Investment Summary

Topsports is the largest sports retailer in China. Started to operate sports shoes and apparel retail in 1999. In the past 20 years, it has expanded its sales network and expanded its brand portfolio to meet Chinese consumers` demand for sports shoes and apparel products. The company currently operates more than 8,000 stores directly in nearly 300 cities across the country in order to establish the broadest and deeply penetrating national sports shoes and apparel retail network. According to Frost & Sullivan's data, Topsports` market share in 2018 was 15.9%, ranking first in China's domestic sports shoes and apparel retail market.

Channel integration, stores continue to upgrade

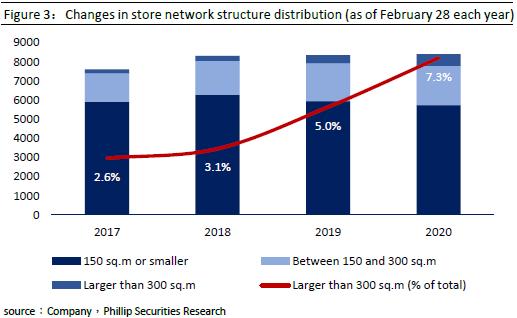

The company continues to focus on the optimization of its direct retail store network to consolidate its retail network advantages. During the period, low-yield and loss-making stores were closed in due course, and new stores were opened with relative caution. During the year, the company closed 1,364 stores during the year and opened 1,416 new stores. The overall number of stores increased by 52 compared with last year and gross sales area increased by 10.6%. Stores covering an area of more than 300 square meters, such as themed flagship stores and brand flagship stores, have increased from 200 in 2017 to 612 in 2020, a three-fold increase in four years to increase customers` offline shopping Experience.

The sportswear industry is steadily improving

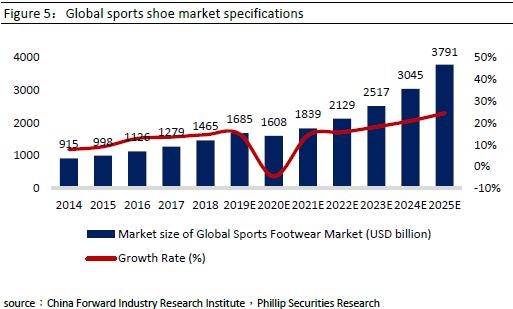

In the past ten years, the global sports shoe market has steadily expanded, and the concept of national sports has driven the growth of global sports consumption. According to a report by China Forward Industry Research Institute (¤¤°ê«eÁx²£·~¬ã¨s°|), the global sports shoe industry market size has risen from US$66.7 billion in 2010 to US$146.5 billion in 2018, growing at a CAGR of 10.3%, and it is estimated that the market is close to the level of 170 billion US dollars in 2019. The institute also predicts that the global sports shoe market will maintain a medium-speed and steady growth, and is expected to reach a scale of US$379.1 billion in 2025, with a compound annual growth rate of about 18.7%.

Close cooperation with global sports brands

The revenue of global sports brands in China mainly comes from wholesale channels. In the past two decades, global sports brands have established strategic and interdependent relationships with Chinese retail partners. Global sports brands mainly rely on mature sports retail companies to provide specific brand products and experiences to local consumers. According to Frost & Sullivan's data, in 2018, about 70% of global sports brands` retail revenue in China came from wholesale channels

