is only slightly behind Japan with 21.5%.

The Chinese game advertisement market

In recent years, the growth of users in the Chinese game market has gradually been slow. According to Frost & Sullivan, the CAGR of Chinese gamers/mobile game players from 2019 to 2024 is expected to be 2.4%/2.7%. In 1H20, even under the impact of COVID and quarantine, the growth of users remained slow. According to the ¡§China Game Industry Report for January-June 2020¡¨ ¡m2020¦~«×1-6¤ë¤¤°ê¹CÀ¸²£·~³ø§i¡n, the number of gamers in China in 1H20 was 557 million, a yoy increase of only 1.97%. As the growth of number of Chinese gamers begins to slow down, the difficulty of acquiring customers for game companies has increased. On the other hand, according to Reyun data, the total amount of creatives of the Chinese TOP 50 highest creatives mobile games have accounted for roughly 41%/40% of the total amount of creatives of the Chinese TOP 500 highest creatives mobile game in 20Q1/20Q2, up by 5ppt/4ppt comparing to the 36% in 19Q4. The increase in this proportion means that the Chinese game advertisement market is gradually dominated by the market leaders. According to DataEye-ADX, the Game ¡m¶Ã¥@¤ýªÌ¡nby Tencent ranked 13th on the ranking of highest creatives Chinese game. This is relatively surprising, since the games developed by Tencent don`t usually appear in the Chinese game advertisement markets, as they are usually promoted and advertised through the diversified advertisement channels of Tencent. This served as a clear evidence that the market leaders have begun to enter the Chinese game advertisement market. The combination of the increasing customer acquisition difficulties as well as the fact that the market leaders begin to enter the Chinese game advertisement market have driven the cost of game advertisement upward significantly.

Developing exquisite games by enhancing R&D capabilities is the general trend in the sector

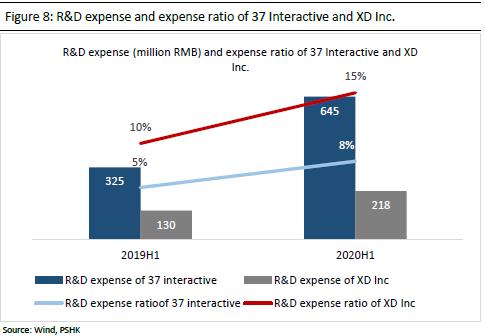

Game development capabilities and game quality have become particularly important especially in the background of high game advertisement cost. The increase in game advertisement cost will squeeze the living space of non-exquisite games on the one hand, and on the other hand, it has shifted the attention of mobile game developers onto the quality of games in order to acquire customers and retain them, rather than spending significant amount on advertisement. In addition, as players consume more and more rationally, whether mobile game companies can tap the value of its existing users by providing high-quality games will become the key. Further, pre-approval of games by Chinese Government are more stringent than ever. This has further pushed game companies to refine their games in order to increase the games` life cycle to cope with the increasingly stringent pre-approvals. The above reasons have promoted high quality and refinement of the mobile game industry and we believe that that increasing their R&D capabilities will be the only way for mobile game companies to survive. Take 37 Interactive Entertainment (A-shares) and XD Inc (HK-listed) as example, the R&D expense of 37 interactive and XD in 1H20 were RMB 645/218 million, up by 99%/68%. The corresponding R&D expense ratio were also up by 2.7ppt/5.5ppt.

Company Overview and its Competitive Advantages

Archosaur Games is a leading mobile game developer in China with more than 20 years of game developing experiences

Archosaur Games was established in 1997, and is a leading mobile game developer in China. The company has intensive experience in developing web games, client games and mobile games. The company was once merged with Perfect world (A-shares) in 2004 and has become one of its core game studios. After the merger, the company started focusing on MMORPG games development and has developed multiple hit games such as Perfect World (§¹¬ü¥@¬É) and Zhuxian (¸Ý¥P). The company has begun to deploy in the field of mobile games in 2013 and was separated from Perfect World in 2014. Since 2014, the company has successively launched popular MMORPG games domestically/ globally, such as Fantasy Zhuxian (¹Ú¤Û¸Ý¥P), Love & Sword (±s¼C±¡½t), The Castle in the Sky (¤ÑªÅ¬ö¤¸), Dragon Raja (Às±Ú¤Û·Q) . Up to now, the company's actual controller is the company's founder, Mr. Li Qing, who holds a total of 29.0% of the equity. Perfect World and Tencent are the company's second and third largest shareholders, respectively.

