Investment Summary

Review of 2019 Results: Performance Dragged by the New Energy Vehicle Business

Inovance Technology undertook heavy pressure on operations in 2019, and the fluctuation of the external macro-environment had greatly impacted the industrial control industry. Meanwhile, the subsidy decline also had a great impact on the new energy vehicle business of the Company. As a result, the target of operating results had not been reached. The total revenue of the Company in 2019 was RMB7.39 billion, up by 25.81% yoy, which was mainly resulted from the consolidation of BST of RMB1.4 billion. The revenue of the Company was approximately RMB6 billion after deducting the revenue of the consolidation, up slightly by 1.9% yoy. Net profit attributable to the parent company was RMB952 million, down by 18.42% yoy. If deducting the revenue of the consolidation, the net profit decreased by 25% yoy to RMB854 million. The EPS was RMB0.55. The cash dividend per share was RMB0.18, and the dividend payout ratio was 33%.

The integrated gross margin in 2019 was 37.65%, a decrease of 4.16% compared to the same period in 2018. The consolidation of BST also had a negative impact on the gross margin. The integrated gross margin of the Company's original business was 40.85%, down by 0.96% yoy. The main reason for the decline was the drop in the gross margin of automotive electronic products and mechanical products. Besides, the increased personnel and financial expenses, as well as the reduction of the tax rebate of value-added tax and software tax also dragged the gross margin of the Company.

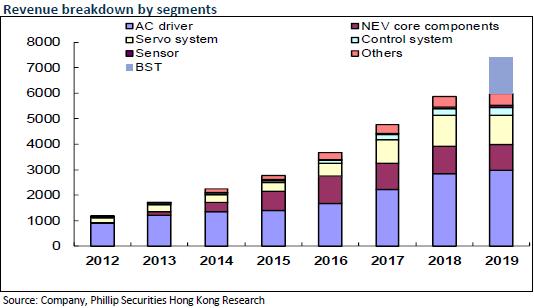

Among the major business sectors,

1) the revenue of automation business was RMB2.9 billion, an increase of 1.3%, which was mainly influenced by the downward economy and the China-US trade war. However, the gross margin rose steadily.

2) The revenue of the new energy vehicle business slumped by 22.5% to RMB652 million influenced by the sharp decrease in subsidy. The general slide of the unit price put the gross margin under heavy pressure, and the loss increased.

3) The elevator business reaped a revenue of RMB2.82 billion, mainly due to the consolidation of BST in the second half of the year.

4) The revenue of railway transportation was RMB349 million, a substantial yoy increase of 64.62%, turning losses into profits.

Nevertheless, the net operating cash flow of the Company was RMB1.36 billion last year, up by 189% yoy. The cash backflow was better than ever before. The main reasons were the larger collection of payments in cash in 2019 and the net cash inflow generated by the consolidation of BST.

Business Recovered in 1Q2020, with Nearly 30% Increase in the Net Profit Driven by Multiple Factors

In 1Q2020, the Company reported a revenue of RMB1,548 million, up by 40.7% yoy, and the net profit attributable to the parent company was RMB172 million, up by 33.6% yoy. The net profit increased by 30% deducting the amount generated by the consolidation of BST. The results of the Company rose against the background of the epidemic in China in Q1, and the main reasons are presented as follows:

1) The Company seized the opportunities for mask machines and melt-blown cloth equipment as well as domestic alternatives due to the delayed supply of foreign-funded brands, and raised the income of high-gross margin general servers for products and control systems rapidly.

2) It effectively reduced costs and enhanced effectiveness, the gross profit of servers, control systems, and integrated elevator and escalator controllers increased year by year.

3) It smoothly resumed work and production and practically controlled the epidemic.

4) The drawback and subsidies for VAT software grew. And

5) The first quarter last year was a low point of performance.

Meanwhile, the Company developed operating objectives for 2020: It aims to raise the revenue and net profit attributable to the parent company by 20%-40% yoy.

Take the Lead in Recovering from the Epidemic

In the face of the changing market, the Company proposed the business strategy to seek leading customers in the industry, and exerted many efforts on the regional retail market, and made certain achievements. In 2019, it recorded RMB7.34 billion worth of new orders (excluding BST), which fell by 5%. New orders in 1Q2020 reached RMB1.67 billion, greatly increasing by 35% yoy. The epidemic has accelerated the import substitution of the domestic automation control industry, and the Company has also taken the lead in recovering from the epidemic.

Recently, the Company has announced that it has obtained the exclusive supply of its electronic control products for the new energy vehicles of a famous European auto company. This significant achievement indicates that the Company has been recognised by international auto companies in the electronic control of new energy passenger vehicles. Looking ahead, the Company will develop in line with two logics. First is technology-based extension which is beneficial to give full play to its technical advantages. Second is market-oriented new solutions of new products for the existing customers. Along with the constant improvement of competitiveness, we are optimistic that the Company will continuously benefit from the increase in market share.

Investment Thesis

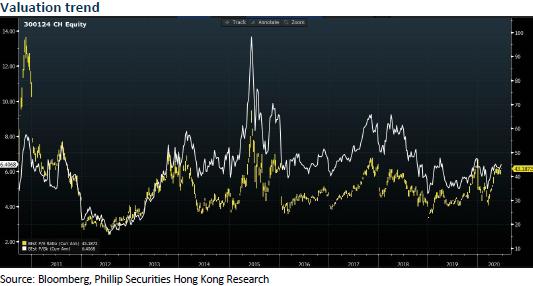

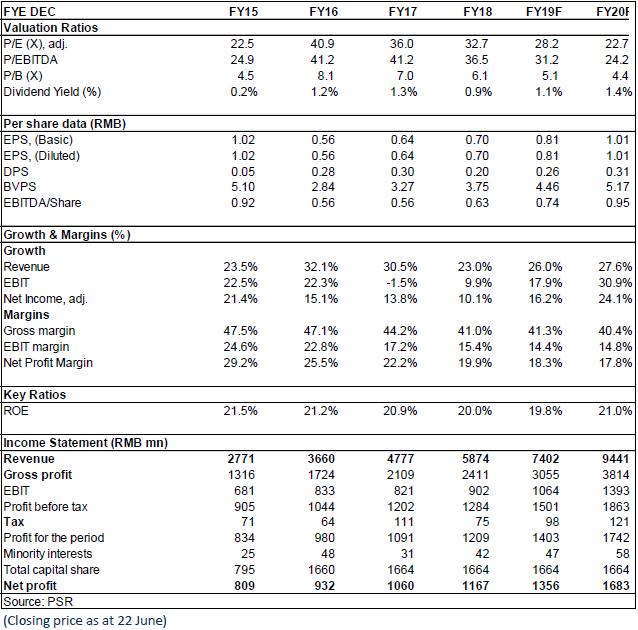

As for valuation, we expected diluted EPS of the Company to RMB 0.81 and 1.02 of 2020/2021. And we accordingly gave the target price to RMB39, respectively 48/38x P/E and 7/6.2x P/B for 2020/2021. "Accumulate" rating. (Closing price as at 22 June)

Financials

Click Here for PDF format...