2019 China & Hong Kong Stock Market Review

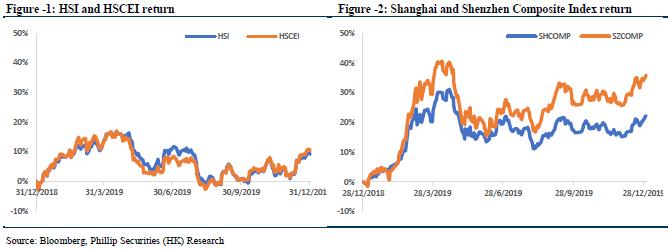

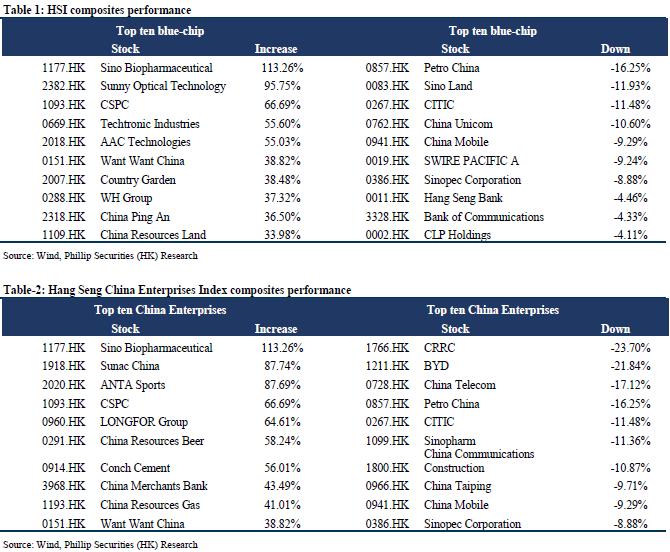

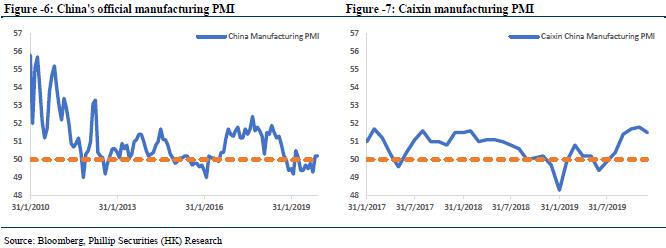

Recalling the history of China & Hong Kong stock market performance, we found that in the past year, especially the third and fourth quarter there is a greater differentiation in performance. Hang Seng Index return in 2019 was 9.07%, the Hang Seng China Enterprises Index in 2019 return was 10.30%, the Shanghai Composite Index in 2019 return was 22.30%, the Shenzhen Composite Index in 2019 return was 35.89%. By comparison, the A-share return in 2019 significantly outperformed Hong Kong market return, while the third and fourth quarter due to the stimulation of the China-US trade war news, Hong Kong market underperformed in the third quarter and outperforming in the fourth quarter. China's manufacturing PMI rebounded in November 2019, the official manufacturing PMI rose to 50.2, which is the index first time went back to above 50 after six consecutive months below 50, to return to the expansion area, also hit eight-month high, and maintained in December. Later Caixin announced its manufacturing PMI, it rose to 50.4 in August 2019 and maintained above 50, until in November rose to 51.8, also above 51.4 of this month and last month's forecast of 51.7 in a Reuters, continuous 5-month rise and the highest since December 2016. PMI shows a good trend due to improved demand and stabilized production, Caixin new orders index also maintained a high level, the economic situation continued to repair.

Mainland China Economic Outlook

A number of international financial institutions released on the world economy and China's economic growth forecasts. Organization for Economic Cooperation and Development (OECD) is expected in November, 2019 and 2020 global economic growth of 2.9%, while the mainland in 2019 economic growth was 6.2 %, an increase of 5.7% in 2020, 5.5% in 2021. The Asian Development Bank on September 25 issued "Asian Development Outlook 2019 Update", ADB forecast China's 2019 and 2020 GDP will grow by 6.2% and 6.0%, respectively. International Monetary Fund (IMF) latest on October 15 will be China 2019 economic growth forecast down from 6.2 to 6.1 percent, a further slowdown in growth next year, forecast from 6% to 5.8%, respectively, down 0.1 and 0.2 percentage points . Reuters news agency on October 14 reported that according to its business and industry survey conducted, Chinese economic growth is expected in 2019 to be reduced to 6.2%, the lowest growth in nearly 30 years, 2020 will be further reduced to 5.9%. We expect that, in view of the signing of the China-US claims is nearing completion of the first phase of trade agreements, and the Chinese economy continued to pick up, China's economic growth will be 6.2% and 5.8% in 2019 and 2020, respectively.

