Investment Summary

The Revenue Increased by More than 10%, and the Profit Increased by 18%

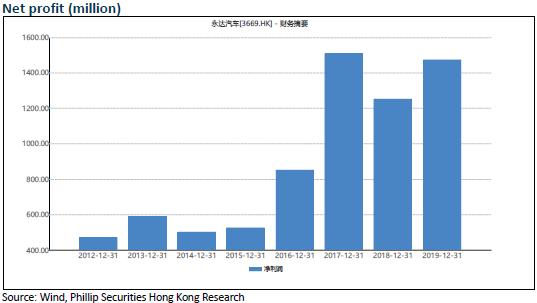

The revenue of Yongda Automobiles was RMB62.71 billion in 2019, up 13.4% yoy; the profit attributable to shareholders stood at RMB1.473 billion, up 17.6% yoy, with the EPS of RMB0.8. Considering the possible recurrence of the outbreak and the potential merger and acquisition opportunities, and for the reason of caution, the management has announced no final dividend, but will pay a dividend of no less than 30% in the middle of this year if the subsequent situation is optimistic.

The Proportion of Premium Cars Increased, and the Structure was Continuously Optimized

In 2019, the sales volume of the premium cars in China increased against the trend. Benefiting from the prosperity in the premium cars market and channel expansion, the Company's overall sales volume of new cars was up 11.6% yoy to 197,400, with the sales volume of the premium cars up 15.5% yoy to 128,600, faster than the industry average of 9.7%.

Among the segmented brands, the sales volume of BMW was up 13.5% yoy to 67,500 units, basically the same as the industry average; the sales volume of Porsche was up 25.4% yoy to 9,871, which is far higher than 8% of the industry average.

The annual sales revenue of new cars was up 13.3% yoy to RMB52.94 billion, among which the revenue of premium cars was up 14.5% yoy to RMB43.77 billion. The sales structure was further improved, and the sales volume and sales revenue of premium cars were up by 2.3 ppts and 0.9 ppts yoy to 65.2% and 82.7%, respectively.

The after-sales revenue was up 15.6% yoy to RMB8.37 billion, mainly due to the rise in the proportion of premium cars in the after-sales business of 2.2 ppts yoy to 83.9%.

The automobile finance had a sustainable development. Revenue of automobile finance was up by only 4.5% yoy to RMB1.617 billion, which was related to the moderate slowdown in proprietary finance supply of the Company. To be specific, the revenue of insurance agency business was up 10% yoy to RMB1.1 billion, while the proprietary finance business was down 6% to RMB511 million.

The car rental business maintained the consistent superiority with a rapid revenue growth of 29% to RMB530 million. The current rental fleet size is about 7800 units.

Gross Margin Basically Stayed Flat, and Operation Efficiency was Enhanced

The gross margin of the sales of new cars basically stayed flat at about 2.4%, which mainly resulted from the overall stable price and accelerated turnover efficiency of the premium cars market, and Porsche maintained a better gross margin. The inventory turnover of the Company's new cars in 2019 was down 6.6 days yoy to 36.5 days, and the inventory turnover of components was down 7.6 days yoy to 43.2 days. The expense ratio was down 0.11 ppts yoy to 6.87%. The financing costs was RMB780 million. We expect the Company to benefit from the domestic overall easing financing environment in the future.

Outlets Expansion was Kept, and the Objectives Remained Unchanged

By the end of 2019, the number of dealerships of the Company increased to 208, with a net increase of 14. Among them, there was 119 luxury brands, which had a net increase of 8. The number of those who had got licenses was 12. Within the year, there was 13 new self-built dealerships and 6 by mergers and acquisitions, including such luxury brands as Porsche/Mercedes-Benz/Lexus/Volvo/Lincoln/Aston Martin as well as the new energy brands like Tesla/WM/Xpeng/Byton.

The outbreak affected the sales in the first quarter, but now, as things get better, the Company is rapidly recovering orders and store visitors, and is expected to return to normal levels in the past in April. In view of the favourable factors such as the newly acquired stores, the increased license plate quota in Shanghai and the support policies of the automobile manufacturers, the management still maintains the original operational objectives and hopes to make up the leeway in the rest of this year.

Investment Thesis

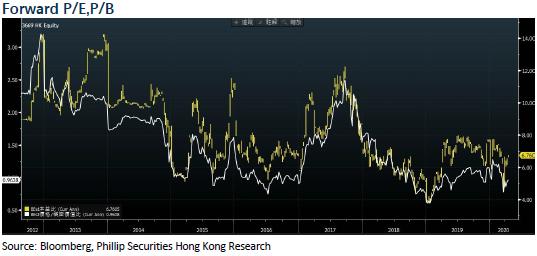

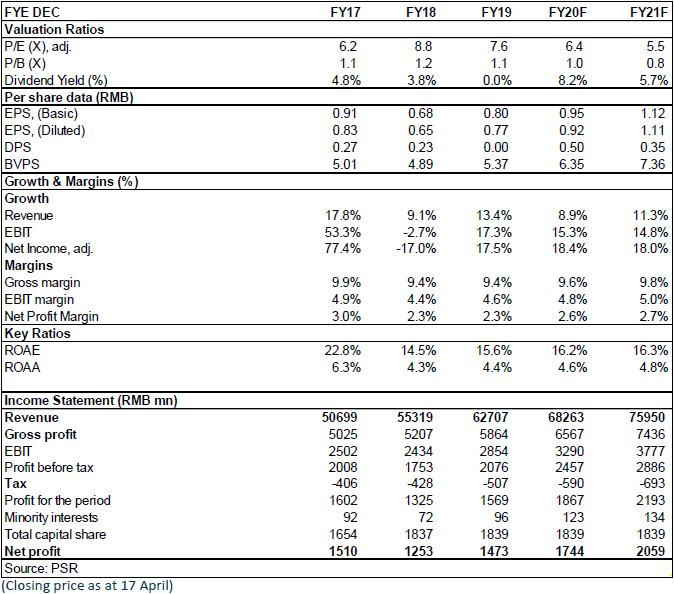

We expect the company's EPS for 2020/2021 to reach 0.92/1.11 yuan and the target price of HK$8.6, corresponding to 2020/2021 8.1/6.9x P/E. We gave a Buy rating. (Closing price as at 17 April)

Financials

Click Here for PDF format...