The company is a leading MMORPG game developer in China

The company has strong game development capabilities, especially in MMORPG games. According to Frost and Sullivan, the company is the 5th largest Chinese mobile game developer in China in terms of total gross billings from self-developed games in mainland China in 2019, with market share of 1.6%. However, in terms of the total gross billings from self-developed MMORPGs in mainland China in 2019, the company actually ranks 3rd in the country, with market share of 5.6%. It is only slightly behind Netease's 11.7% market share and is higher than Tencent's market share of 4.0%. On the other hand, in terms of the total gross billings from self-developed MMORPGs on iOS App Store and Google Play in markets outside of mainland China from 2017 to 2019, the company ranks 3rd as well in the country, with market share of 8.1%, just slightly behind Netease and Tencent. The company's hit game Dragon Raja (Às±Ú¤Û·Q) also has the highest MAUs in China among all other MMORPG games in 2019. The above data and figures can clearly show that the company is one of the market leader in the MMORPG game sector. Since its establishment, the company has totally launched 14 games and all 14 of them are self-developed with majority of them being MMORPG games. Among them, 5 of them were hit games with total gross billing over RMB 100 million in the first month since launched. These 5 games are Fantasy Zhuxian (¹Ú¤Û¸Ý¥P), The Castle in the Sky (¤ÑªÅ¬ö¤¸), Loong Craft (¤»Àsª§ÅQ/¤»Às±s¤Ñ), Legend of Nine Tails Fox («C¥Cª°¶Ç»¡) and Dragon Raja (Às±Ú¤Û·Q). The first month total gross billing of Dragon Raja (Às±Ú¤Û·Q) was even as high as RMB 600 million (Set a new high in company history). According to Frost and Sullivan, MMORPG games has the highest market share in China among all other game genres and also has the highest growth potential in the future. The expected CAGR from 2019-2024 is 19.7%, way higher than the 11.7% CAGR of the average in the mobile game industry in the same period. Further, MMORPG games also has higher-than-average life cycles, highest ARPU and highest Pay user conversion rate comparing to other mobile game genres. The company is expected to become the main beneficiaries of the high future growth in MMORPG mobile game sector because of the company's forward looking and deep cultivation in the field of MMORPG games.

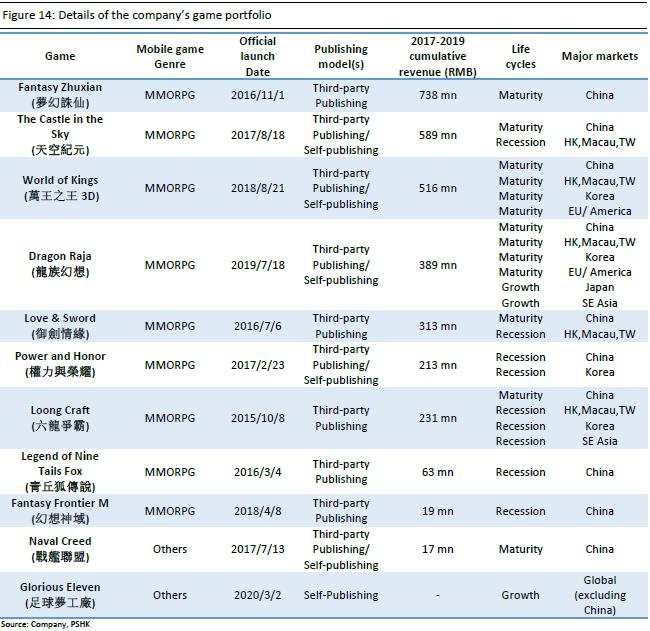

The company's current mobile game portfolio.

As of 30th of June 2020, the company has 11 self-developed games, 9 of them are MMORPG games. The company has achieved a number of ¡§firsts`` in China's mobile game industry. The company has launched one of the first real 3D mobile MMORPG grand strategy wargames, Loong Craft (¤»Àsª§ÅQ/¤»Às±s¤Ñ), and China's first next-generation real 3D mobile MMORPG powered by Unreal Engine 4, Dragon Raja (Às±Ú¤Û·Q). The company has also launched one of the pioneering real 3D turn-based mobile MMORPGs, Fantasy Zhuxian (¹Ú¤Û¸Ý¥P). All of these ¡§firsts¡¨ have fully demonstrated the high R&D capabilities of the company in MMORPG game genre.