China & Hong Kong Stock Market Investment Strategy In 2020

From external influences, we believe that in 2020 China and Hong Kong stock market will be mainly affected by the following factors: 1) progress in China-US trade talks; 2) Brexit uncertainties; 3) the trend of the USD and CNY prospects; 4) US government fiscal and monetary policies; 5) implementation of local political factors and the risk of the Hong Kong government relief measures; 6) Middle East geopolitical crisis; 7) the economic risks caused by global political events. From the sectors point of view, we recommend attention to Guangdong-Hong Kong-Macao Greater Bay Area concept stocks that focus on regional development, China telecom stocks and semiconductor stocks driven by the rapid development of 5G technology, and consumer stocks that have benefited from mainland China's economic development and domestic demand stimulation. Blue-chips infrastructure stocks driven by economic stimulus policies and infrastructure investment, gaming tourism and auto stocks at low valuations, China's new economic stocks that are about to set off a return to Hong Kong, and insurance and pharmaceutical stocks that are more resistant to the economic cycle.

Risk Factors

Progress in China-US trade negotiations; China's economic growth risk; Hong Kong community events further deterioration; Exchange rate risk.

2019 China & Hong Kong Stock Market Review

Recalling the history of China and Hong Kong stock market performance, we found that the performances in the past year, especially in the third and fourth quarter performance there is a greater differentiation from the data:

HSI 2019 return of 9.07%, Q3 return of -8.58%, Q4 return of 8.04%

HSCEI 2019 return of 10.30%, Q3 return of -6.26%, Q4 return of 9.48%

SHCOMP 2019 return of 22.30%, Q3 return of -2.47%, Q4 return of 4.99%

SZCOMP 2019 return of 35.89%, Q3 return of 2.10%, Q4 return of 8.01%

By comparison, the A-share return in 2019 full-year significantly outperformed Hong Kong market, while the third and fourth quarter due to the stimulation of the China-US trade war news, Hong Kong market underperformed in the third quarter and outperformed the A shares in the fourth quarter. We believe that the above trend of differentiation occurs by multiple factors, including: 1) Hong Kong stocks are more vulnerable to external factors, while the A shares relative to the mainland environment as the leading factor; 2) China Securities Regulatory Commission broadened the trading range of equity financing, and up to 12 May 26, Shanghai and Shenzhen markets margin balance reached 1,015 billion CNY, the last time financial balances exceeded 1 trillion is at the end of 2014, making the A-share trading volume increased and supporting the performance of A-shares objectively; 3) international index companies improved the A-share index factor, the Chinese government canceled the QFII and RQFII investment restrictions, attracting foreign investment in A-share market; 4) due to the Chinese government favorable policies, the Shenzhen Composite Index return is higher than the Shanghai Composite Index; 5) affected by the local community in Hong Kong, visitors to Hong Kong dropped significantly, resulting in Hong Kong's local economy weak and sentiment also weakened, dragged down Hong Kong stocks.

For sectors, the Hang Seng business sector in 2019 return was 10.76%, the Hang Seng financial sector in 2019 return was 9.23%, Hang Seng property sector in 2019 return was 8.20%, the Hang Seng utilities sector in 2019 return was -2.09%.

Mainland Chinese Economic Data Review

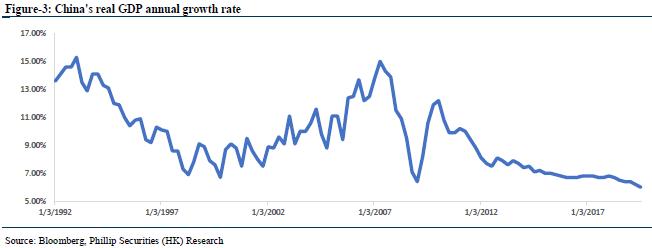

Quarterly GDP growth continues to slow

China's real GDP annual growth rate since 2010 continued to slow down, until the third quarter of 2019 reached the lowest growth rate of only 6%, worse than expected and hit a 27-year low. With downward pressure, slowing consumption, internal and external causes of China's GDP growth continued to slowdown. We believe that the future of China's economic growth will change over the past pursuit of high-speed development to high-quality steering stage, and continuing to slow GDP growth is expected, it is estimated that full-year 2019 GDP growth forecast of 6% ~ 6.2%, and 2020 is expected to slow further to 5.8% ~ 6%.

