Investment Summary

A diversified gaming company

The company develops and operates quality games in China and overseas. According to Frost & Sullivan, among PRC game operators who earned a majority of game operating revenue overseas in 2018, the company ranked fifth in terms of revenue from mobile games in 2018. The company has a diverse portfolio of games across different genres. As of December 31, 2019, its game portfolio consisted of 38 online games and 11 premium games. The company also operates TapTap, a leading game community and platform in China. According to the Frost & Sullivan, TapTap was the largest game community and platform in China in terms of average MAUs in 2018.

The company's abundant game reserve

The company has an abundant game reserve and is expected to launch multiple online games in 2020, including 3 self-developed games, Fantasy World (³Ð·Q¥@¬É), Torchlight: Infinity (¤õ¬²¤§¥ú¡GµL) and Project A (tentative name). Project A, the largest game project invested by the company since Ragnarok M, has been prepared for more than a year and is a Japanese girl-style MMORPG. Its liquidity is expected to reach Ragnarok M's relative high level. In terms of premium games, the company will launch multiple premium games in 2020 including Human: Fall flat (¤HÃþ¡G¤@±Ñ¶î¦a) , which is a game with a huge fan base around the globe and has already achieved incredible results in the Client game sector. The company's abundant game serve has laid a solid foundation for the company's future growth.

The unique strategy of ¡§Game + Platform¡¨, is becoming the economic moat for the company

Most game developers out there in the market do not have their own game community platform, so their business models are relatively traditional and fragile. Many game companies are worried about the imbalance in revenue and expenditure, therefore reducing their R&D expenses and promotion expenses for a greater safety margin. However, smaller capital investment on games also means that the games are less competitive, resulting in worse game performance. This business model will bring the company into a vicious circle. In contrast, Xd Inc has its own game community platform, therefore there is an additional revenue sources for the self-developed games. In addition to the traditional income generated from the self-developed games, the self-developed games as being the company's unique products, will also attract players to become TapTap platform's users. Thereby adding commercial value to the platform in long term and this value will be able to monetize in the long run. When the company considers the additional returns / commercial value brought by the platform, the company will be more willing to spend R&D expenses to improve product competitiveness. In addition, the company is also more willing to develop game types that are not dare to get involved under the traditional business model (such as game types with low initial returns but large market potential). Such products often have higher user anticipation and less market competition. In conclusion, we believe that this unique strategy of ¡§Game + Platform¡¨ has a huge advantage and will become an economic moat for the company. It also guarantees to the company's future earnings growth.

Valuation

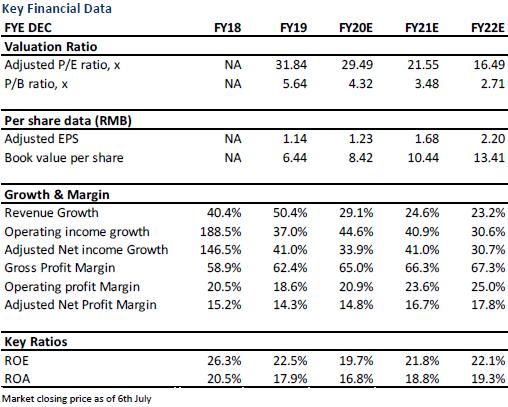

We believe that the company's economic moat created by its ¡§game + platform¡¨ strategy can bring a significant huge growth to the company's future performance with a certain amount of stability. It's growth potential is likely to be matched with the level of the Chinese top tier game companies. We forecast that the company's 2020/2021/2022 EPS are RMB 1.23/1.68/2.20 respectively. The target price is HKD 41.2, which implies a 2020/2021/2022 P/E ratio of 30.1x / 22.0x / 16.8x. We initiate with a ¡§Neutral¡¨ Rating.

