|

HEC PHARM(1558)

Analysis¡G

YiChang HEC ChangJiang Pharmaceutical Co.(1558) announced that the total consideration for the acquisition of Target Assets from Sunshine Lake Pharma was being revised to RMB1,645,600,000 from RMB2,057,000,00, i.e. 80% of the valuation of the Target Assets. The Target Products have distinctive medical functions, currently enjoy a leading position in China's market and possess great market potential. The application of the Target Products align with the Company's current product pipeline; and when approved for marketing, the Target Products will realize synergies with the current product pipeline of the Company, and are expected to secure a market share rapidly and generate considerable sales revenues. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $41.00, Target Price: $45.00, Cut Loss Price: $39.00

|

ZIJIN MINING(2899)

Analysis¡G

Zijin Mining recently issued a public offering of US $ 8 billion to supplement the acquisition of a 100% stake in copper, zinc and gold resources company Nevsun (at a price of 9.36 billion). In the next three years, the company's mineral gold, zinc, copper, silver, and iron concentrates will reach 49-54 tons, 38-42 tons, 67-74 tons, 242-269 tons, and 299-332 tons, respectively, by 2022. The copper composite content reaches 21.9-26%. The company's active overseas presence will gradually usher in the harvest period and is expected to become a global resource leader.

Strategy¡G

Buy-in Price: $3.60, Target Price: $4.30, Cut Loss Price: $3.10

Yokohama Reito Co., Ltd. (2874)

Established in 1948. Carries out the chilled / frozen storage business involving seafood / agricultural and livestock products, etc., the food products retail business involving processing, retail, import and export, etc. and real estate leasing, etc. Owns a distribution centre in Yokohama and Osaka (Yumeshima), which is a proposed site for the IR.For FY2019/9 results announced on 14/11, net sales decreased by 18.5% to 139.979 billion yen compared to the previous period (93.3% compared to the plan) and operating income decreased by 1.1% to 4.774 billion yen (81.7% compared to the plan). Despite an increase in both sales and profit in their cold storage warehouse business due to operations proceeding smoothly in the distribution centre newly built last year, the decrease in both income and profit in seafood products in the food products retail business has affected.For its FY2020/9 plan, net sales is expected to decrease by 2.2% to 143 billion yen compared to the previous year and operating income to increase by 13.1% to 5.4 billion yen. While pork and beef imports are soaring from lower tariffs due to the TPP and EPA coming into effect, slow domestic consumption of livestock products have led to warehouses storing chilled / frozen import food products being filled to the brim across the country. In addition, concerns on the spread of the ASF infection in China is spurring an increase in imports, therefore, an increase in revenue from storage fees / stevedorage is predicted.Target Price : 1,100 yenBuy Price : 1,000 yenCut-Loss : 970 yen

|

|

|

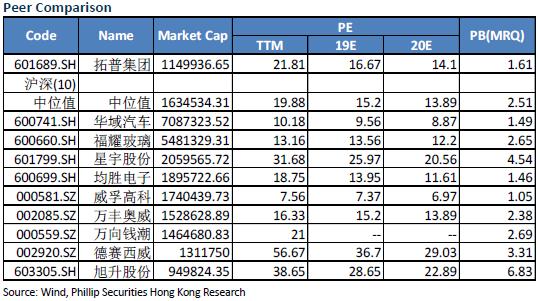

Tuopu Group (601689.CH) - Lightweight and Automotive Electronics Business See Opportunities