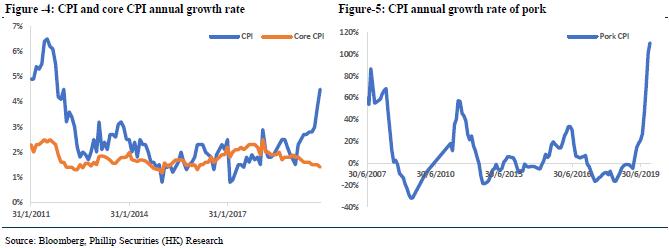

Inflation continues to heat up

Chinese consumer price index in July 2011 reached 6.50% of annual growth, the highest in nearly a decade. Afterwards it declined in January 2015 to 0.76%, subsequently experienced a rebound, and in recent years it remained at 0.76% -3% range, overall volatility is stable. Only the last three months due to the problem of African swine fever affected, pork prices rose sharply and in November 2019 CPI rose to 4.5% annual growth rate as the highest since January 2012, while the core CPI annual growth rate of the index drop to 1.4%; pork CPI annual growth rate of -3.2% by the beginning of the year increased significantly to 110.2% at the end of year. It should be noted that the core CPI, PPI and non-food CPI dropped down, displaying the current round of influence "pig cycle" is not conducted to the PPI, also reflecting the overall economic environment lack of demand, deflation intensified in industrial sectors.

Manufacturing PMI showed a good trend

Overall, domestic and international economic momentum is slowing, weakening domestic and external demand, manufacturers are also affected by the situation, PMI showed a poor overall performance compared to last year. However, China's manufacturing PMI rebounded in November 2019, the official manufacturing PMI rose to 50.2, which is the index first time went back to above 50 after six consecutive months below 50, to return to the expansion area, also hit eight-month high, and maintained in December. Later Caixin announced its manufacturing PMI, it rose to 50.4 in August 2019 and maintained above 50, until in November rose to 51.8, also above 51.4 of this month and last month's forecast of 51.7 in a Reuters, continuous 5-month rise and the highest since December 2016. PMI shows a good trend due to improved demand and stabilized production, Caixin new orders index also maintained a high level, the economic situation continued to repair.

Weakening Retail Sales of Consumer Goods Data

Continued weakening of the annual growth rate of China's retail sales of consumer goods data from June 2017 peak (annual growth rate of 11%), fell to 7.2% in October 2019, November rebounded to 8%, of which the automotive retail (annual growth rate -1.8%), building materials retail (-0.3% annual rate) to maintain negative growth in retail sales (annual growth rate of 7.8%), petroleum retail (annual growth rate of 0.5%) remained low by historical growth rate, dragged down retail sales performance.

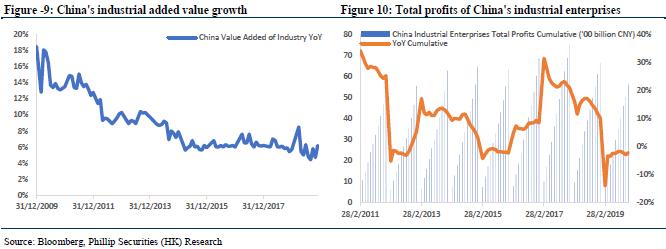

Slowing Trend of Industrial Production Growth

China's industrial added value growth rate bottomed out in August 2019 (4.4% annual rate), a 17-year low, after September rebounded to 5.8%, November data was 6.2%, accelerating 1.5 percentage points higher than October. From three categories, in November, the annual growth of value added in mining was 5.7%, compared with the growth rate 1.8 percentage points in October to speed up; manufacturing industry increased 6.3%, accelerating 1.7 percentage points; electricity, heat, gas and water production and supply grew 6.7%, accelerating 0.1 percentage points. Among 41 major industries, 38 sectors keep growing; among 605 kinds of products, 369 kinds of products grew more than expected.

In November, China's industrial enterprises above designated size achieved a total profit of 593.9 billion CNY, an annual increase of 5.4%, in October it was down 9.9%. From January to November, the national scale industrial enterprises realized a total profit of 5,610 billion CNY, down 2.1% on an annual decline narrowed by 0.8 percentage points over January to October. It was mainly due to the decline in industrial prices narrowed, production and sales growth rebounded and other factors.

PPI continued downward

In November 2019 China's industrial producer price index PPI annual decrease 1.4%, a decline narrowed 0.2 percentage points than in October, the second lowest in three years, deflationary pressures increase. Industrial producer purchasing price PPIRM fell 2.2% yoy, 0.1 percent points lower than in October. Chinese producer prices PPI and purchasing prices PPIRM overall showed a downward trend, but the difference between the two spin-down has increased 0.8% in November, 0.3 percentage points increasing compared with October, reflecting the profits of industrial enterprises, though it is still at the level of the poor, but showed signs of improvement.