Industry Review and Forecast

The mobile game market has the highest growth potential in Chinese game market

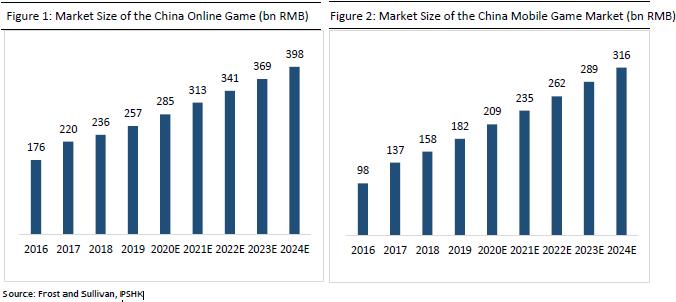

Since 2015, China has been the world's largest market of online games in terms of gross billings. One of the main reasons for the boom of China's online game market was the intensified demand for entertainment. According to Frost and Sullivan, China's online game market reached a size of RMB257 billion in 2019, and is expected to reach RMB398 billion in 2024, representing a CAGR of 9.1%. With the advancement of hardware and internet technology, the graphics, content and response speed of online games are being constantly upgraded, the development of online games are more tailored to player preference. Mobile game sector is the main sub-segment in the game sector with its growth higher than other sub-segments (client game sub-segment and web game sub-segment). China's mobile game market expanded from RMB98 billion in 2016 to RMB181.7 billion in 2019, and is expected to reach RMB316 billion in 2024, representing a CAGR of 11.7%. We believe that with the ongoing development of gaming online broadcast and the e-sport industry, as well as the increase proportion of mobiles in population, the mobile game sub-segment is likely to slowly replace the other sub-segments.

The size of the game market in the rest of the world

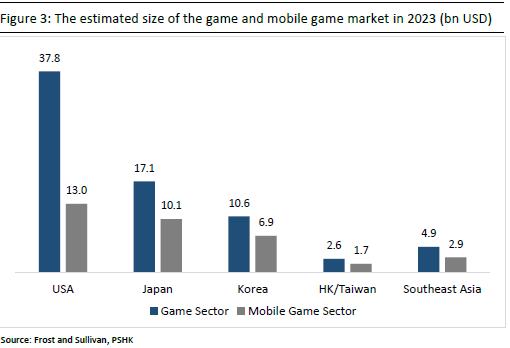

The United States had the second largest game market by revenue in the world in 2018. According to Frost & Sullivan, the size of the U.S. game market has reached USD 28.7 billion in 2018, and the size of the mobile game segment is about USD 9 billion. It is estimated that in 2023, the size of the online game market and the mobile game market will reach USD 37.8 billion and USD 13 billion respectively, with a CAGR of 5.7% and 7.5% in 2018-2023. In addition to the United States, the Asian mobile game market is also expected to continue to grow in the future. According to Frost & Sullivan, the 2018-2023 CAGR of the mobile game market size of Japan/Korea/Hong Kong and Taiwan/Southeast Asia are 6.5%/ 7.4%/ 10.6%/ 11.5% respectively.

The market for PRC Mobile Games Overseas

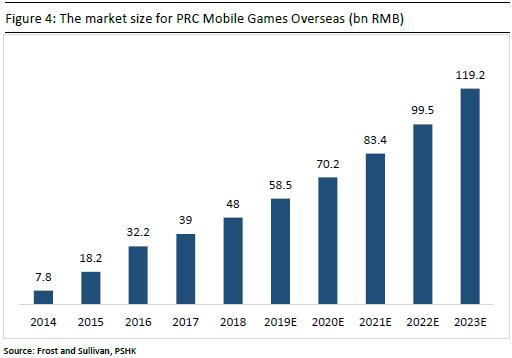

In recent years, many mobile game companies have been focusing on their overseas market business, mainly because the mobile game markets in many overseas regions (especially Southeast Asia) are still in the early stage of development and has great growth potential. Secondly, although the Chinese government has recently significantly relaxed the supervision of the Chinese mobile game market. Nonetheless, there are still a certain amount of policy risk in the Chinese mobile game market. As a result, expanding overseas markets will help Chinese mobile game industry participants to reduce this policy risk. According to Frost & Sullivan, the scale of China's overseas mobile game market recorded a significant growth at a CAGR of 57.5% from 2014 to 2018, and is expected to grow at a CAGR of 20.0% from 2018 to 2023.