Fantasy Zhuxian (¹Ú¤Û¸Ý¥P)

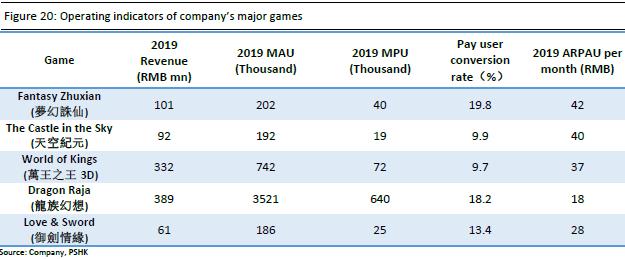

Fantasy Zhuxian (¹Ú¤Û¸Ý¥P) is one of the pioneering real 3D turn-based mobile MMORPGs powered by Unity 3D. It was launched on the 1st of November, 2016. Acclaimed among turn-based game players, it ranked among the top 15 on the Top Grossing Games Chart of the iOS App Store in mainland China for four consecutive months following launch. In 2017, the game has MAU/MPU of 1.2million and 269 thousand. As of the end of 2019, the game has a cumulative gross billings amount of RMB 3.3 billion. The game has contributed revenue of RMB 463/174/101 million in 2017/2018/2019. The 2019 average MAU/MPU were 202/40 thousands, with pay user conversion ratio of 19.7%. The 2019 average ARPAU per month was RMB 42.

Dragon Raja (Às±Ú¤Û·Q)

Dragon Raja (Às±Ú¤Û·Q) was launched on the 18th July 2019 and it was the China's first next-generation real 3D mobile MMORPG powered by Unreal Engine 4. The company sourced the IP of the fiction, Dragon Raja (Às±Ú), which enjoys a significant fan base, and adapted it to form the game's main storyline. Dragon Raja (Às±Ú¤Û·Q) ranked first among all mobile MMORPGs in terms of average MAUs in mainland China in 2019, ranked first on the Top Free Games Chart of the iOS App Store in mainland China on the first day of launch in July 2019 and ranked first on the Top Grossing Games Chart of the iOS App Store in mainland China for the entire week after launch. Besides that, the company has self-published the game in overseas market and has also achieved brilliant results. On the first day the company published a new regional version of the game in the Americas and Europe in 2020, it ranked first among mobile MMORPGs and second among mobile RPGs based on iOS App Store downloads in the United States and sat among the top ten mobile games based on iOS App Store downloads in eight regional markets in Europe. Further, Dragon Raja (Às±Ú¤Û·Q) is the first Chinese mobile MMORPG to top the Top Free Games Charts of both iOS App Store and Google Play Store in Japan. In addition, the game has topped the Top Free Games Charts of both iOS App Store and Google Play in Thailand for eight consecutive days as well as the Top Free Games Chart of Google Play in Singapore for nine consecutive days. By leveraging the brilliant performance of the game in overseas market, the company has reached the App Annie Top 30 Chinese mobile game company ranking for the first time in terms of oversea revenue in June 2020. As of the end of 2019, the company's cumulative total gross billing amount was RMB 1.34 billion, and has contributed a total of RMB 389 million in 2019. The 2019 average MAU/MPU were 3.52 million/639 thousand, with pay user conversion ratio of 18.2%. The 2019 average ARPAU per month was RMB 18. The company is expected to launch a new regional version of such game in Vietnam in 20H2.

Kings/World of Kings (¸U¤ý¤§¤ý3D)

King of Kings/World of Kings (¸U¤ý¤§¤ý3D) was launched 21st of August 2018 and is a mobile MMORPG powered by Unity 3D. The game is available in five regional versions supported in Simplified Chinese, Traditional Chinese, Korean, English, German, Russian, Thai and Indonesian. It once ranked first on the Top Free Games Chart of the iOS App Store in mainland China on the first day of launch and won the Best Original Mobile Game of 2018 Golden Plume Award. The game has contributed revenue of RMB 184/332 million in 2018/2019. The 2019 average MAU/MPU were 742 /72 thousand, with pay user conversion ratio of 9.7%. The 2019 average ARPAU per month was RMB 37.