Valuation and Investment Recommendation

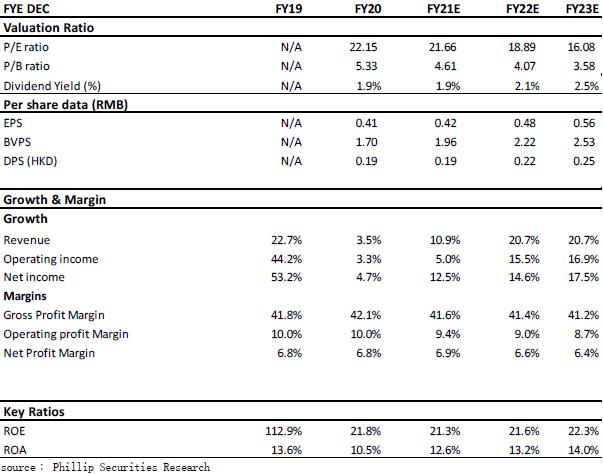

In the past, the company continued to maintain a good cooperative relationship with Nike and adidas. Facing the impact of e-commerce on the retail industry, the company improved its stores to provide customers with unique consumer experiences that e-commerce cannot provide, such as holding theme events, etc. The impact of the COVID-19 on the company's revenue has been mainly reflected in the FY20 annual report. We expect the company's earnings per share in 2021/2022 to be RMB 41.80/47.92 cent. The target price of $11.61 HKD corresponds to P/E of 25.00x /21.81x in FY21/FY22.

Risk

1) The impact of COVID-19 continues 2) Business relies on two major brands 3) The conflict between US and China.

Company Profile

Topsports is the largest sports retailer in China. Started to operate sports shoes and apparel retail in 1999. In the past 20 years, it has expanded its sales network and expanded its brand portfolio to meet Chinese consumers` demand for sports shoes and apparel products. The company currently operates more than 8,000 stores directly in nearly 300 cities across the country in order to establish the broadest and deeply penetrating national sports shoes and apparel retail network. According to Frost & Sullivan's data, Topsports` market share in 2018 was 15.9%, ranking first in China's domestic sports shoes and apparel retail market.

Company development process

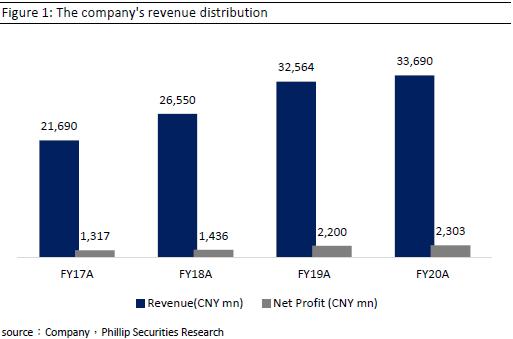

The company was acquired by Belle International in 2006. Belle International was listed on the main board of Hong Kong in 2007 and was privatized and delisted in 2017 because it could not withstand the impact of e-commerce. Topsports integrated and transformed after Belle's delisting, and then in 2019, Belle International spun off its sports distribution business, Topsports, and went public. Topsports` revenue and net profit grew at a compound annual growth rate of 16% and 20% from FY2017 to FY2020, respectively. The company's revenue and net profit in FY2020 were RMB 33.693 billion and RMB 2.303 billion, an increase of 3.45% and 4.71% year-on-year.

Cooperating with world-renowned brand

The company's income distribution is mainly divided into sales of goods income and joint operating fee income, of which sales of goods income is divided into main brands (Nike and Adidas) and other brands. The company currently owns the distribution rights of 11 international brands. In addition to the main brands Nike and Adidas, other brands include Puma, Converse, Timberland, Vans, The North Face, Asics, Onitsuka Tiger, Reebok, Skechers, etc. The main brands contributed 87.5% of the company's total revenue in FY20, while other brands accounted for 11.6%.

Channel integration, stores continue to upgrade

As of February 29, 2020, Topsports has 8,395 directly-operated stores, contributing 86.6% of the company's revenue. In addition, it has more than 1,000 downstream retailers, operating nearly 2,000 dealership stores, contributing 12.5% of the company's revenue.

The company's direct-operated stores can be divided into three forms: 1) Single-brand stores. In 2019, more than 99% of the company's direct-operated stores are single-brand stores, which are the main store composition. 2) Multi-brand collection stores, including Topsports and Foss. 3) Sports City.

