Investment Summary

Profit in 2019H2 Was Slightly below Expectations and One-off Factors Resulted in the Decrease of Gross Margin

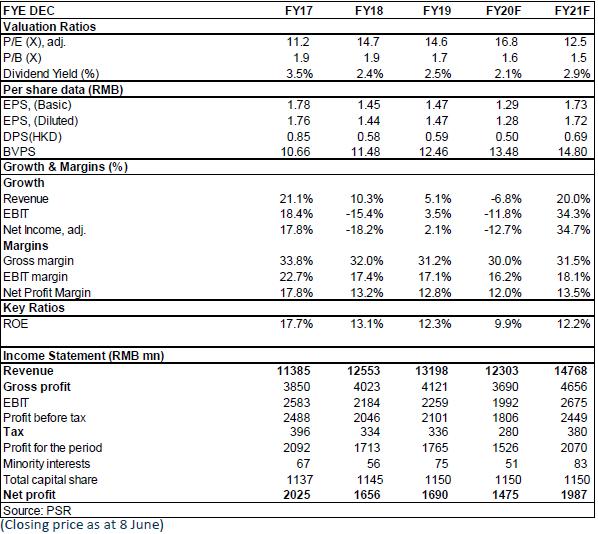

In 2019, Minth Group's turnover amounted to RMB13.198 billion, up 5.1% yoy, mainly from business growth in overseas markets, especially in Europe and North America. Net profit attributable to shareholders stood at RMB1.69 billion, up 1.8% yoy. Basic EPS was RMB1.472 and proposed dividend was RMB0.588, maintaining a high and stable dividend payout rate of nearly 40%.

Profit was approximately 6% lower than expectations, mainly because gross margin reached 30.19% in H2 due to the following factors, at lowest in five years, down 2.23 ppts hoh and 0.58 ppts yoy.

(1) New products delivered by German factories failed to meet expectations in H2, resulting in a large increase in labour costs.

(2) New facility of Huaian is put into operation and still in the climbing period, with insufficient capacity utilization and high depreciation cost.

(3) Despite some of the business had been transferred to Thailand, the US-China trade war tariffs affected about 7% of the Company's business, resulting in a decrease of 0.6 ppts in gross margin.

Now the situation of German plant has improved from the second half of last year, and the production and operation of Huaian plant have picked up and met expectations.

Orders in Europe Increased Steadily, and the Expenses Ratio of Administration and R&D Increased

Revenue from the Company's overseas market in 2019 has increased 13.8% yoy due to the increase of orders from BMW, Audi, Daimler and GM. The European business proportion of revenue increased from 15.1% to 16.9% and the North American business proportion increased from 18.9% to 20.9%.

Meanwhile, product mix has continued to be optimized, and the aluminium products have maintained double-digit growth. These are dominant factors for the Company's turnover bucks the trend of recession in the global vehicle market.

The administration expenses rate increased by 0.5 ppts yoy to 7.9%, mainly due to higher employee wages and more personnel at new plants. The R&D expenses increased by 11.0% yoy to RMB660 million, and the R&D expenses rate increased by 0.3 ppts yoy to 5.0%, mainly due to the Talent Scouting and the R&D of new products. The Company plans to strictly control the expenditure of sales, administration to a reasonable level this year, while low cost in raw materials such as aluminium will improve its profitability.

The Company's CAPEX declined from RMB2.23 billion to RMB1.67 billion last year, and the net cash flow of operating activities was RMB2.38 billion, with the free cash flow turning from negative to positive.

The Impact of the Pandemic is Gradually Diminishing, Prosperous Future Unchanged

Minth's domestic business has returned to normal in April with the weakening of the pandemic and the resumption of work in various places. The recovery of overseas markets will be a bit slower, with European plants resuming work since late April/early May and U.S. plants resuming work since mid-May. The business of overseas is expected to return to normal in June-July.

Minth Group has been committed to the expanding of product lines and the optimization of product mix. The Company has further developed and expanded products in the field of new energy vehicles such as aluminium battery packs, aluminium door frames and ACC signs in recent years. The aluminium battery pack business has been implemented first and has entered the supplier system of global electric vehicle platform of main engine factories, such as Europe, Japan, the United States and China. The business has received orders from many global projects, making Minth one of the largest suppliers of aluminium battery pack in the world. The aluminium door frames have reached level of mass production, and the intelligent exterior decorative products also progress smoothly, obtaining a lot of designated projects and orders of ACC products from Japanese and European customers.

At present, the new orders of the Company are 4.6 to 4.7 billion. The target of 7.5 to 8 billion new orders for the whole year is maintained. Although the pandemic has brought challenges to the auto industry in H1, it is assured that there will be a strong result rebound after the pandemic because the Company has abundant orders, high-quality customer structure, gradual mass production of new models and huge improvement prospects in overseas business.

Judging from new energy strategic plan of major vehicle enterprises across the world, most of them regard the year of 2020 or the year of 2025 as the ``critical year`` for new energy planning. New orders are expected to explode with the acceleration of overseas electrification of vehicles.

Valuation

Considering the impact of the epidemic this year, we revised the forecast of EPS of 2020/2021 to be 1.29/1.73 yuan. And we believe that it is reasonable to give the company a valuation of 19.2/14.3x P/E and 1.8/1.7x P/B for 2020/2021, equivalent to target price of HK$ 27.45 and Accumulate rating. (Closing price as at 8 June)

Financials

Click Here for PDF format...