The company's mobile game reserve

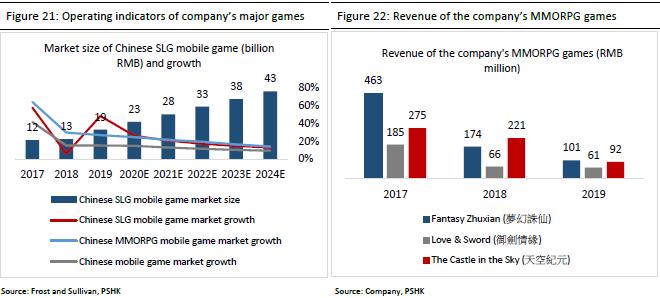

The company has ample reserves of game projects, and currently there are 8 games in the development stage. Among them, 3 of them are SLG strategic games. The growth potential of SLG genre game market is huge. According to Frost and Sullivan, the CAGR of SLG game market is 18.1% from 2019-2024, which is only slightly below the 19.1% CAGR of MMORPG. The company's business expansion to SLG game genre can potentially become a huge growth driven in the future and can also enrich the game categories of the company's game portfolio for new user expansion. Besides that, as comparing to MMORPG genre games, the SLG genre games tend to have longer life cycles and more stable gross billing. Although MMORPG genre games have huge gross billing in early stages, but the gross billings and revenue tend to fall hugely in maturity stages (as shown in figure 22). Hence, the inclusion of SLG game genre to the company's game portfolio can help increase the stability of future revenue. We believe that MMORPG games are more difficult to develop than SLG games as well as there are many similarities between two game genres from the R&D and the core playstyles perspectives. In addition, the core members of the R&D team of the SLG games are all experienced players and experts in SLG games. Therefore, we expect that the company's professional R&D team to be competent in the development of SLG games.

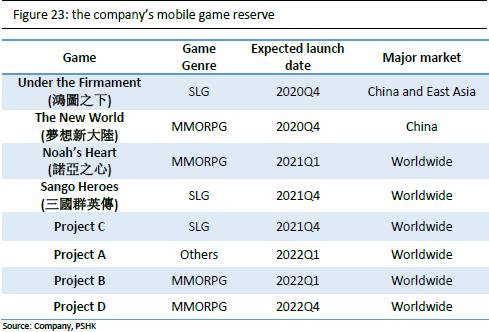

On the other hand, the company is expected to launch Under the Firmament (ÂE¹Ï¤§¤U), The New World (¹Ú·Q·s¤j³°) and Noah's Heart (¿Õ¨È¤§¤ß) in 2H20 and 1H21. Regarding the domestic publishing of these 3 games, the company has already reached agreements with Tencent and Tencent will be responsible for all these 3 games publishing in Mainland China. This has once again proven the high recognition of the company's R&D capabilities from the market leader Tencent. On the other hand, apart from The New World (¹Ú·Q·s¤j³°), which is expected to be released in the second half of 2020, all other games will be self-published by the company in overseas markets. We expect the company's oversea revenue contribution will increase further in future.

Under the Firmament (ÂE¹Ï¤§¤U)

Under the Firmament (ÂE¹Ï¤§¤U) is the first mobile SLG powered by the Unreal Engine 4. The game is based on the settings of the Three Kingdoms of ancient China. Unreal Engine 4 technology has broken through the gorgeous visual effects that many SLG games could not show before (including the realistic weather system, the exquisite design of characters/clothing weapons), with the aim to create a real and magnificent Three Kingdoms War setting for users. Hence, the game is expected to give gamers an unprecedented innovative experience while adhering to SLG's traditional gameplay. The game currently scores 8.9/10 on TapTap platform with the number of reservation exceeds 63,500. We can see that there are plenty of Strategic SLG games also with three kingdom setting on the market (ie Immortal Conquest (²v¤g¤§滨) and Tactical Three Kingdoms (¤T°ê§Ó ¾Ô²¤ª©) etc). These games tend to have very impressive gross billings; hence we are highly anticipated by the gross billing performance of Under the Firmament (ÂE¹Ï¤§¤U). The game is set to be issued on the 21st of Oct and according to the management of the company, the game has very impressive operation indicators during the testing period.