Export Growth Continued To Fall, Imports Eased

China General Administration of Customs announced in US dollars, China November exports fell an annual 1.1%, worse than the market expected to grow by 0.8%; imports were up 0.3%, better than market expectations -1.4%. October imports fell 6.4%. Trade surplus of $38.73 billion in November, annual narrowing of 7.5%. The first 11 months, China's total imports and exports was $4.14 trillion, down 2.2%. Among this, exports were $2.26 trillion, down 0.3%; imports were US$ 1.88 trillion, down 4.5%; trade surplus of $377.6 billion, expanding 28.4%. By the global economic downturn and trade war affects, China's exports pressure increased, while domestic demand improved.

Fixed Asset Investment Grew Moderately

Since 2010, China's fixed asset investment growth dropped sharply, mainly due to severe overcapacity, coupled with the reform of state-owned enterprises, private investment willingness is insufficient, and it is relied more on government-led infrastructure and real estate investment. November 2019 China's fixed asset investment in cumulative annual growth rate was 5.2%, unchanged from last month, to maintain the minimum data records. From January to November, industrial investment grew 3.7%, accelerating 0.2 percentage points compared with January to October, investment in technological upgrading of industrial growth was 8.7%, 5.0 percent higher than industrial investment, which has become an important factor driving the growth of industrial investment . Oil and natural gas industry investment grew 31.6%, coal mining and washing industry investment grew 27.3%.

Hydropower investment grew 13.9%, wind power investment grew 33.9%, biomass power generation investment grew 50.3%. Road transport investment grew 8.8%, 0.7 and 0.3 percentage points higher than January to October and last year respectively. High-tech industry investment grew 14.1%, 8.9 percentage points higher than the total investment.

2019 January-November real estate investment grew by 10.2%, with the growth rate from January to October falling 0.1 percentage points, decline narrowed in stages. In the first 11 months of this year, the cumulative growth rate of real estate investment was stable at 10%, higher than the same period investment in fixed assets 5.2% growth, while the overall real estate development climate index was 101.16, 34 consecutive months of higher than 100, in state of an economy boom.

Commercial Housing Sales Enhanced on a Monthly Basis

In the first 11 months of 2019, the newly-started floor space of housing enterprises fell from a high level, and the growth rate continued to decline to a low point. The cumulative growth rate of newly-started floor space in the first 11 months dropped to 8.6%, mainly due to the continuous tightening of the financing environment. During the same period, the growth rate of land purchases has significantly narrowed. The area of land purchases in the first 11 months has decreased by 14.2% year-on-year, and the decrease rate has been narrowed by 2.1% from January to October. The heat of land transactions remains relatively low, and enterprises` willingness to acquire land has gradually increased.

In the first 11 months of 2019, the sales area of commercial buildings nationwide was 1.489 billion square meters, a year-on-year increase of 0.2%. Since the previous month, it has increased from a decline to an increase of 0.1 percentage point from the previous month. Among them, the sales area of residential buildings increased by 1.6%, the sales area of office buildings decreased by 11.9%, and the sales area of commercial buildings fell by 14.1%. In terms of value, the total sales of commercial housing in the first 11 months reached 13.9 trillion CNY, an increase of 7.3%, and the growth rate was flat. Among them, the sales of residential buildings increased by 10.7%, the sales of office buildings decreased by 11.3%, and the sales of commercial buildings fell by 13.5%.

Mainland China Economic Outlook

Mainland China economic growth forecast

The Organization for Economic Cooperation and Development (OECD) predicted in November that the global economic growth in 2019 and 2020 will be 2.9%, while the Mainland's economic growth will be 6.2% in 2019, 5.7% in 2020 and 5.5% in 2021. The Asian Development Bank released the Asian Development Outlook Update" on September 25. With the escalation of trade disputes with the United States, exports have decreased and investor confidence has been frustrated. China's economic growth in 2019 and 2020 will be somewhat faster than in 2018 Slow down. However, loose fiscal and monetary policies will help ease these pressures. ADB forecasts that China's GDP will increase by 6.2% and 6.0% in 2019 and 2020, respectively. The International Monetary Fund (IMF) released the "World Economic Outlook", which refers to increasing trade barriers, increasing geopolitical tensions and weakening economic growth. It is estimated that the trade tensions between the United States and China will lead to a cumulative decline in global GDP levels by 2020 0.8%. Among them, the latest IMF on October 15 cut China's 2019 economic growth forecast from 6.2% to 6.1%, and growth will slow down next year, forecasting from 6% to 5.8%, down 0.1 and 0.2 percentage points, respectively. Reuters reported on October 14 that a business survey conducted by it found that China's economic growth in 2019 is expected to decrease to 6.2%, which is the lowest growth rate in nearly 30 years, and it will be further reduced to 5.9% by 2020. We expect that given China and the United States claim that the signing of the first phase of the trade agreement and the continued recovery of the Chinese economy, China's economic growth in 2019 and 2020 will be 6.2% and 5.8%, respectively.

