Investment Summary

Results Maintained Rapid Growth

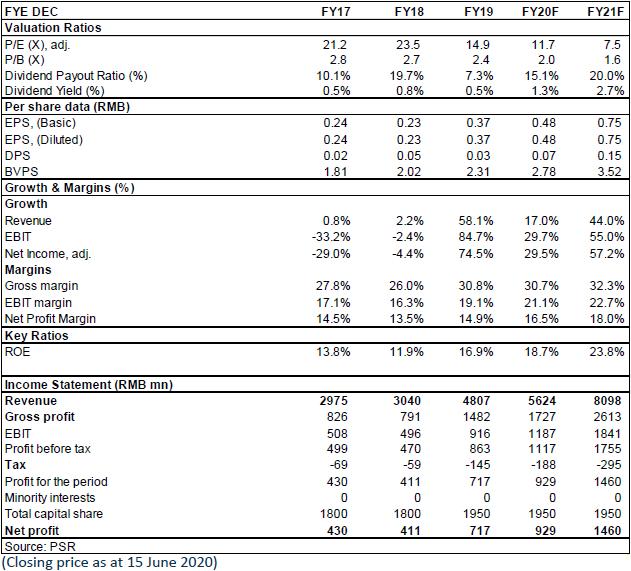

Flat Glass recorded a revenue of RMB4,807 million in 2019, up by 56.9% yoy because of the rise of unit price resulting from commission of new production capacity and the recovery of demand. The Company reported net profit attributable to the parent company of RMB717 million, up by 76% yoy; a net cash flow from operating activities of RMB510 million, up by 18.4% yoy; a weighted return on equity of 17%, up by 5% yoy.

Both the Quantity and the Price Increased, with Revenue from PV Glass Accounting for Nearly 80%

In 2019, the sales volume of PV glass of the Company reached 160 million square meters, up by 67% yoy. The gross margin of the Company increased by 5.18 ppts to 32.87% because of the recovering price of PV glass, improvement of production efficiency of the newly-commissioned production capacity and improvement of product mix (thin glass accounted for a higher proportion).

On a closer look, the Company reported revenue of RMB3.75 billion, RMB171 million, RMB451 million and RMB336 million, respectively, from PV glass, float glass, engineering glass and home glass, up by +79%, +9%, +14% and +1% yoy, respectively. Segment gross profit margins was 32.9%, 12.4%, 22% and 28.1%, respectively, which changed by +3.04, -2.83, -2.6 and +0.9 ppts yoy, respectively. The proportion of revenue from PV glass increased to 78%, approaching 80%. Total production capacity increased to 5400 tons/day.

In Q1 2020, the Company recorded a revenue of RMB1,203 million, up by 29.10% yoy and down by 15.6% qoq; net profit of RMB215 million, up by 97.0% yoy and up by 2.6% qoq. Because of the continuance of effect of price yoy lift of PV glass, plus with the low material price, 2020Q1 gross margin continued to hike, reaching a historic height of 39.88%.

In 2019 and Q1 2020, the Company recorded an administration and R&D expense ratio of 6.8% and 5.8%, respectively, down by 0.8 ppts and1.4 ppts yoy, respectively. However, the sales expense ratios were 5.31% and 5.8%, up by 1.12 ppts and 1.25 ppts yoy, respectively, which is mainly because of the increase in transport unit price.

The Pandemic Delay the Demand, but the Prospect of the Industry May Continue in H2

In 2019, domestic PV market tightened, but great performance was reported in overseas market, with export increasing rapidly. Strong overseas momentum was continued in Q1 2020, which compensated the shortage of domestic demand due to domestic suspense of work. In Q2, the delay of overseas demand caused by the pandemic put pressure on the price of PV glass, which may exert some negative impact on the results of the Company in 2020 Q2. However, the revenue from European and American markets only accounted for 10% of the total revenue of the Company. We expected that the demand side will improve steadily from H2 because of the reopen. Looking forward, the PV industry has entered the phase of scale competition. The concentration of the industry continuously roused, and the total market share of the Company and Xinyi Solar has exceeded 50%, which helped the double-oligarchy layout taking shape.

CB and Private placement Will Release the Debt Pressure, and Promotion of Equity Incentives Will Improve Long Term Growth Vitality

In recent years, the Company proactively increased production, which resulted in relatively high pressure on capital expenditure. In the recent three years, capital expenditure reached RMB550 million, RMB1.26 billion and RMB1.3 billion, respectively, and the debt-asset ratio reported 45%, 47%, and 52%, respectively. Recently, the Company announced that it would release convertible bonds of RMB1.45 billion and Private placement of RMB2 billion, which were mainly used in the production and construction of the two 1,200-ton-per-day production lines (Line 4/Line 5), as well the preparation and construction of Line 6/ Line 7 (also 1,200 tons per day) in Fengyang, Anhui. Due to obvious advantages in technology and scale of newly increased capacity, increase in finished production rate and decrease in unit cost will further improve the profitability of the Company.

The Company released an incentive plan on equities of A-share (draft) in April, which intended to grant 6 million restricted shares of the Company to 16 middle and senior level management personnel and key technical personnel if the yoy growth ratio of revenue is no lower than 0%, +20%, +25%, +13% and +17%, respectively from 2020 to 2024. The plan aimed at binding benefits of employees with the Company to ensure the steady and healthy growth of future results.

Investment Thesis

Considering the epidemic, we decide to revise target price to HK$7 for the Company, equivalent to 2020/2021 E 13.4/8.6x P/E, Accumulate rating. (Closing price as at 15 June 2020)

Financials

Click Here for PDF format...