The company continues to focus on the optimization of its direct retail store network to consolidate its retail network advantages. During the period, low-yield and loss-making stores were closed in due course, and new stores were opened with relative caution. During the year, the company closed 1,364 stores during the year and opened 1,416 new stores. The overall number of stores increased by 52 compared with last year and gross sales area increased by 10.6%. The number of stores of 150 square meters and below in the company has continued to decrease in the past four years, from 5,918 in 2017 to 5,732 in 2020, and the overall proportion has dropped from 77.8% to 68.3%. Stores covering an area of more than 300 square meters, such as themed flagship stores and brand flagship stores, have increased from 200 in 2017 to 612 in 2020, a three-fold increase in four years to increase customers` offline shopping Experience.

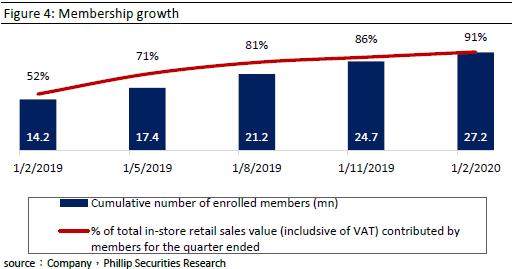

While optimizing channels, the company has also deepened its interaction with consumers through continuous development of membership plans and enriching membership benefits in the past year. As of February 29, 2020, the company's cumulative number of registered members reached 27.2 million, an increase of approximately 91.5% within a year. At the same time, in the quarter ended February 29, 2020, 91.0% of the company's total in-store retail sales came from members. The continued expansion of the membership program will help the company serve consumers in more dimensions and at the same time have a better understanding of each consumer's preferences.

Industry analysis

The sportswear industry is steadily improving

In the past ten years, the global sports shoe market has steadily expanded, and the concept of national sports has driven the growth of global sports consumption. According to a report by China Forward Industry Research Institute (¤¤°ê«eÁx²£·~¬ã¨s°|), the global sports shoe industry market size has risen from US$66.7 billion in 2010 to US$146.5 billion in 2018, growing at a CAGR of 10.3%, and it is estimated that the market is close to the level of 170 billion US dollars in 2019. Affected by the COVID-19, this year, the sports shoe market is expected to decline in 2020. With the continuous recovery of the world economy, emerging markets with huge consumption potential such as India and China will drive the global economy. The institute also predicts that the global sports shoe market will maintain a medium-speed and steady growth, and is expected to reach a scale of US$379.1 billion in 2025, with a compound annual growth rate of about 18.7%.

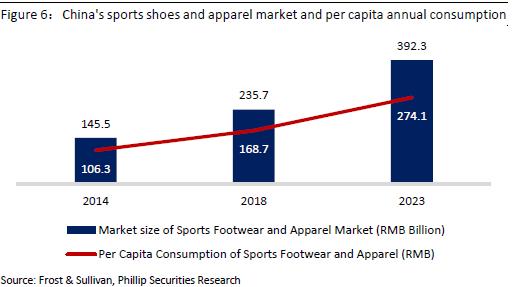

According to Frost & Sullivan's report, in terms of total retail sales (including value-added tax) in 2018, China has become the second largest sports footwear retail market after the United States. The total retail sales (including value-added tax) of China's sports shoes and apparel retail market increased from RMB 145.5 billion in 2014 to RMB 235.7 billion in 2018. At the same time, China's per capita annual consumption expenditure on sports shoes and apparel products also increased from RMB 106.3 in 2014 to RMB 168.7 in 2018, representing a compound annual growth rate of 12.2%. It is estimated that by 2023, total retail sales (including value-added tax) and per capita annual consumption expenditure will reach RMB 392.3 billion and 274.1 respectively. Nevertheless, China's consumption expenditure on sports shoes and clothing is lagging behind other major developed economies. According to Frost & Sullivan's data, in 2018, China's per capita annual consumption of sports shoes and clothing accounted for all types of shoes and clothing. The per capita annual consumption is only 12.5%, while the United Kingdom, the United States and Japan are 27.7%, 31.8% and 24.3% respectively. At this stage, there is still great potential for growth.