Noah's Heart (¿Õ¨È¤§¤ß)

Noah's Heart (¿Õ¨È¤§¤ß) is a mobile MMORPG powered by Unreal Engine 4 and it was unveiled at the Tencent Games Annual Conference. With the support of Unreal Engine 4 technology, this game is the first MMORPG game that has realized the "spherical continuous big map (²y§Î³sÄò¤j¦a¹Ï)", which is more realistic than the common flat maps in previous MMORPG games. In addition, the game has a real-time dynamic weather system, and the game experience is very real. The current score of "Noah's Heart" on the TapTap platform is 8.3, and the number of reservations is close to 120,000. Based on the company's past performance in MMORPG games, we are highly anticipated to the launch of this game. Considering that the game is the first ¡§open world¡¨ MMORPG and the unique features of the game comparing to the company's previous MMORPG games, we expect the gross billing can reach or exceed the high level of Dragon Raja (Às±Ú¤Û·Q).

The company's leading R&D team is among the first to successfully introduce UE4 into mobile game development in China

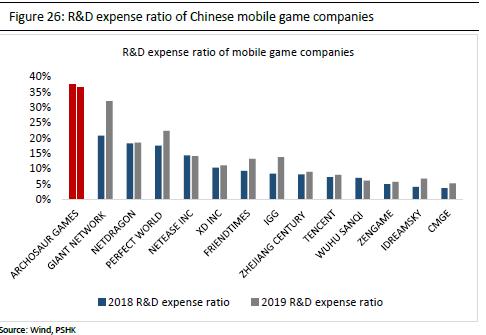

The company has a top R&D team in the industry, with a total of 871 R&D personnel, accounting for 87.3% of the company's total employees. Among the 871 R&D personnel, 236 R&D personnel have more than ten years of game development experience. The company understands that the R&D team is particularly important to the success of game development, so it binds outstanding R&D talents by giving competitive remuneration and equity incentives, and constantly improves remuneration and incentive policies through market research and comparison with competitors. In addition, the company is one of the first developers to successfully introduce Unreal Engine 4 into China's mobile game development industry and conduct secondary development. The company has started to shift their focus on R&D in Unity 3D engine to Unreal Engine 4 in 2018 and had starting to record impressive outcomes as a result of the shift in engine. The game Dragon Raja (Às±Ú¤Û·Q) in 2019 is China's first true 3D MMORPG mobile game powered by the Unreal Engine 4. The company's strong UE4 development capabilities was recognized by Epic games, the original developer of UE4, and the company was invited by Epic games to introduce the unique features of Dragon Raja (Às±Ú¤Û·Q) and the other 3 upcoming UE4 games at the 2019 Game Developers Conference and the China Joy in Aug 2020. The company spends significant resources of R&D and its R&D expenses ratio is among the top comparing to its peer. The R&D expense ratio in 2018/2019 is as high as 37.7%/36.5%. The company's strong mobile game R&D capabilities and high R&D investments have created a strong economic moat for the company and enables the company to survive and grow in the gradually refined Chinese mobile game sector.

The oversea markets will be a growth driver for the company

According to the company's past game publishing record, the company generally self-published games in overseas markets (sometimes partner up with a third party publisher), while mainly license the domestic game publishing to a well-known third party publisher (such as Tecnent, Zilong Game etc). This is because as compared with China's distribution channels, the overseas game distribution channels are relatively less complicated and more concentrated, with Google Play and IOS App Store occupying most of the market shares of mobile app distribution. On the contrast, the mobile app distribution business in China is relatively more complicated (especially for Android system), with different mobile brands` official app stores and third-party app stores. Therefore, the company has decided to conduct self-publishing in overseas markets, where the process of mobile game publishing is relatively simpler, while it choose to license the game publishing to an experienced third party game publisher in China, where the process of game publishing is more complicated.