2020 A-Share Incremental Funding is Expected to Be More Than Trillion

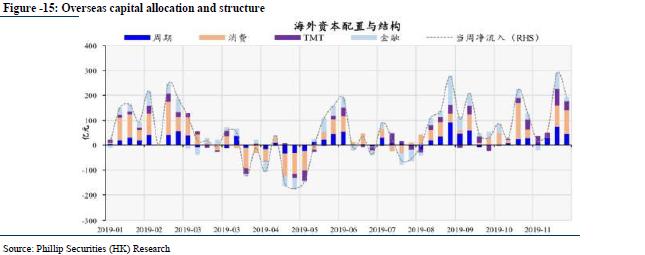

China has three major market incremental funding sources: overseas funds, bank financing subsidiaries and emerging public fund. Since mid-August 2019, the net inflow of foreign capital continued. So far, net inflows have more than 191.3 billion CNY, of which the consumer sector inflow of 71.2 billion CNY, 45.8 billion CNY inflow cycle sector, the financial sector inflow of 43.7 billion CNY, 30.3 billion CNY inflow in the TMT sector. And in accordance with the slope of the inflow of foreign capital, it is estimated that in 2020 the net inflow of foreign capital totaling about 250 billion to 350 billion CNY.

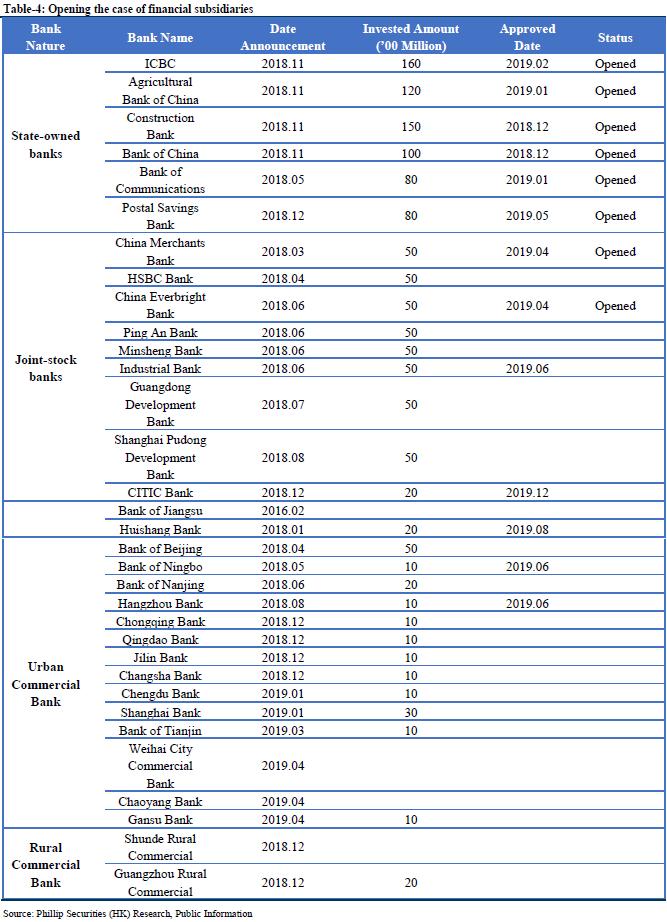

It has opened a total of 8 financial subsidiaries, 5 approved to build, and 20 to be set up, a total of 33. As of 2018, the bank non-insurance financial survival balance of 22.04 trillion CNY, of which equity investment accounted for 9.92%, corresponding to the scale reached 2.19 trillion CNY. As calculated in accordance with the annual growth rate of 3%, as of 2020, non-bank financial survival guaranteed balance is expected to reach 23.38 trillion CNY; according to 10% of the equity accounting estimates, the scale of investment equity market is expected to reach 2.34 trillion CNY, meaning 2020 bank financial subsidiaries corresponding incremental funding size of about 150 billion CNY.

In addition, from 2017 to December 2019, the average annual compound growth rate of newly established fund partial stocks is 18%. Based on this estimate, we estimate that the size of newly established fund partial stocks in 2020 is expected to reach 490 billion to 500 billion CNY. On the whole, the incremental funds for A-shares in 2020 are expected to exceed one trillion CNY.

China & Hong Kong Stock Market Investment Strategy In 2020

From the perspective of internal and external influences, we believe that the trend of the Chinese and Hong Kong stock markets in 2020 will be mainly affected by the following factors: 1) the progress of China-US trade negotiations; 2) the uncertainty of Brexit; 3) the prospect of the USD and the RMB; 4) China and US government's fiscal and monetary policies; 5) the risk of local political factors in Hong Kong and the implementation of government relief measures; 6) the geopolitical crisis in the Middle East; 7) economic risks caused by global political events.

