Investment Summary

Slump in ROI Contributes to a Slight Decline at 5% in Last Year's Results

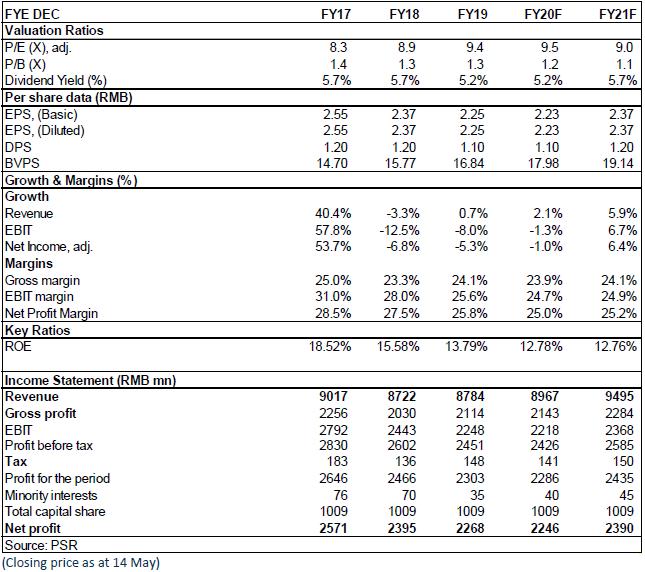

In 2019, Weifu High-Technology Group Co., Ltd. recorded total revenue of RMB8.78 billion, an increase of 0.7% yoy. The net profit attributable to the parent company reached RMB2.27 billion, down by 5.3% yoy, while net profit attributable to the parent company excluding non-recurring items reached RMB1.947 billion, down by 3.34% yoy. Earnings per share was RMB2.25. The figure was RMB2.37 in last year. The result was slightly (about 1%) above our expectation. The cash dividend per share was RMB1.1, with a dividend payout rate of 49%, maintaining a high dividend payout rate.

The ROI was RMB1.61 billion, down by 17% yoy. The ROI from Bosch Automotive Diesel Systems Co., Ltd. and Zhonglian Electronics Factory Co., Ltd. decreased by 11% and 24%, respectively, accounting for two-thirds of the company's total profit. The ROI contributed by wealth management plans fell to RMB240 million from RMB310 million in the previous year.

Increase in Sales Price Has Improved the Gross Margin though the Sales Volume Has Declined

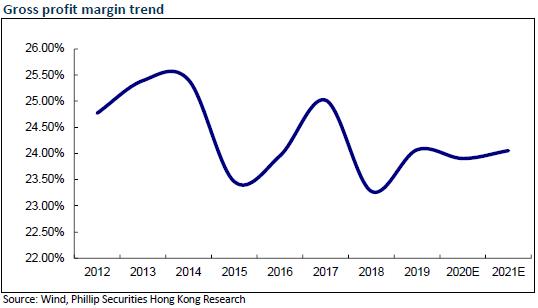

The auto market in 2019 was affected by the economic downturn and the decline in consumer demand, with the overall sales volume declining. The sales volume of the company's main products is under pressure: The sales volume of fuel pumps fell by 2.8%, that of post-processing systems fell by 32%, and that of intake systems fell by 2.8%. However, profitability has improved as a result of higher average product prices brought by the upgrade of the China VI Emission Standards. Revenue from fuel injection systems was RMB4.87 billion, down by 3.1% yoy, and gross margin was 30.28%, up by 1.06 ppts yoy. Revenue from post-processing systems was RMB3.04 billion, up by 8.64% yoy, and gross margin was 14.3%, up by 2.3 ppts. Revenue from intake systems was RMB446 million, up by 1.26% yoy, and gross margin was 27.4%, down by 0.8 ppts. The overall gross margin also improved by about 1 ppt to 24%.

Net Profit Decreased by 20% in Q1 2020 under the Pandemic

In the first quarter of 2020, the company achieved a revenue of RMB2.772 billion, up by 22.11% yoy, and the net profit attributable to the parent company reached RMB550 million, down by 20.2% yoy. Gross margin fell by 4.3 ppts yoy to 18.81% under the pandemic, which is estimated to be mainly due to the increase of the revenue percentage of the post-processing system products with low gross margin. In the first quarter, the natural gas engine post-processing products produced by WFLD, the company's subsidiary, recorded a high growth, driven by a 25% increase in domestic sales volume of natural gas heavy trucks.

In addition, the pandemic affected the pace of sales of major affiliates in the first quarter. The declined short-term results resulted in the company's net ROI at RMB363 million, down by 18.5% yoy, which is also a significant factor. However, ROI is expected to gradually recover as the domestic auto market gradually recovers.

The Prosperity of the Heavy Truck Industry Is Expected to Continue under the Countercyclical Policy Environment

Aiming at boosting the economy, the government authorities are strengthening the countercyclical adjustment policies. Ministry of Finance has expanded the issuance scale of local government special bonds, and multiple provinces and municipalities an intensive range of investment plans. The growth of infrastructure is expected to be recovered, which will subsequently drive the demand for engineering heavy trucks. At the end of March, the State Council announced a policy of bonus for compensation from the central budget for supporting the phasing out of the diesel cargo trucks under or below the China III emission standard in key areas such as Beijing-Tianjin-Hebei. Meanwhile, a value added tax at the rate of 0.5% based on the sales revenue will be imposed from May 1 to the end of 2023 for the used vehicle sales of second-hand automobile dealers. A high drive of heavy truck sales is expected from the demand upgrade caused by the phasing out of diesel trucks and gears falling on or below the China III emission standard.

The company is expected to benefit from the competitive advantages in the core power system components of heavy truck engines, advanced exhaust treatment technology and abundant product reserves.

Presence in new fields of fuel cell components and automotive chips

The company recently announced the purchase of 66% of equity in IRDFuelCellsA/S for EUR7.26 million, and the joint investment of RMB200 million to set up a semiconductor device and integrated circuit enterprise. The former has a number of patents in the field of fuel cells, involving membrane electrodes and bipolar plates, and its products in Europe, the United States, China and other regions have stable technical partners and customers. The latter is in line with the "New Four" (electric, networking, intelligent, sharing), which is an upgrade trend in the automotive industry. We believe that these two extensive mergers and acquisitions are helpful for the company to cultivate new business growth points and achieve strategic transformation and upgrading of product lines.

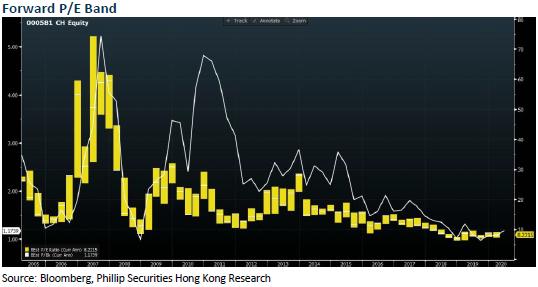

Valuation

The company holds abundant cash flow and wealth management plans, with stable operation style, providing a foundation for the future merger and acquisition transformation and high dividend. As analyzed above, we expected diluted EPS of the Company to RMB 2.23 and 2.37 for 2020/2021. And we accordingly gave the target price to 25, respectively 11.2/10.6x P/E for2020/2021. "Accumulate" rating. (Closing price as at 14 May)

Financials

Click Here for PDF format...