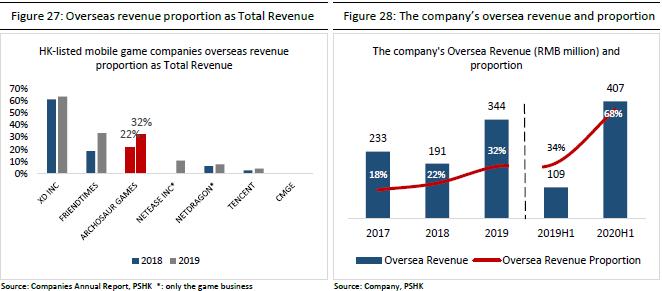

The company's overseas business has developed rapidly in recent years. Its overseas business revenue has risen from RMB 230 million in 2017 to RMB 340 million in 2019. The proportion of overseas business revenue has also increased from 18% in 2017 to 32% in 2019. The company's revenue contribution from oversea markets ranks in the top half among all HK-listed mobile game companies. The company's 1H20 oversea revenue was even as high as RMB 410 million, up by 273% yoy and accounted for 67.5% of the company's total revenue. This huge increase was mainly attributed by the brilliant performance of the self-published game Dragon Raja (Às±Ú¤Û·Q) in US, Europe as well as South East Asia regions. From the eye-catching performance, we can see that the overseas game business has become an indispensable part of the company. With the launch of Dragon Raja (Às±Ú¤Û·Q) in other emerging overseas markets (ie Vietnam) in 2H20 and the oversea publishing of new games such as Noah's Heart (¿Õ¨È¤§¤ß) and Under the Firmament (ÂE¹Ï¤§¤U) in 2H20/1H21, we strongly believe that the company's revenue from oversea markets will maintain a high growth and become a major growth driver.

The company's self-developed games are favored by Tencent, which provides certain guarantees for the company's domestic game business revenue

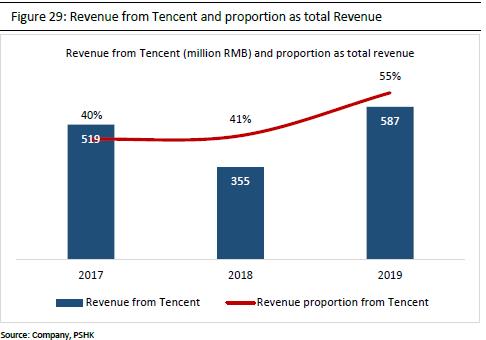

In terms of domestic game publishing, the company has always maintained a good cooperative relationship with Tencent. The company has also partnered up with Tencent and published 4 games in China, including Fantasy Zhuxian (¹Ú¤Û¸Ý¥P), Loong Craft (¤»Àsª§ÅQ), World of Kings (¸U¤ý¤§¤ý3D) and Dragon Raja (Às±Ú¤Û·Q). The revenue share from Tencent has already become an important portion of the company's total revenue, and this proportion also had an upward trend from 2017-2019. Tencent will also be responsible for domestic publishing of multiple upcoming games for the company, as mentioned above. Beside the game publishing business, Tencent also provides cloud services to the company. In addition to the in-depth business binding between the two parties, Tencent is also one of the company's major shareholders with a shareholding ratio of 13.34%. We believe Tencent and Archosaur Games will maintain their strong business partnership in the future, which will provide certain guarantees for the company's domestic game business revenue.