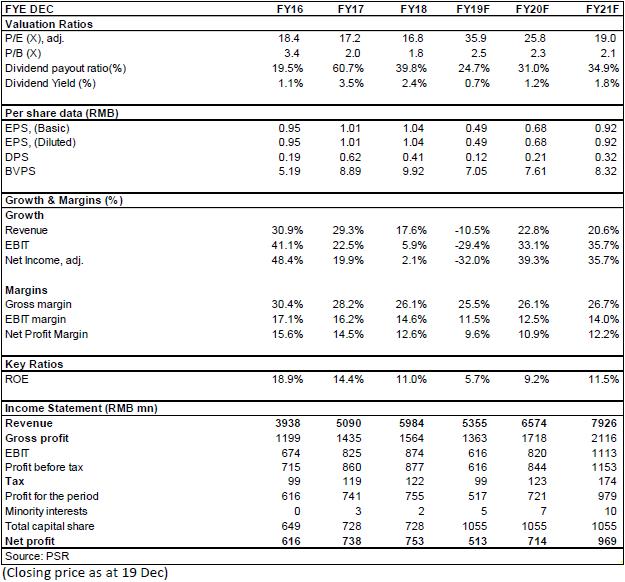

Investment SummaryDecline Slowed in the Third Quarter Tuopu Group recorded a revenue of RMB3766 million in the last three quarters, a 15.50% fall compared with the same period of last year. Among which, Q3 revenue was RMB1328 million, signaling a 3.90% Y-o-Y decrease and a M-o-M increase of 11.30%. Compared with the 25% decrease in the second quarter, the decrease has significantly shrunk. In terms of net profit attributable to the parent company, it was RMB340 million in the last three quarters, decreasing by 30% year-on-year. Among the RMB340 billion, RMB130 million was in the third quarter, which represented a 30% year-on-year decrease and a 30% month-on-month increase. Compared with the same period of last year, gross profit margin and net profit margin down 1.55 and 3.5 ppts, respectively, mainly attributed to the decline in industry prosperity and the increase in depreciation. Recovery of Sales Volume of Major Customers Leads to the Improvement of Capacity Utilization Ratio The improvement in results in the third quarter is resulted from the improved demand from downstream customers. The output of the company's major customers Geely Motor and SAIC GM increased by 9.3% and 3.8%, respectively in the third quarter over the previous quarter. The production of SAIC self and Chang`an Ford also improved compared with the previous quarter, leading to a rebound in the company's capacity utilization. Gross profit margin increased by 0.6 ppts to 26.4% compared with the second quarter, and net profit margin also increased by 1.4 ppts to 9.55% compared with the second quarter. We expect that with the further improvement in sales of major customers in the fourth quarter, the company's profitability will continue to pick up, and net profit growth is expected to be positive. The company continued to reduce costs and increase efficiency in adversity, and the sales, management and R&D expenses accounted for 14.76% of revenue in the third quarter, which fell by 0.92 ppts compared with the second quarter. The company has a good cash flow with a RMB226 million net flow from its operating activities. Inventories fell 12.9% year-on-year to RMB1.14 billion. Lightweight and Automotive Electronics Business See Opportunities for Development The construction of Tesla's Shanghai plant was faster than expected. The trial production began in October and nearly 20,000 vehicles will be produced by the end of the year. As capacity climbs, production will reach 150,000 in 2020 and is expected to exceed 250,000 in 2021. Tuopu supplies Tesla with more than RMB5,000 for each vehicle, and it is estimated that the Model 3 vehicles will bring the company a net profit increment of RMB93 million and RMB180 million in the next two years, respectively, accounting for about 12% and 24% of the company's net profit in 2018. In the field of automotive electronics EVP and IBS, the company's visionary layout brings it a leading position among domestic manufacturers. Tuopu is expected to break through the technological monopoly of foreign giants and realize domestic substitution in the future. Overall, the Company's lightweight chassis and automotive electronics business are in line with the trend of industry upgrading, which will inject momentum into the company's new round of development. Investment ThesisWe estimate that the company's net profit in 2019/2020/2021 will reach RMB513 /714/969 million, respectively, with the corresponding EPS being RMB0.49/0.68/0.92. Although the results in 2019 are under pressure, under the acceleration of Tesla's localization, the company's results will usher in an inflection point and we are optimistic about the development prospects of the company's lightweight business and automotive electronics. So, we lift the Company's target price to RMB19, respectively 26/21 x P/E for 2019/2020/2021, a "Accumulate" rating. (Closing price as at 19 Dec) RiskPrice war among peers Raw material price increase New business risk

Financials

Click Here for PDF format...

| Recommendation on 30-12-2019 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 17.440 | | Suggested purchase price | N/A | | Target Price | $ 19.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|