From the perspective of asset classes, given the current relatively low interest rates globally, we recommend focusing on relatively robust asset classes. Because the 10-year US bond yield rate has fallen to a lower point, stocks with stable and high dividend payout ratios, strong domestic demand stocks, and investment-grade bonds have higher investment value. However, it should be noted that the market's risk aversion mood is heating up from time to time, and it is recommended to hold gold, JP yen and other relevant safe-haven assets or other reverse products for hedging.

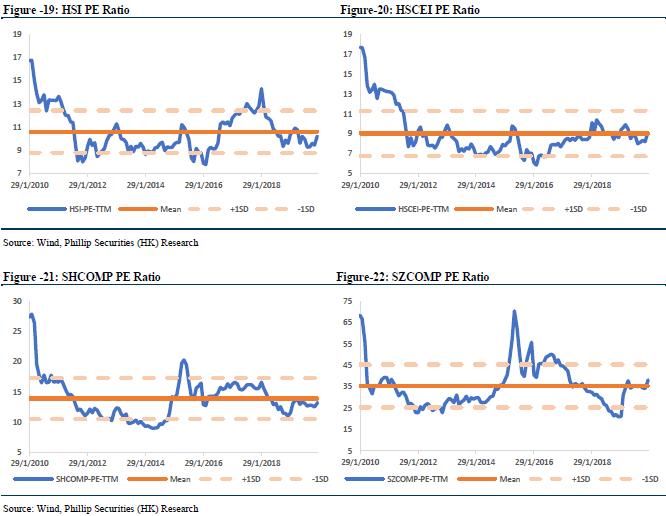

From the perspective of market selection, as China and the United States gradually reach the first stage of the trade agreement, China-US trade frictions can be cooled in the short term, which will help boost the short-term performance of Hong Kong and A-shares. The continued recovery of the Chinese economy, the "structural easing policy" of the People's Bank of China, the stabilization of the RMB exchange rate, and the continued inflow of foreign capital will all benefit the performance of the China and Hong Kong stock markets. However, it should be noted that the weakness of Hong Kong's consumption and economy has not yet eased, and will continue to have a negative impact on the Hong Kong stock market. From the historical price-earnings ratio, affected by the mean reversion, A shares and Hong Kong stocks are near the average value of the valuation, but considering that the data used is TTM P/E, we believe that valuation after the results is still attractive, long-term funds will increase the allocation of Chinese and Hong Kong stocks.

From the perspective of sector allocation, we recommend that we focus on the Guangdong-Hong Kong-Macao Greater Bay Area concept stocks that focus on regional development, China telecom stocks and semiconductor stocks driven by the rapid development of 5G technology, and consumer stocks that have benefited from mainland China's economic development and domestic demand stimulation. Blue-chips infrastructure stocks driven by economic stimulus policies and infrastructure investment, gaming tourism and auto stocks at low valuations, China's new economic stocks that are about to set off a return to Hong Kong, and insurance and pharmaceutical stocks that are more resistant to the economic cycle.

Bay Area Stocks

The "Guangdong-Hong Kong-Macao Greater Bay Area Development Planning Outline" has been officially released. The "Outline" outlines the roles of cities and emphasizes the connection and cooperation between major cities. Through the advantages of core cities, the Greater Bay Area will be positioned as finance and innovation center. We expect that as the connection strengthens, population growth accelerates, and residents` income rises, it will drive consumption and housing demand in the Greater Bay Area, and the real estate industry is expected to benefit.

At the same time, the Mainland economy is affected by factors such as the China-U.S. Trade war, and downward pressure is increasing. The Chinese government is stepping up its efforts to introduce more easing policies, including tax cuts. In the past years, it was simple, and the content did not mention "housing and living without speculation" and "to curb rising house prices." We believe that this means that the current regulatory thinking of urban governance will continue, and subsequent local policies have greater flexibility and adjustment space. The overall interior market is expected to be supported.

We suggest that you can pay attention to Times China (1233), which has 93% of the Greater Bay Area land reserve. The company's management has strong execution ability, and the land reserve is sufficient to 18.5 million square meters. It is expected that both profit and sales will remain high in the next 3 years. The growth is mainly due to the continued advancement of the city. The project will convert approximately 10.8 million square meters during the period, with a market value of approximately 200 billion CNY. CIMC Group (2039.HK) and Country Garden (2007.HK) also belong to the concept stocks of the Greater Bay Area.

5G Technology-Related Stocks

At the opening forum of the China International Information and Communication Exhibition in 2019, Chen Zhaoxiong, Deputy Minister of Industry and Information Technology, and the chairman of China Telecom, China Mobile, China Unicom, and China Tower jointly launched 5G commercialization, announcing that China is entering the 5G commercial era. The three major operators have announced the first batch of 5G commercial use in 50 cities. The 5G commercial package launched is divided into multiple stalls, which include traffic ranging from 30GB to 300GB. The starting price is about 128 CNY. November 1 officially launched.