The revenue of global sports brands in China mainly comes from wholesale channels. In the past two decades, global sports brands have established strategic and interdependent relationships with Chinese retail partners. Global sports brands mainly rely on mature sports retail companies to provide specific brand products and experiences to local consumers, and their self-operated sales channels are mainly online retail and factory stores. At the same time, it also operates a small number of flagship stores in first- and second-tier cities to showcase the brand and increase customer awareness. According to Frost & Sullivan's data, in 2018, about 30% of global sports brands` retail revenue in China came from self-operated stores or online channels, and another 70% came from wholesale channels (including national and regional retail sales).

National retailers refer to retailers that have established a network of directly-operated stores throughout China. The company's prospectus stated that at the end of 2018, there were only three national retailers in China. Regional retailers refer to retailers that operate a regional network of stores in China. Compared with national retailers, their scale of operations is smaller and highly dispersed. Because national retailers have higher levels of operation, marketing, financial and technical resources, they tend to have closer cooperative relationships with brand partners than regional retailers. According to Frost & Sullivan data, in 2018, brand self-operated channels, national retailers and regional retailers accounted for approximately 33.4%, 28.7% and 37.9% of China's sports footwear and apparel retail market, respectively. However, 28.7% of the market share is occupied by only three national retailers. It can be seen that the retail market is currently dominated by national retailers.

The prevailing single-brand store model in China provides customers with a unique brand experience

In terms of the retail model, different from other major developed economies where multi-brand stores are the main retail model, single-brand stores are the more common business model in China. Compared with multi-brand stores, the competitive advantage of single-brand stores lies in their ability to show brand image and provide customers with a unique brand experience. Global sports footwear and apparel retail has also begun to transform to a single-brand store model. Leading sports brands have devoted more resources and attention to excellent retail partners who can enhance consumer experience and enhance brand influence.

Company competitive advantage

The company takes a firm lead in the domestic retail industry

The market for China's sports shoe and apparel retail industry is relatively fragmented, with only two national retailers accounting for a significant share. Among all the market participants in China, Topsports is firmly in the leading position. According to Frost & Sullivan, in terms of retail equivalent sales, Topsports ranked first among retailers in the Chinese sports shoe retail market in 2018, reaching RMB 37.5 billion, which is higher than the second place. More than 30%. Topsports and Pou Sheng, the top two sports shoes and apparel retailers in the market, together account for 27.5% of the market. The remaining market share is derived from many regional retailers, generally only about 1%. At the same time, Topsports` directly-operated stores are also more efficient. In 2018, the average retail sales of a single store of the company's directly-operated stores reached RMB 3.7 million, which was about 12% higher than the second-place peer. Due to higher operating efficiency, synergy of cross-regional operations and strategies, company will continue to maintain its competitive advantage.

The company has a close relationship with Nike and adidas

Topsports works closely with leading global sports brands, and has cooperated with Nike and adidas for nearly 20 and 15 years respectively. The company is currently Nike's second largest retail partner and adidas's largest retail partner. The company implemented the strategic store model for the first time in 2016, and the design of strategic stores usually meets the standards of brand partners` self-operated flagship stores to enhance customers` shopping experience. The performance of these store models has proven its commercial success. As of February 28, 2019, the company is the retail partner that operates the most Nike BEACON stores (one of Nike's premium store classifications) in mainland China. In addition, the company not only operates the first adidas Sportswear Collective ("SWC") store operated by a retail partner of adidas in China, but also has the largest number of adidas highest-level stores in China.

Single-brand stores enable the company to provide services to consumers seeking a specific brand shopping experience. At the same time, the company also opens theme stores with specific sports as the theme. In April 2019, the company was authorized by the NBA to open the largest NBA store outside North America (the ¡§NBA Beijing Flagship Store¡¨) in Beijing, covering an area of more than 1,000 square meters. In addition to the collection of NBA officially licensed products produced by more than ten different brands, the store also creates a shopping experience for NBA fans through in-store design and store activities, and opens up new business models.

Topsports not only provides retail services for the two major brands. With its years of marketing experience in China, the company also provides product design feedback to Nike and adidas to help them better cater to the Chinese market. Topsports is currently the only domestic retailer that contact with Nike's global headquarters regularly to share the company's observations on macro market trends. Through regular conversation with the management of brand partners in Greater China, the company can give advices brand partners on product design, product line and brand positioning strategies, and establish more cooperation models with partners. Nike and Adidas have successively listed China as their target market and put forward a strategy for developing China's deeply penetrating market. It is expected that Topsports will continue to benefit from the brand's development in the Chinese market.

