Investment Summary

Obvious Characteristic of High in the Beginning and Low at the End regarding Profit in 2019

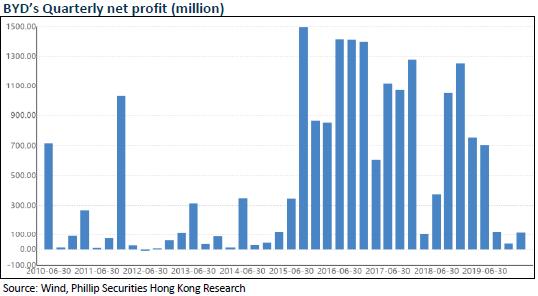

BYD recorded revenue of RMB121,780 million, basically levelled with the previous year. Net profit attributable to the parent company decreased by 42% to RMB1.6 billion. The EPS was RMB0.5, with a dividend paid of RMB0.06 per share. In the four quarters, the net profit of the Company was RMB750 million, 705 million, 120 million and 40 million, respectively, up by 236.4%, up by 24.5%, down by 80.6% and down by 84% yoy, respectively. Regarding profit, there was obvious characteristic of high in the beginning and low at the end, which was consistent with the fluctuation of domestic new energy vehicle industry which resulting from the retreat of subsidy policy and switch to China VI vehicle emission standards.

The sales volume of new energy vehicles of the Company in H1 and H2 of 2019 was 146,000 and 84,000, respectively, up by 94.5% and down by 51.5% yoy, respectively, and down by 7.4% throughout the year. The sales volume of traditional fuel vehicles was 232,000, down by 15% yoy. The gross margin of the car sector was 21.9%, with the operating profit margin being around 4.7%. Overall, the contribution from the car sector throughout the year remained stable, slightly down by 3.6% yoy, accounting as much as 56% of total operating profits. The car sector was still the biggest result contributor.

The mobile phone sector was impacted by the fierce price competition of metal parts in 2019. The gross margin dropped by 9.4% to 3.2 ppts, the operating profit margin fell by 3 ppts to 3.4%, and the operating profit contribution of the mobile phone sector decreased by 33% yoy.

The PV market was obviously rebounding. The cell/PV business increased to a certain extent, with revenue being up by 12% yoy.

Epidemic Resulted in Pressure in 2020 Q1 Results of the Car Sector

In Q1 2020, the Company reported a revenue of RMB19,679 million, down by 35.1% yoy. Net profit was RMB113 million, down by 85% yoy. Given that the mobile phone business of BYD E(285.HK) recorded net profit of RMB660 million, it can be deduced that the car sector and cell/PV sector generated a loss of around RMB320 million.

Impacted by the epidemic, the sales volume of cars of the Company was 61,000, down by 48% yoy. Among them, new energy vehicles was 22,000, down by 70% yoy, and 39,000 fuel vehicles were sold, down by 12% yoy. The epidemic seriously impacted the production capability utility rate and gross margin of the car sector. Luckily, some of the impact was set off by the increase of 4.4 ppts of gross margin in the mobile phone sector. Thus the overall gross margin of the Company dropped by 1.4 ppts.

Result Guidance Indicates the Significant Improvement of Results in Q2

Meanwhile, the Company predicts that the net profit attributable to the parent company from January to June in 2020 will be RMB1.6 billion to RMB1.8 billion, up by 10% to 23.75% yoy. This is mainly because of the significant improvement in the profitability of BYD Electronic, the Company's subsidiary. There will be no less than a 280% of increase yoy. In other words, the mobile phone sector will contribute at least RMB1 billion of net profit in Q2. Based on this, in Q2, net profit of the car sector and cell/PV sector will be between RMB487 million and RMB687 million, which will be a great improvement compared to Q1's loss.

The Company suggests that the reason for the great increase of profits in Q2 are:

1) With the gradual disappearance of impact of the epidemic in China, the car industry will recover steadily. The subsidy policies are relatively positive. The sales volume and revenue of new energy vehicles will get out of the trough and experience a recovering increase. Meanwhile, new blade cells and technologies including DMI will be fully launched, which is beneficial to reducing costs and improving profits. In terms of fuel vehicles, led by the hot sale models including "Song pro", it is estimated that the sales volume will be large.

2) With respect to skyrail business, because of the acceleration of infrastructure construction projects of local governments, the business has profited in Q1 and will become a new profit increase engine in the future.

3) As for the mobile sector, the market share of main customers has been increasing and the business scale has been enlarging. Meanwhile, the outcome of introducing new spare parts and accessories is shown and the production volume of mobile phone parts made of glass ceramics and other materials has been increasing rapidly. Therefore, the profitability will be significantly improved in Q2. In addition, mask production will also contribute positively.

4) Regarding the PV sector, impacted by the overseas epidemic, it is estimated that PV business will suffer pressure in Q2.

Investment Thesis

Transformation Pays, Maintaining Accumulate Rating

We believe that the technological progress and transformation of BYD in recent years will activate its overall competitiveness again, which will enable it to enlarge its market shares in the coming reshuffling period. Advance position in a qualified race track, forward-looking layout and outstanding capability to implement are helping the Company to enter a result realizing period with multiple harvest businesses. Therefore, although there are various challenges in the future, we believe that the Company is entering into a growth period with more stability and sustainability.

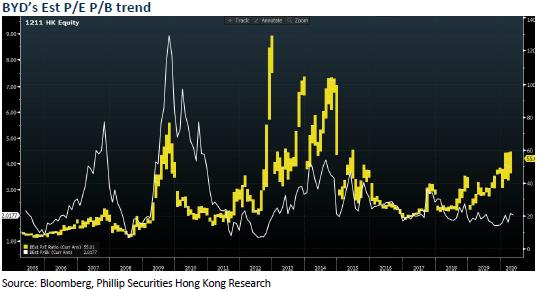

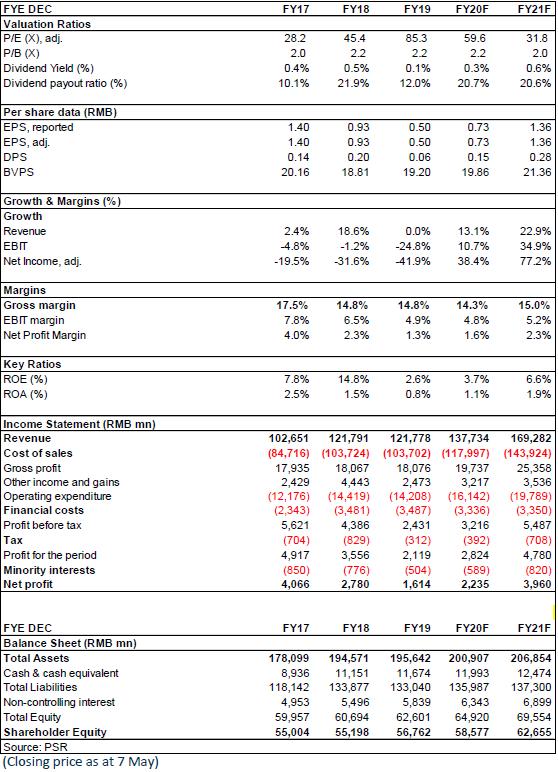

As the latest estimates, we revise the target price to HKD53, which corresponded to 2.4/2.3x P/B and 65.5/35.5 x P/E ratio for 2020/2021. We give the rating of ¡§Accumulate¡¨. (Closing price as at 7 May)

Risk

Sales of NEVs is not as good as expected

Cloud Rail business risk

Slow-down of Hand-set components business

�Financials

Click Here for PDF format...