From the perspective of the 5G packages released by the three major operators, the price difference is basically small; compared to the 4G era, the package price has increased significantly, and is significantly higher than the current average monthly ARPU value of 4G users. After 5G is officially put into commercial use, CAPEX will continue to grow. In 2020, operators are expected to realize the scale of 5G base stations with 600,000 to 800,000 stations, driving the performance of related companies in the industry chain. In addition, with the completion of SA network construction in 2020, the transmission network construction market is expected to open up room for growth. We are optimistic about the continued growth of related communications equipment and device companies. We recommend that you pay attention to: ZTE (763.HK) and O-Net Technology Group (877.HK). In addition, after the widespread launch of 5G mobile phones to reduce costs and reduce prices, domestic consumers will begin to update mobile phones on a large scale from 2020 to 2021, and the industrial chain will usher in historic opportunities. For related stocks, we recommend China Tower (788.HK), COMBA (2342.HK), Kingboard Laminates (1888.HK), BYD Electronics (285.HK), and China Communications Services (552.HK).

According to the website of the Ministry of Finance on May 22, the Ministry of Finance and the State Administration of Taxation formally announced the announcement of the corporate income tax policy for integrated circuit design and software industries: "Integrated IC design enterprises and software enterprises established in accordance with the law and qualified in December 2018 Calculate the preferential period from the profit-making year before 31 days. Corporate income tax enjoys the "two exemptions and three halves" policy (the first year to the second year of the company is exempt from corporate income tax, and the third to the fifth year is reduced by a statutory tax rate of 25% Half-taxed corporate income tax) until expiry. "

In fact, as early as the National Assembly on May 8th, preferential tax policies for integrated circuits and software companies have been proposed. Today, this policy has been finalized in less than a month, which shows that the country is attractive to attract Domestic and foreign investors are more determined to participate in and promote the localization of the integrated circuit and software industries.

In recent years, as the country continues to increase support, the integrated circuit industry has developed rapidly, but the problems and bottlenecks that restrict industry development remain prominent. In 2018, China's wafer imports were US $ 312 billion, exceeding US $ 200 billion for six consecutive years, and exports were US $ 84.6 billion, with a deficit of US $ 227.4 billion. The huge market and the urgent need for localization have also contributed to the golden development era of the industry.

The implementation of the "two exemptions, three halves and half" policy is undoubtedly a huge benefit for high-tech companies such as the chip, integrated circuit, and software industries. The domestically-made alternative strategy for integrated circuits and software has also been officially rolled out. We expect that it will be a long time in the future. It will be a golden period for the explosive growth of the industry. Coupled with the input of the National Integrated Circuit Industry Investment Fund, which has been set up since 2014, the state provides comprehensive guidance on related industries from the policy and asset level. We recommend focusing on chip design and manufacturing related companies, such as SMIC (0981.HK), Hua Hong Semiconductor (01347.HK), ASM Pacific (522.HK), NAURA TECHNOLOGY (002371.SZ), etc.

High-Quality Consumer Stocks

China's economic growth has slowed to 6% in the third quarter. We expect that government measures including tax cuts, easing monetary policy and some infrastructure spending will have effects, and a new round of counter-cyclical easing measures is expected. The economic growth rate will be able to reach the central target of 6% to 6.5%. Supporting domestic demand will still be the focus of the Chinese government. We recommend that we continue to focus on investment opportunities in high-quality domestic demand stocks, such as China Want Want (151.HK), Bosideng (3998.HK), and so on.

National policies support the development of the Chinese sports industry. Following Premier Li Keqiang 's decision at the executive meeting of the State Council to further promote sports fitness and sports consumption, the General Office of the State Council recently issued the ¡§Outline for the Construction of a Powerful Country in Sports¡¨ to propose a series of strategic tasks, 2035 The annual target is to become a pillar industry of the national economy, and the proportion of people who regularly participate in physical exercise reaches more than 45%. In 2050, it will become a sports power.

The "Outline" also proposes to accelerate the development of the sports industry and foster new economic development momentum, including creating a group of well-known sports companies with international competitiveness and independent sports brands with international influence, and supporting superior companies, advantageous brands and advantageous projects to "go global" ". At the same time, sports consumption should be expanded, mass sports activities should be extensively carried out, the stickiness of sports consumption should be enhanced, the supply of holiday sports events should be enriched, and the demand for sports consumption should be stimulated. Expand new consumer space such as sports fitness, sports viewing, sports training, sports tourism, and promote the development of fitness and leisure and competition performance industries. Among the many mainland sports goods listed in Hong Kong, we recommend Anta (2020.HK), Li Ning (2331.HK), Xtep (1368.HK), China Dongxiang (3818.HK) and Topsports (6110.HK).