Financial Analysis and Forecast

Revenue

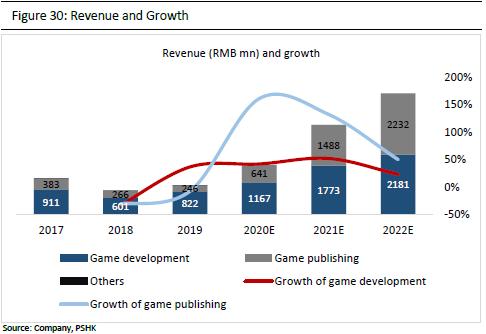

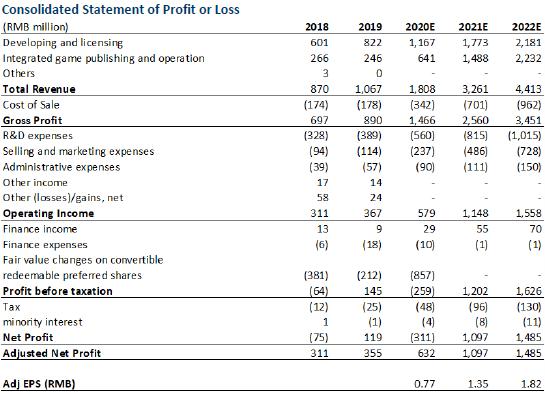

The company's revenue is mainly composed of two parts, developing and licensing (hereinafter referred as game development) as well as integrated game publishing and operation (hereinafter referred as game publishing). The company's total revenue for 2017/2018/2019 were RMB 1.31/0.87/1.07 billion. The company saw a yoy decrease of total revenue in 2018 was mainly attributable to the suspension of games pre-approval by Government in 2018 and the shift in focus of engine R&D in 2018. The suspension of games pre-approval delayed the launch of the company's new games. With the games pre-approval back on track in 2019, the company saw a yoy increase of 22.7% in revenue. The company's revenue from game development for 2017/2018/2019 were RMB 911/601/822 million, accounting for 70%/69%/77% if total revenue, respectively. On the other hand, the company's revenue of game publishing were RMB 383/266/246 million accounting for 29%/31%/23% of the total revenue.

Looking forward, considering 1) the company will launch 8 new self-developed games before the end of 2022; 2) the company will continue to focus on developing its overseas games` self-publishing business (the share of gross billing for self-publishing games are higher, but with a higher cost as well); 3) old games (such as "Dragon Fantasy", etc.) will continue to contribute stable income, we believe that the company's revenue will enter a high growth period. We believe the launch of new games, especially in new game genres, and the continuous development in oversea markets will further increase the company's MAU/MPU. We expect the company's game development revenue for 2020/2021/2022 to be RMB 1.17/1.77/2.18 billion, up by 42%/52%/23% yoy. On the other hand, the company's game publishing revenue for 2020/2021/2022 was 0.64/1.47/2.20 billion, up by 161%/132%/50% yoy.

Cost and expenses

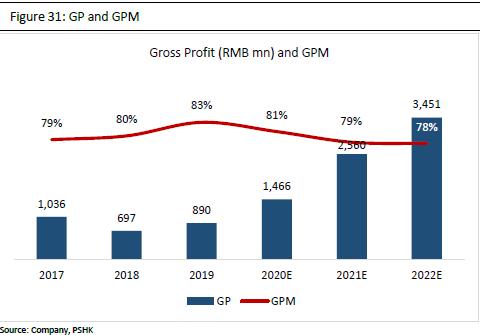

The company's gross profit margin has maintained a relatively stable level in the past and has an upward trend, rising from 79.1% in 2017 to 83.4% in 2019. The upward trend is mainly due to the decline in the proportion of the company's payment to IP parties, distribution channel and payment channels to total revenue. Compared with peers, the company's past gross profit margin is actually at a relatively high level. This is because the company's revenue for game development has accounted for majority of the total revenue. In terms of the company's game development business, revenue are recorded at a net basis of the total gross billing of the games, commission charged by payment channel and distribution channel are not recorded in the company's book, hence lower host and higher margin. With the expected increase self-publishing in overseas area (ie Dragon Raja (Às±Ú¤Û·Q) and some other news games), the company's revenue proportion from game publishing will increase. For game publishing businesses, the revenue is recorded as the gross basis of total gross billing of games and commission charged by distribution and payment channels etc are recorded as cost of sales, hence we expect the GPM of the company as a whole will slowly decline in the future as the revenue proportion from game publishing increases. We forecast the GPM in 2020/2021/2022 will be 81%/79%/78%.

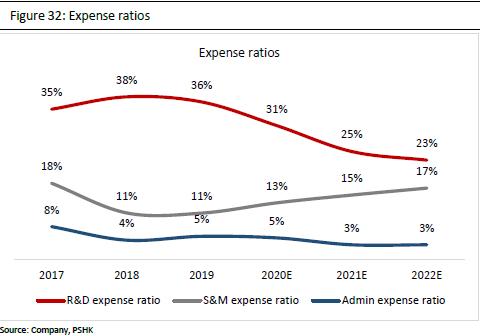

In terms of R&D expenses, the company has maintained a very high R&D expense ratio, which is about 34%-38%. We believe that the company's strong game R&D capabilities absolutely constitute a strong moat for the company, and the company will continue to invest huge resources in its R&D system in the future. We expect that the CAGR of R&D expenditure in 2019-2022 will be as high as 37.6%. Nonetheless, we think that the R&D expense ratio will drop in the future, despite the huge increase in R&D expenses, as we believe that the R&D expenses will grow slower than the huge revenue growth of the company in the future as described above. We forecast the company's R&D expense ratio for 2020/2021/2022 will be 31%/25%/23%, respectively.