The impact of the epidemic on the mobile gaming industry

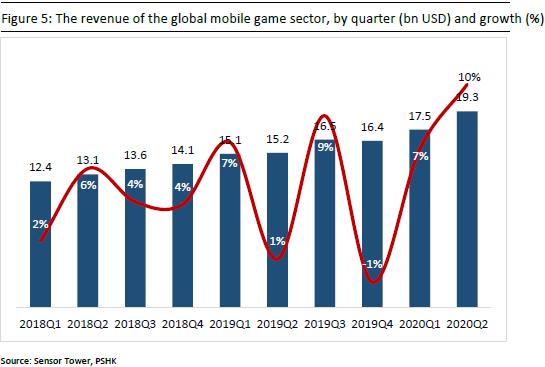

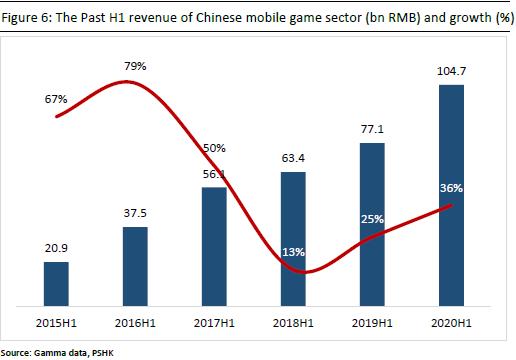

During the epidemic, mobile games not only provide a form of entertainment, but also serve as a channel for social communication, allowing people to socialize remotely when they are isolated at home. According to the Sensor Tower store intelligence data, the global mobile game revenue in 2020Q2 is as high as USD 19.3 billion, an increase of 27% yoy/10% qoq. In addition, the number of downloads of mobile games reached a new high during the epidemic. The global mobile game downloads in 2020 Q2 was 15 billion times, representing a yoy/qoq growth of 45%/13%. As for China's mobile game industry, according to gamma data, China's total mobile game revenue in the first half of 2020 was 104.7 billion yuan, an increase of 36% yoy, and the growth rate was higher than the global average.

�Company Overview and its Competitive Advantages

A diversified gaming company

The company develops and operates quality games in China and overseas. According to Frost & Sullivan, among PRC game operators who earned a majority of game operating revenue overseas in 2018, the company ranked fifth in terms of revenue from mobile games in 2018. The company has a diverse portfolio of games across different genres. As of December 31, 2019, its game portfolio consisted of 38 online games and 11 premium games. The company focuses on the development, distribution and operation of online games. The company's online games include mobile games and web games. Since 2012, the company has shifted its business focus to mobile games. In 2019, 96.6% of online game operating revenue came from mobile games.

The company also operates TapTap (also known as the Chinese Steam), a leading game community platform in China. According to the Frost & Sullivan, TapTap was the largest game community and platform in China by average MAUs in 2018. In 2016, 2017, 2018 and 2019, TapTap mobile app had average MAUs of 0.9 million, 10.2 million, 15.0 million and 17.9 million, respectively. TapTap provides gamers with a vast and diverse library of mobile game resources, such as game information, game recommendation and downloadable games. For the year ended December 31, 2019, games on TapTap had been downloaded 352.0 million times, increased by 36.8% on a year-on-year basis. Gamers post reviews and ratings of games on TapTap, and share their game experience in TapTap's forum. The numbers of game reviews and forum posts increased from 7.3 million and 3.0 million, respectively at the end of 2018 to 11.6 million and 6.5 million, respectively, at the end of 2019. On the other hand, TapTap serves as an open and convenient distribution platform for game developers. The number of registered developers increased by 3,344 and reached 11,006 at the end of 2019.

Strong game development and operation capabilities

As of December 31, 2019, the company is operating 38 online games. The income of online games mainly relies on users spending in games to purchase virtual items in the game, while online games are free to download. On the contrary, the income of premium games comes from the fees paid by customers for downloading games. The company is operating a variety of popular games including RPG genre Ragnarok M and Shen Xian Dao (HD)( ¯«¥P¹D°ª²M«»sª©), CCG genre Girls` Frontline (¤Ö¤k«e½u), SLG genre Heng Sao Qian Jun (¾î±½¤dx), battle arena game genre Sausage Man (»¸z¬£¹ï) and placement game genre Ulala (¤£¥ðªº¯Q©Ô©Ô). Most of the company's popular online games have been launched in the past two- three years and are in the growth or maturity phase of their life cycle. Hence, the future revenue contribution from these games are expected to be relatively stable and rising.

