Investment Summary

Annual Sales Volume was Better than Expectation

The year of 2019 has witnessed a continued booming in the heavy truck industry in China. The annual sales of heavy trucks hit a fresh record of 1.174 million units, according to data from CAAM (China Association of Automobile Manufacturers). It drove the annual sales of Weichai engines to 742,000 units, up by 10.1% yoy, Shaanxi Heavy Duty Automobile to 161,000 trucks, up by 5.2% yoy, and Fast Gear to 1.002 million units, up by 10.2% yoy.

Sales Promotion and Raw Material Cost Rise in Q4 Posed a Drag on Gross Profit

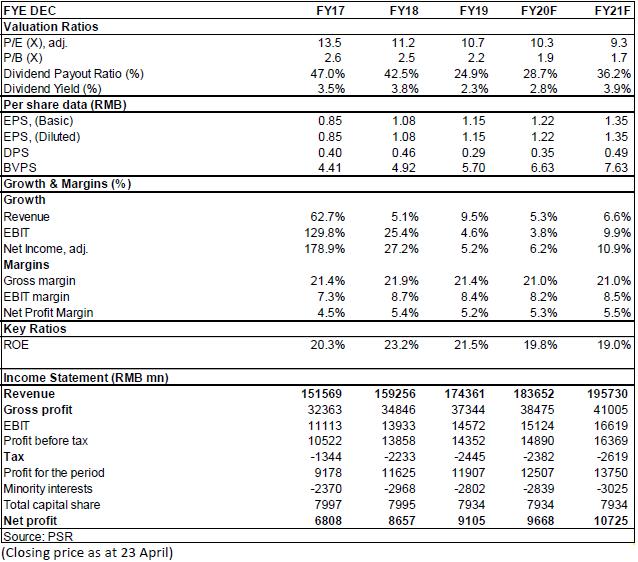

In 2019, Weichai recorded a revenue of RMB174.4 billion, up by 9.5% yoy, and a net profit attributable to the parent company of RMB9.1 billion, up by 5.2%, but slightly lower than the expectation mainly due to a drop in the Company's net profit in the fourth quarter (RMB2.047 billion) by 22.9% yoy. Weichai stepped up efforts in sales promotion and marketing in the fourth quarter in a bid to promote trucks and engines of the China VI emissions standard and take the market share, leading to the rise in short-term cost. In addition, the price increase in the precious metal raw material resulted in a drop in the engine gross margin in the fourth quarter. Currently the precious material price has fallen back from the fourth quarter of last year. Meanwhile, through investing in R&D, the Company has achieved a lower consumption on precious metal. The current consumption per unit has dropped by 20-30%. The gross margin is expected to recover to a normal range when the production recovers after the work resumption.

In terms of income in 2019, Weichai engines reported a revenue of RMB45.76 billion, up by 14.7% yoy, Shaanxi Heavy Duty Automobile, RMB54.4 billion, up by 6.4% yoy and Fast Gear, RMB15.11 billion, up by 8.5% yoy. Having the benefit from the execution of previous orders, KION recorded a revenue of RMB67.18 billion, up by 11.0% yoy.

As for the profit contribution, the engine recorded a net profit of RMB7.36 billion, up by 9.2% yoy, among which the net profit in the fourth quarter witnessed a fall by 15.2% yoy to RMB1.86 billion mainly attributed to the drop in gross margin; Shaanxi Heavy Duty Automobile recorded a net profit of RMB1.26 billion, up by 6.4% yoy, Fast Gear, RMB1.33 billion, up by 1.2% yoy, and KION, RMB2.65 billion, up by 3.3% yoy.

High Investment in R&D

The cost rate was maintained at a stable range, and the total period cost rate was 13.54%, slightly up by 0.19 ppts over the last year. The R&D cost increased by 21%, or by RMB908 million to RMB5.23 billion, mainly for investing in the electronic control sector for further bringing up the product competitiveness. The final dividend rate dropped by 5 ppts to 25%, mainly resulting from the Company's intention to enhance the rick control capability considering the impact from the potential return of the epidemic. The dividend ratio will be brought back to a normal range after the negative impact of the epidemic.

Countercyclical Policy to Secure High Demand of Infrastructure

Aiming at boosting the economy, the government authorities are strengthening the countercyclical adjustment policies. Ministry of Finance has expanded the issuance scale of local government special bonds, and multiple provinces and municipalities an intensive range of investment plans. The growth of infrastructure is expected to be recovered, which will subsequently drive the demand for engineering heavy trucks. At the end of March, the State Council announced a policy of bonus for compensation from the central budget for supporting the phasing out of the diesel cargo trucks under or below the China III emission standard in key areas such as Beijing-Tianjin-Hebei. Meanwhile, a value added tax at the rate of 0.5% based on the sales revenue will be imposed from May 1 to the end of 2023 for the used vehicle sales of second-hand automobile dealers. A high drive of heavy truck sales is expected from the demand upgrade caused by the phasing out of diesel trucks and gears falling on or below the China III emission standard.

As shown by the latest data, the engineering machinery demand has bounced back strongly in March, and the price rise suggested the recovery of supply and demand balance. In general, the impact of epidemic in China was mainly in January to February. The accumulated demand in the previous period for engineering machinery was released in March along with the quick recovery of infrastructure demand and real estate work resumption.

What's more, Weichai is furthering cooperation with Sinotruk and will benefit from the scale effects brought from increasing market share. From the middle term, the clear strategic framework of ¡§power engine + hydraulics + new energy¡¨ and the access to both the foreign and domestic market cam help the original business to offset the period fluctuation in domestic heavy truck industry and build a more balanced business system.

Investment Thesis

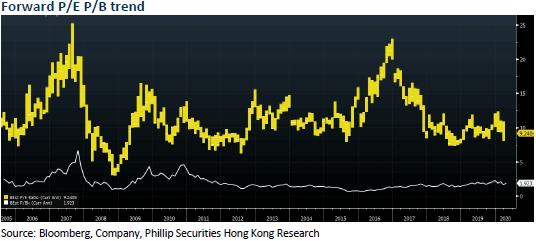

We revise the profit forecast of the company in 2020/2021 to EPS of RMB 1.22/1.35. We will also revise target price to 15.6 HKD (11.6/10.5x for 2020/2021 P/E) and Accumulate rating. (Closing price as at 23 April)

Financials

Click Here for PDF format...