Yangtze River Delta Integration Opportunities

The Central Committee of the Communist Party of China and the State Council issued the Outline of the Yangtze River Delta Regional Integration Development Plan on December 1. On November 5, 2018, Xi Jinping announced at the first China International Import Expo to support the development of the Yangtze River Delta regional integration and become a country. Strategy, focusing on implementing new development concepts, building a modern economic system, advancing deeper reforms at a higher starting point, and opening up to a higher level, opening up with the ¡§Belt and Road¡¨ initiative, the coordinated development of the Beijing-Tianjin-Hebei region, the development of the Yangtze River Economic Belt, the Guangdong-Hong Kong-Macao Bay The construction of the districts will complement each other and improve the layout of China's reform and opening up. The outline identified five strategic positionings for the development of regional integration in the Yangtze River Delta. They are strong and active growth poles for national development; high-quality development model areas in the country; leading areas for the basic realization of modernization; demonstration areas for regional integrated development; Highlands. The planning period is 2025, and the outlook is 2035.

The "Outline" states that it is necessary to promote the formation of a new pattern of coordinated regional development. Focusing on ten major fields such as electronic information and biomedicine, we will strengthen regional advantageous industry cooperation. Promote the upgrading and transfer of traditional industries such as heavy chemical industry and engineering machinery, light industry food, textiles and clothing in the central area to cities outside the central area and some coastal areas with the ability to undertake. Strengthen the development and application of new technologies such as big data, cloud computing, blockchain, Internet of Things, artificial intelligence, and satellite navigation. Make overall plans to promote cross-regional infrastructure construction. Join forces to build a world-class airport cluster and plan to build a new airport in Nantong, becoming an important part of the Shanghai International Aviation Hub. Jointly build a digital Yangtze River Delta and accelerate the development of the quantum communication industry. It is necessary to strengthen the joint protection and co-governance of the ecological environment and accelerate the convenient sharing of public services. We believe the above sectors will benefit from the overall development of the Yangtze River Delta region. It is recommended to focus on artificial intelligence, industrial Internet, Internet of Things, big data, integrated circuits, 5G and other fields. Individual stocks include Flat Glass (601865.SH), Jiahua Energy (600273.SH), and DCITS (000555.SZ).

Insurance Stocks With Resistance To Economic Cycles

The Shenzhen Banking and Insurance Regulatory Bureau recently issued the "Plan for Establishing the Qianhai Cross-Border Insurance Innovation Service Center (Draft for Comment)". . The Opinion Draft states that the products that can be purchased by Qianhai Cross-border Insurance Center are mainly divided into three categories: First, there are no types of insurance with cash value, such as cross-border auto insurance and accident insurance; Insurance, critical illness insurance, etc .; Third, it is in line with Hong Kong and Macao deductible tax policies, such as voluntary medical insurance and deferred annuities. In terms of implementation, it will be a two-step approach. The first step is to provide claims services for mainland residents` existing Hong Kong policies only. The second step is to comprehensively develop insurance agency consulting, sales and claims services, and truly realize the interconnection and interconnection of insurance products.

The Opinion Draft states that cross-border insurance innovation service centers are settled by qualified insurance intermediaries such as agents and brokers, who apply for staffing at counters, and provide cross-border insurance company customers with insurance intermediation services such as underwriting, claims, and consulting. And encourage business personnel with relevant qualifications in Hong Kong and Macao to join service center intermediary agencies. According to the Hong Kong Insurance Regulatory Bureau, as of June 30, 2019, there were a total of 2,395 registered insurance agents, 73,277 individual agents, and 25,525 principals and business representatives.

At the beginning of August 2019, the Central Committee of the Communist Party of China and the State Council issued the Opinions on Supporting Shenzhen to Build a Pioneering Demonstration Area with Socialism with Chinese Characteristics. It explicitly requested Shenzhen to promote the interconnection and mutual recognition of financial markets and financial products with Hong Kong and Macau. At the same time, providing convenient services for cross-border insurance customers, and gradually realizing the interconnection of insurance between Guangdong, Hong Kong and Macau are also one of the important contents of the "Development Plan for the Guangdong-Hong Kong-Macao Greater Bay Area Development Plan". We believe that the Hong Kong stock insurance sector will benefit. We recommend focusing on AIA (1299.HK), Prudential (2378.HK) and Manulife Financial-S (945.HK).

Risk Factors

Progress in China-US trade negotiations; China's economic growth risk; Hong Kong community events further deterioration; Exchange rate risk.

Click Here for PDF format...