Ragnarok M is an MMORPG game based on the Norse Mythology creating a fantasy world of swords and magic. The game was jointly developed by Gravity, Dream Network and the company. The game is currently distributed in more than 50 countries and regions around the world, and has achieved brilliant results. As of December 31, 2019, it has totally 33 million registered users and over 5 million monthly active users (MAUs), becoming one of the most popular mobile MMO games across the world. The company, currently the sole publisher and operator of Ragnarok M in China, recognize the whole gross billing as revenue, and only pay 13.667% of the gross billings to Dream Network. In terms of other region, the company is acting as technical/ operational support and collect 22.5%-45% of respective regions` gross billing as service fees. The company plans to release an important updated version of Ragnarok M in the second half of 2020, in which it will significantly improve picture quality and add new game contents. We believe the updated version of the game can extend its life cycle and increase the MPUs and ARPPUs of the game. The revenue of Ragnarok M in 2017, 2018 and 2019 as of the end of May were RMB 468 million, RMB 627 million and RMB 504 million, respectively, contributing 35%, 33% and 49% of the company's total revenue.

Sausage Man (»¸z¬£¹ï) is a battle arena game. All the characters in this game have sausage shapes. Gamers can opt to land on multiple terrains in the game and are required to seek and use gear to defeat other gamers and obtain their gear. Since the launch of Sausage Man in China in April 2018, it quickly became popular among PRC gamers and topped the free game chart of App Store in China for five consecutive days in October 2018. Sausage Man had average MAUs of approximately 4.3 million in 2018 and average MAUs of approximately 11.1 million for the nine months ended September 30, 2019. The company started to monetize Sausage Man in Feb 2019. It is expected the game will enter its gross billing's harvest period in 2020/ 2021 and contribute significant of revenue for the company. Sausage Man has been launched on the market for almost three years, during which both operating data and income maintain growth. It also serves as the best case study for the synergetic growing between our games and TapTap. The company will integrate player accounts, friendship and in-game community of both Sausage Man and TapTap this year to enhance their user experience.

On the other hand, the company operates 11 premium games as of December 2019, including ICEY, Muse Dash, To the Moon, Heimdallr and The Swords. However, the company's premium games only contributed roughly 2% of the companys` total revenue. As of December 31, 2019, the company had sold over 3.0 million copies of ICEY and over 1.4 million copies of Muse Dash across all platforms globally.

The company's abundant game reserve

The company has an abundant game reserve and is expected to launch multiple online games in 2020, including 3 self-developed games, Fantasy World (³Ð·Q¥@¬É), Torchlight: Infinity (¤õ¬²¤§¥ú¡GµL) and Project A (tentative name). Project A, the largest game project invested by the company since Ragnarok M, has been prepared for more than a year and is a Japanese girl-style MMORPG. Its liquidity is expected to reach Ragnarok M's relative high level. In terms of premium games, the company will launch multiple premium games in 2020 including Human: Fall flat (¤HÃþ¡G¤@±Ñ¶î¦a) , which is a game with a huge fan base around the globe and has already achieved incredible results in the Client game sector. Human: Fall flat has already been launched in overseas region but has not yet been launched in China. The company is currently revising and upgrading the game according to the feedbacks from overseas players. We believe the game can drive the company's revenue from premium games after the game is launched in China. The company's abundant game serve has laid a solid foundation for the company's future growth.