On the other hand, the company's sales and marketing expenses in 2018 and 2019 also remained stable, at approximately 11%. However, with the rapid growth of the company's overseas self-publishing business, we expect advertisement and marketing expenses will increase in the future at a rate higher than the rate of increase of revenue. Compared to before, when the company focuses hugely on

game development and third party publishing, the company's advertising and marketing expenses were very low, since majority of these fees were paid by the third party publisher. We expect that the company's 2020/2021/2022 sales and marketing expense ratio to be 13%/15%/17% respectively.

Lastly, we forecast the administrative expense ratio of the company in 2020/2021 /2022 to be 5%/3%/3%. The relatively high ratio in 2020 was mainly attributed to the one off expenses, ie the listing fees. This ratio will be normalized to 3% in 2021 and 2022.

Valuation

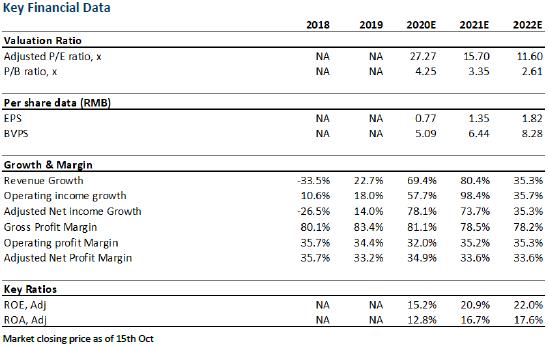

The company has a leading advantage in MMORPG games genres and has constituted a strong economic moat. The company has already laid a solid foundation in MMORPG games genres and is starting to expand businesses to SLG game genres (MMORPG and SLG are the two games genres with the highest growth potential). In addition to that, the self-publishing of games in oversea markets will further boost the company's performance in the near future and so we are high anticipated the company's results in 2021 and 2022. We forecast the adjusted EPS of the company in 2020/2021/2022 to be RMB 0.77/1.35/1.82.

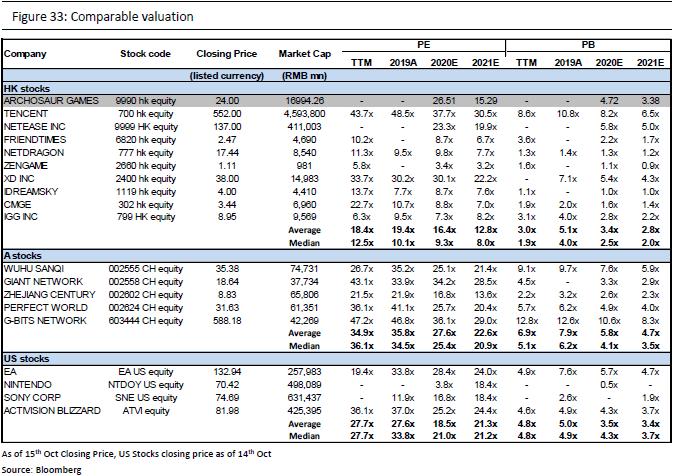

As of the closing price of 14th, the average 2021 PE of HK-listed mobile companies is 12.8x, but after considered that 1) the economic moat constituted by the company's strong R&D capabilities 2) the performance and gross billings of the company's past self-developed games 3) the new self-developed games are domestically published by Tencent, where a certain degree of stability on gross billings of these games can be guaranteed. Hence, in terms of valuation, we will give the company a certain amount of premium compared to the average of peers. The target price of Archosaur Games is HKD 33.6, corresponds to 2020/2021 adjusted PE of 38.1x/22.0x PE. We are initiating with a ¡§Buy¡¨ rating. (Market closing price as of 15th Oct) (exchange rate: RMB 0.88/HKD)

Risk

1) The tightening on Game regulations 2) The Games underperform comparing to expectation 3) Games launching are delayed due to unexpected reasons

Financial Statements

Click Here for PDF format...