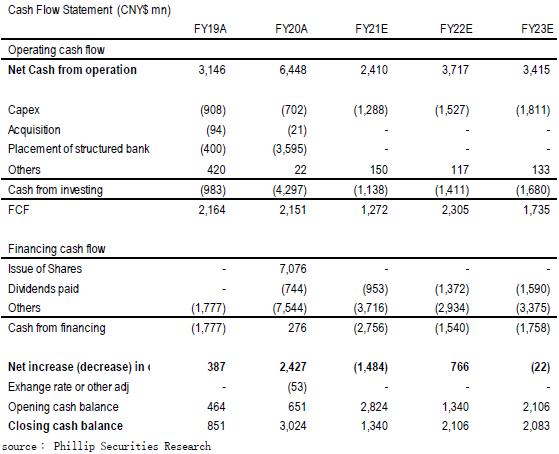

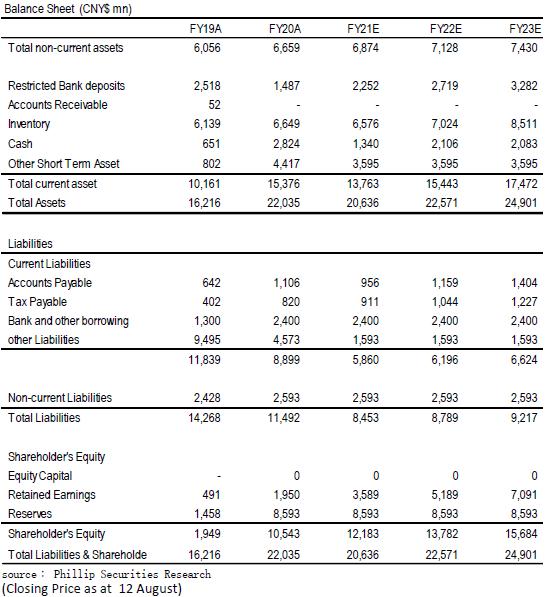

Financial Analysis

Revenue analysis

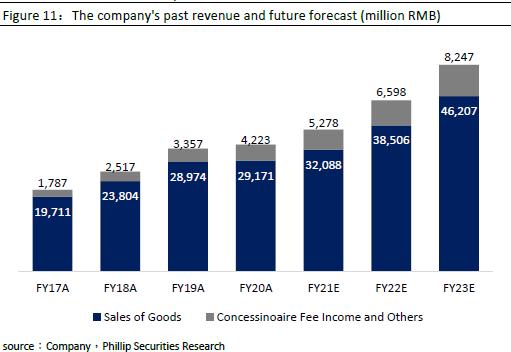

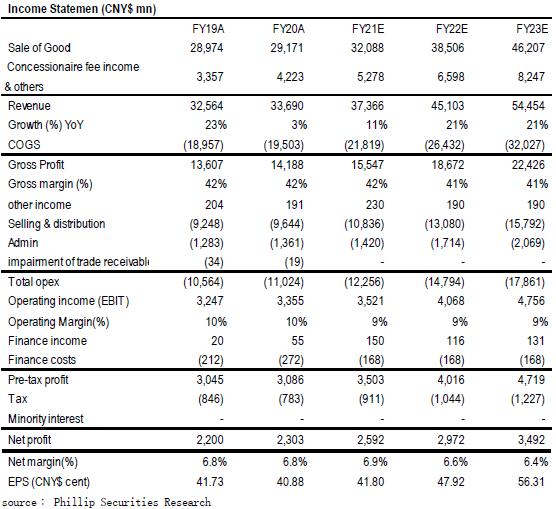

The company's revenue has increased year-on-year in the past four years, increasing at a compound annual growth rate of 15.8%, from RMB 21.69 billion in 2017 to RMB 33.69 billion in 2020. Since the beginning of 2020, the outbreak of new crown pneumonia in mainland China, many merchants closed in the first quarter of this year, which also affected the company's retail business. During the fiscal year 2016 to the fiscal year 2019, the average growth of the retail business was about 22%. The growth of the retail business for the year was flat in fiscal 2019.