The market leading Game platform ¡V TapTap

Ever since the launch of TapTap platform, it has established a free-to-distribute business model. Therefore, the revenue of TapTap platform comes mainly from its advertisement but not the share of gross billings from games downloaded through the platform. Thereby greatly enhanced the credibility of the games recommended by the platform in the eyes of users. Because of this, the company has the largest user base in the industry, which is beneficial to the platform's advertisement income. The company is only charging a 5% distribution fee from the premium games downloaded through the platform (the 5% distribution charged is very low comparing to its competitors) and this income is mainly used to cover the fee charged by the payment channel. The company's low distribution fee charged has increased the profits for the game developer and hence increase their R&D willingness, thereby bringing games with better quality to the platform. This is likely to help increasing the number of users of the platform and improving the platform's advertisement business. In addition, For the games recommended on the homepage of TapTap, the company will introduce a deep learning-based recommendation algorithm, through which, games on the homepage will be recommended and ranked in view of habits and preference of different users and based on editor's recommendations and community ratings. This is likely to further increase the users` experiences and number of users of the platform.

The unique strategy of ¡§Game + Platform¡¨, is becoming the economic moat for the company

Most game developers out there in the market do not have their own game community platform, so their business models are relatively traditional and fragile. Many game companies are worried about the imbalance in revenue and expenditure, therefore reducing their R&D expenses and promotion expenses for a greater safety margin. However, smaller capital investment on games also means that the games are less competitive, resulting in worse game performance. This business model will bring the company into a vicious circle. In contrast, Xd Inc has its own game community platform, therefore there is an additional revenue sources for the self-developed games. In addition to the traditional income generated from the self-developed games, the self-developed games as being the company's unique products, will also attract players to become TapTap platform's users. Thereby adding commercial value to the platform in long term and this value will be able to monetize in the long run. When the company considers the additional returns / commercial value brought by the platform, the company will be more willing to spend R&D expenses to improve product competitiveness. In addition, the company is also more willing to develop game types that are not dare to get involved under the traditional business model (such as game types with low initial returns but large market potential). Such products often have higher user anticipation and less market competition.

On the other hand, with the accumulation of TapTap platform users, the company's user database (such as user preferences) has also expanded. The company can analyze these user data through big data analysis, and combine the analyzed data with the company's R&D system in order to develop high-quality and popular games that meet player preferences. This will greatly improve the company's revenue and its revenue stability. Lastly, The TapTap users will also increase as more high-quality self-developed games are brought to the platform, which is beneficial to the platform's advertisement business. In conclusion, we believe that this unique strategy of ¡§Game + Platform¡¨ has a huge advantage and will become an economic moat for the company. It also guarantees to the company's future earnings growth.

The company is likely to become a major business partner of ByteDance and grow rapidly from it

Since 2018, ByteDance has entered the online game industry. Although ByteDance has abundant resources, nonetheless, it has entered the online game industry later than the other game giants (such as Tencent and Netease). As a result, the relatively bigger and more popular IPs has been already locked by these game giants. We believe that if ByteDance intends to continue its adventure in the online game sector, it will inevitably have to confront with these game giants in the future. Hence, the chance of ByteDance to cooperate with these game giants is very low. Rather, ByteDance would have to search for cooperation opportunities with the second tier game companies and would have to provide a very attractive offer to attract these companies. We believe that ByteDance, as being one of the shareholders of XD Inc, will actively seek for strategic cooperation with XD Inc in the future. Xd Inc is also likely to grow rapidly by relying on ByteDance's huge traffic resources.

