|

MENGNIU DAIRY(2319)

Analysis¡G

China Mengniu Dairy (2319) continues to expand its overseas business coverage to speed up the implementation of the international business plan. In 2019, Mengniu conducted two strategic acquisitions to implement overseas strategic layout and realize long-term strategies. It completed the acquisition of Bellamy`s, an Australian organic infant formula and baby food producer, in December 2019 and entered into an agreement for the proposed acquisition of 100% shares of Lion-Dairy & Drinks (LDD), an Australia-based branded dairy and beverage company. The acquisition of Bellamy`s is in line with Mengniu`s strategies of achieving breakthrough growth in the premium infant milk formula segment and expanding into overseas markets with a focus on Southeast Asia and Australia. The acquisition of LDD will help Mengniu develop high-end UHT milk. Both acquisitions allow the Group to not only swiftly enhance its competitiveness and take control of high-quality milk sources, high-end organic infant formula and baby food brands, and long-established brands of high-end liquid milk, but also to further its business in the domestic and overseas markets, especially in Australia and the Southeast Asian region. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $29.00, Target Price: $31.00, Cut Loss Price: $28.00

|

SF HOLDING(002352.SZ)

Analysis¡G

The company is a leading integrated express logistics service provider in China. As of the end of 2019, SF express has successfully deployed industrial park projects in 45 cities across the country, with a first-mover advantage. Among them, the layout of the logistics land area is 7089 acres, and the total planned construction area is about 4.182 million. The latest Securities Regulatory Commission and the National Development and Reform Commission jointly issued a document proposing to give priority to supporting infrastructure supplementary board industries, including storage and logistics, toll roads and other transportation facilities, to promote toll road REITs issuance.

Strategy¡G

Buy-in Price: RMB49.30, Target Price: RMB53.80, Cut Loss Price: RMB46.00

Matsuoka Corporation ¡]3611¡^

Founded in 1956 as Matsuoka Gofukuten (kimono shop). In addition to planning, manufacturing and distribution, the company operates an ¡§Apparel OEM Business¡¨ which manufactures clothing under consignor brands by receiving orders from apparel manufacturers, trading companies and mass retailers.For FY2020/3 results announced on 22/5, net sales decreased by 9.9% to 57.112 billion yen compared to the previous year and operating income decreased by 22.6% to 2.603 billion yen. Despite an increase in orders received mainly in casual wear for major SPA in the latter half, changes to the distribution policies of clients and production adjustments in the apparel industry following climate factors in the first half have affected, which lead to a decrease in sales and income.Their FY2021/3 plan is undecided due to uncertain effects from the spread of COVID-19. Company was chosen as one of the 5 suppliers for the cloth masks currently being distributed by the government, and the absence of problems faced in their collection has raised their rating. In addition, UNIQLO, which is under Fast Retailing (9983), will enter the mask business this summer, and the production and retail of cloth masks made from breathable material which prevent stuffiness when worn is also likely to benefit the company's performance.Target Price : 2,500 yenBuy Price : 2,129 yenCut-Loss : 1,900 yen

|

|

|

Report Review of May. 2020

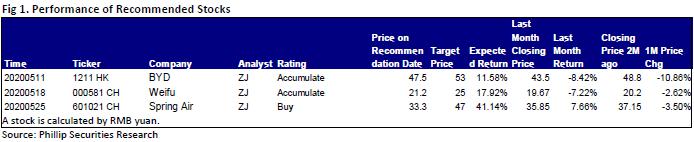

Sectors: Air & Automobiles (Zhang Jing), Automobile & Air (ZhangJing)This month I released 3 updated reports of BYD (1211.HK)¡AWeifu (000581.CH)¡Aand Spring Airlines (601021.CH), which got success by their unique Competitive edge. Among them, we highly recommend Spring Airlines. Spring Airlines, the leader of the low-cost airlines in China, is the first private low-cost airlines in China. No matter in terms of the size of the fleet and the number of routes, or of the passenger traffic, Spring Airlines is far ahead in the domestic low-cost airline market. The unit operating cost of the company is 32%-37% lower than that of the other three major airlines. With a significant cost advantage, the company is able to launch products at lower prices. The company provided tickets with prices 30-45% lower than that of full-service airlines. Such advantage in cost effectiveness attracts numerous self-paying passengers who are more sensitive to prices as well as business travellers pursuing high cost effectiveness, Maximizing the use of existing assets has recorded efficient production operations. The company's yield and P L/ F are much higher than that of other domestic airlines, which reflects its excellent capabilities for operations. China's low-cost airlines started developing late and are still in the early stages of development, with a low penetration rate. The company has vast development space, and has the first-mover advantages and a "barrier", which help it to fully enjoy the industry dividend. We believe that short-term impact caused by the epidemic does not change the long-term investment value of the company. As for valuation, we expected diluted EPS of the Company to RMB 0.42/2.56 of 2020/2021. And we accordingly gave the target price to RMB47, respectively 2.8/2.3x P/B for 2020/2021. "Buy" rating.

Click Here for PDF format...

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2020 Phillip Securities (HK) Ltd. All Rights Reserved.

|