Investment Summary

Last Year's Results Declined with the Market

Tuopu Group reported a revenue of RMB5,359 million in 2019, down by 10.45% yoy due to the sliding sales volume of major customers such as Geely, SAIC-GM and Ford resulting from overall downturn of the automobile industry last year. The net profit attributable to the parent company of RMB456 million, down by 39.44% yoy. Basic EPS was RMB0.44, and the DPS was RMB0.19, a dividend payout ratio of 43%.

In 2019, the car sales volume of Geely, SAIC-GM and Ford were down by 9.3%, 25.7% and 26.1%, respectively. This affected the sales volume of the Company's interior trim and chassis system, and the revenue of the two segments was RMB1,650 million and RMB1,047 million, respectively, down by 25.64% and 10.28%, respectively. Another two segments of shock absorbers and automotive electronics stayed flat, recording an income of RMB2,342 million (+1.50%) and RMB128 million (+1.30%), respectively.The gross margin decreased by 0.6 ppts to 26.29% in 2019, and the net profit margin declined by 4.04 ppts to 8.58%. The period expense ratio was 15.6%, up by 2.2 ppts from the previous year. The expense ratio of sales/administration/R&D was 5.36%/10.15%/5.87%, respectively, which was mainly because of the rapid increase in administration expense rate (the increase of wages and depreciation and amortization) and R&D cost rate (the increase of R&D input).

The Results of Q1 2020 Outperformed the Market

In Q1 2020, the Company recorded a revenue of RMB1,208 million, down by 2.98% yoy. The net profit attributable to the parent company was RMB114 million, up by 0.14% yoy. The performance of the Company obviously outperformed the market, and the main contribution came from Tesla's localization project. The period expense ratio was 16.39%, up by 0.58 ppts yoy, among which the expense ratio of sales/administration/R&D was 5.46%/4.15%/6.22%, respectively. The R&D input remained high. The result of the Company had been dragged by the high depreciation brought by the new production lines in the early stage. It is expected that as the capital spending slows down, the pressure of depreciation and amortization will be significantly reduced, and the expense ratio of the whole year will keep steady.

Non-public Offering and Production Expansion will Promote the Company to Grow with High-quality Customers

In recent years, the Company has proactively made a layout of the module of the lightweight chassis system and the automotive electronics business as the future strategic development project, in order to adapt to the trend of electrification, intellectualization and lightweight of vehicles. As one of the four core systems of automobile, the automotive chassis system is capital-intensive and technology-intensive, and of high single vehicle value. We believe electrification and lightweight is the direction of the automobile industry in the future.

The lightweight chassis system plays an important role in improving the endurance mileage of the new energy vehicle, and the comfort and controllability of the vehicle. The application of parts of the lightweight chassis system in the whole vehicle, especially the new energy vehicle will be deepened continuously. The Company continues to increase the investment in innovation and make the layout of the supporting capacity of new energy vehicles and the R&D input of lightweight products. Currently, various light alloy products and lightweight chassis developed by integrating many processes such as aluminium alloy have achieved the recognition of customers at home and abroad, especially new energy vehicle enterprises. Now, Tuopu has entered the supply chain of manufacturers such as Tesla, Geely, BYD, BAIC, Great Wall, NIO and WM.

Investment Thesis

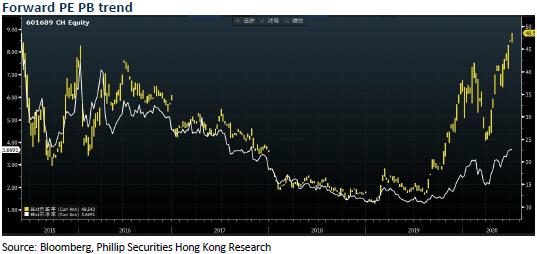

We revised the estimate that the company's net profit in 2020/2021 will reach RMB 654/980 million, respectively, with the corresponding EPS being RMB 0.62/0.93. Although the stock price recorded a significant increase, under the acceleration of Tesla's localization, the Company's results will usher in an inflection point and we are optimistic about the development prospects of the company's lightweight business and automotive electronics. So, we lift the Company's target price to RMB30, respectively 48/32 x P/E, 4/3.6 x P/B for 2020/2021, a "Accumulate" rating. (Closing price as at 3 July)

Risk

Price war among peers

Raw material price increase

New business risk

Financials

Click Here for PDF format...