Financial Analysis and Forecast

Game Revenue

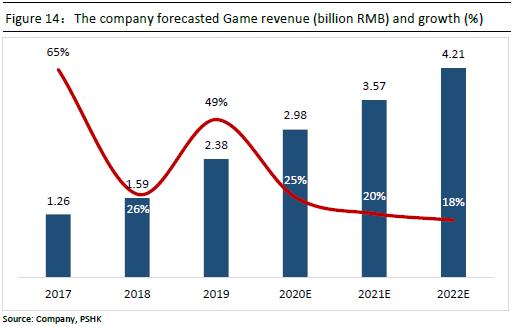

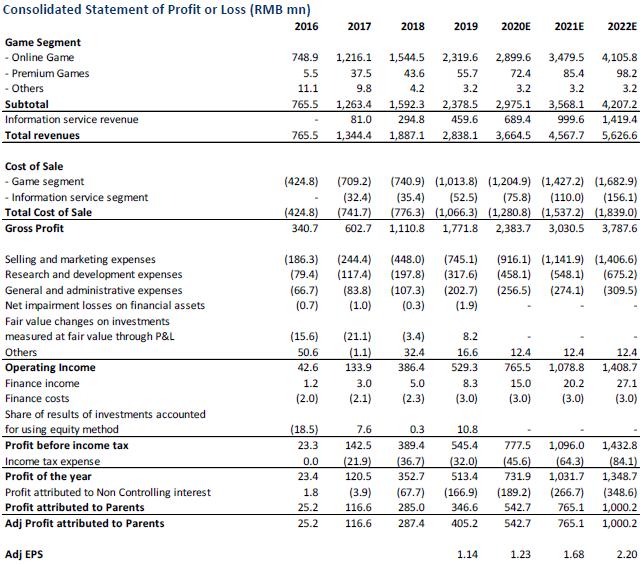

The company's game revenue is mainly divided into three parts, online games, premium games and other game revenues. Among them, the company's online game revenue increased from RMB 1.216 billion in 2017 to RMB 2.320 billion, with a CAGR of 38%. This huge increase was mainly attributed to the rapid increase in MPUs during the period. The MPUs was up from 240 thousand in 2017 to 720 thousand in 2019. The reason for such rapid increase was mainly because the outstanding performance of multiple games including the Ragnarok M during the period. Ragnarok M has contributed 35% and 33% of revenue in 2018 and 2018. Looking forward, since most of the company's popular games are still in the growth stage of their life cycle, and the company's project reserves are abundant, several popular games such as "Project A" and other long-prepared games will be launched before the end of the year. In addition, Ragnarok M will also continue to be distributed in different overseas regions, so we believe that the company's future MPUs will have room for growth in the upcoming years. We forecast the MPUs in 2020/2021/2022 will be roughly 900/1080/1,275 thousands. Based on the above reasons, we predict that the company's online game revenue for 2020/2021/2022 will be RMB 2.90/3.48/4.11 billion, up 25%/20%/18% yoy. On the other hand, we expect that the revenue contributed by the premium games and others together in 2020/2021/2022 will still remain insignificant, and forecasted to be RMB 75.6/88.6/101.4 million respectively. In total, the forecasted total game revenue in 2020/2021/2022 are RMB 2.98/3.57/4.21 billion respectively.

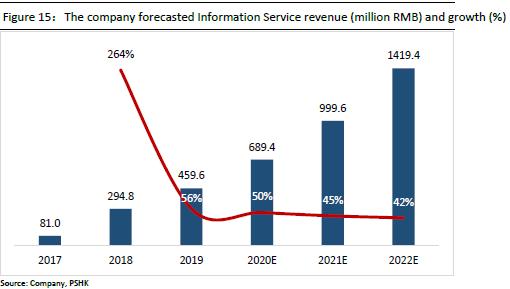

Information Services Revenue

Since the company began operating the TapTap platform in 2017, its information service revenue has increased dramatically, from RMB 81 million in 2017 to RMB 460 million in 2019, with a CAGR of 138% from 2017 to 2019. As of the end of 2019, the Monthly Active users (MAUs) of the TapTap platform was only 17.9 million. We believe that the (MAUs) of the TapTap platform can grow rapidly in the future by relying on the strategic model of "Game + Platform" mentioned above, thereby bringing more traffic and advertising revenue to the platform. The forecasted MAUs of the platform in 2020/2021/2022 are 20.6/22.8/27.0 million. Lastly, we believe that the pricing power of the company on its information services business will also increase as the number of MAUs of the platform increases. We predict that the company's information service revenue for 2020/2021/2022 will be RMB 689/1,000/1,419 million, a yoy increase of 50% /45% /42%.