Both Adidas and Nike said in the interim results of this year that since the second quarter, the company's retail sales data in the Greater China region has returned to the level of same period in last year. Together with the economic recovery in Mainland China, sales are expected to record positive growth in the second half of the year. Although the retail sales growth of China may not achieve high growth rate as previous years, it is expected to record positive growth. As for the company's wholesale business, the growth has slowed in the past three years, from 41% in 2018 to 26% in FY 2020. It is expected that FY21 total revenue will increase by approximately 10.9% and return to growth in FY22 track.

Profitability

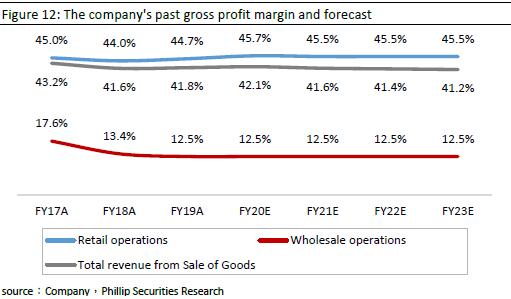

The company's gross profit margin in the past four years was relatively stable, with an average of about 42.2%. The gross profit margin of retail business fell on average at 44.6%. The gross profit margin of wholesale business was relatively volatile. The gross profit margin was 17.6%, which continued to drop to 12.5% in 2018 in the next two years. The future gross profit margin of this business is expected to be similar to the current level.

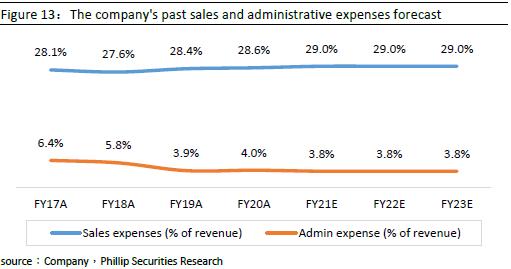

Expenses for the period

The company's sales expenses have been stable over the past three years, with an average of about 28.2%, which is similar to the industry level and is expected to remain at 29% in the future. The performance discount of administrative expenses over the past three years has improved, from 6.4% in 2017 to 4.0% in 2020, and it is expected that it will remain at a similar level in the future.

Company valuation

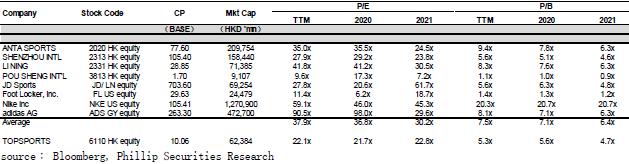

In the past, the company continued to maintain a good cooperative relationship with Nike and adidas. Facing the impact of e-commerce on the retail industry, the company improved its stores to provide customers with unique consumer experiences that e-commerce cannot provide, such as holding theme events, etc. The impact of the COVID-19 on the company's revenue has been mainly reflected in the FY20 annual report. In addition, Nike and adidas both stated that their revenue in the Greater China region had been flat in the second quarter and began to grow in May. The company's revenue is expected to be Respond quickly after the epidemic. Anta Sports, Li Ning, and Pou Sheng International, which also focus on functional apparel in Hong Kong stocks, have an average P/E of 31.03x.

Because the company's main business is brand retailers, the future revenue growth potential may not be as good as the company with its own sports brands. We expect the company's earnings per share in 2021/2022 to be RMB 41.80/47.92 cent. The target price of $11.61 HKD corresponds to P/E of 25.00x /21.81x in FY21/FY22.

(Closing Price as at 12 August)

Risk

1) The impact of COVID-19 continues

2) Business relies on two major brands

3) The conflict between US and China

Peer Comparison

Financials

�

Click Here for PDF format...