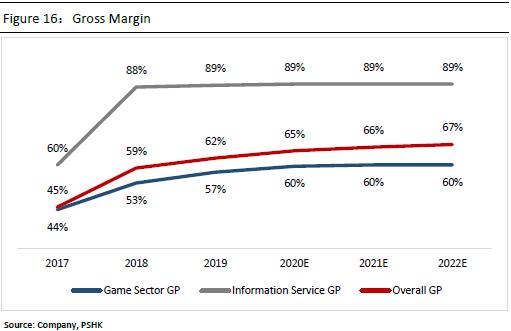

Gross Profit and Margin

The gross profit margin of the company's game business has increased steadily in recent years, from 44% in 2017 to 57% in 2019. The main reason is that with the increase in the proportion of overseas market revenue from games such as "Ragnarok M" and Langrisser in recent years, the company's revenue from games recognized on a net basis has also increased as a percentage of total game revenue, thereby driving the company's overall game GPM upward. With the overall trend of the industry's games going overseas, we expect the company's future game GPM will rise and be maintained at 60%. On the other hand, the gross profit margin of the company's information services has remained at a level of approximately 88%-89% in the past two years. We believe that the company can continue to maintain this GPM level in the future. We forecast the company's gross profit for 2020/2021/2022 will be RMB 2.34/3.03/3.78 billion, with a corresponding gross margin of 65%/66%/67%.

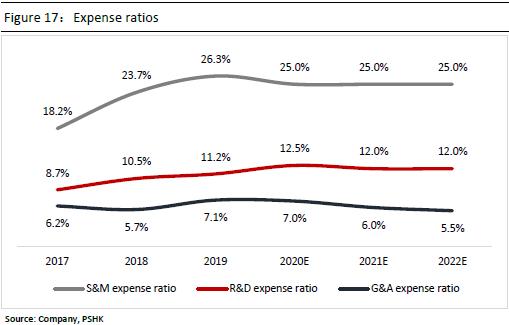

Expenses and Expense Ratio

The company's sales and marketing expense ratio (S&M ratio) has risen steadily in the past three years, from 18% in 2017 to 26% in 2019. We believe that the company will continue to spend a certain amount of marketing expenses on games and TapTap in the future. Therefore, we expect the company's future S&M expense ratio will remain at a relatively high level of 25%. In addition, the company's R&D expense ratio in the past three years was relatively stable, ranging from 9-11%. We believe that the company's future R&D expense ratio will increase and stay between about 12%-13%. The reason is that we expect the company will continue to improve its R&D capabilities in the future in order to improve game quality and user experience. Finally, we believe that the company's future general and administrative expense ratios (G&A ratio) will steadily decline along with the company's economies of scale.

�Valuation

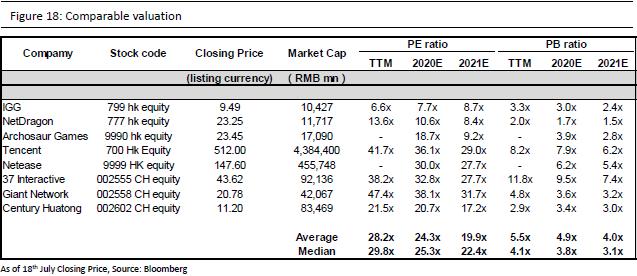

As of the closing price on 18th Aug, the 2021 P/E of the HK listed market leaders - Tencent / Netease are 29.0x/27.7x respectively and the 2021 P/E of the HK listed industry average (excluding the bottom tier company) is 19.9x. We believe that the company's economic moat created by its ¡§game + platform¡¨ strategy can bring a significant huge growth to the company's future performance with a certain amount of stability. It's growth potential is likely to be matched with the Chinses top tier game companies. Hence, from the valuation perspective, giving out a target P/E that is above the industry average (excluding the bottom tier company) and close to the P/E of the market leaders will be more reasonable. We are setting a 2021 target P/E of 22x to the company.

We forecast that the company's 2020/2021/2022 EPS are RMB 1.23/1.68/2.20 respectively. The target price is HKD 41.2, which implies a 2020/2021/2022 P/E ratio of 30.1x / 22.0x / 16.8x. We initiate with a ¡§Neutral¡¨ Rating

Risk

1) The tightening on Game regulations 2) The Games underperform comparing to expectation 3) The MAUs growth of TapTap platform is less than expectation

Financial Statements

Click Here for PDF format...