|

|

SUNAC(1918)

Analysis¡G

The latest announcement from Sunac China shows that the company`s performance has maintained a relatively high growth rate. In October 2019, the company achieved a contracted sales amount of approximately RMB64.43 billion , a year-on-year increase of 23.3%; the contracted sales area reached 4.389 million square meters, an increase of 22.2%. The average contracted sales price was 14,680 yuan / square meter, an increase of 0.9%. From January to October, the company achieved a total contracted sales amount of 433.92 billion yuan, a year-on-year increase of 16.9%; the cumulative contracted area reached 29,700 square meters, an increase of 22.5%. The company`s total inventory value is sufficient, and the quality is high. Nearly 80% of the inventory is located in the first- and second-tier cities. It is not difficult to complete the annual sales target of 550 billion. The company`s total land bank is already very sufficient, more than 200 million square meters, to meet the company`s continued development in the next 2-3 years. In the second half of the year, the company slowed down the pace of land acquisition and accelerated the sales to get cash. With the release of performance, the company`s financial situation will be improved, and the company`s net gearing ratio is expected to drop significantly by the end of the year. The tight financing environment of the real estate industry will improve as the land market getting cools, which will help the company continue to de-leverage.

Strategy¡G

Buy-in Price: $38.90, Target Price: $43.20, Cut Loss Price: $34.80

Chugai Pharmaceutical Co., Ltd (4519)

Founded in 1925 and established in 1943 as a company. Became a subsidiary of the Roche Group in Switzerland since 2002. Carries out research and development, and the manufacturing, sales and import/export of pharmaceuticals. Specializes in prescription drugs. A leading domestic company of biopharmaceuticals and antibody drugs, with top share in domestic sales of cancer and antibody drugs.For 3Q (Jan-Sept) results of FY2019/12 announced on 24/10, revenue increased by 19.3% to 508.851 billion yen compared to the same period the previous year, operating income increased by 64.3% to 160.878 billion yen, and net income increased by 61.7% to 114.588 billion yen. Product sales increased by double digits through contributions from new and main products and export growth. Revenue from royalties, etc., had also increased owing to contribution from Hemlibra.Company has revised its full year forecast upwards. Revenue is expected to increase by 17.3% to 680.0 billion yen compared to the previous year (original plan 592.5 billion yen), core operating income to increase by 67.3% to 218.0 billion yen (original plan 143.0 billion yen), and core EPS to increase by 71.2% to 302 yen (original plan 198 yen). As the annual dividend forecast has not been set, the core payout ratio, which was set at 48.5%, has yet to be finalized.Target Price : 9,500 yenBuy Price : 8,500 yenCut-Loss : 7,700 yen

|

|

|

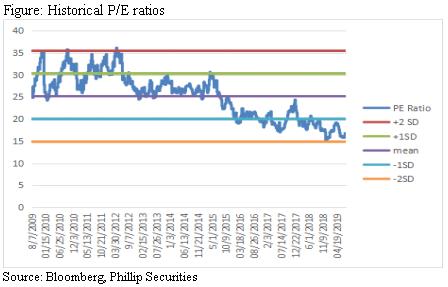

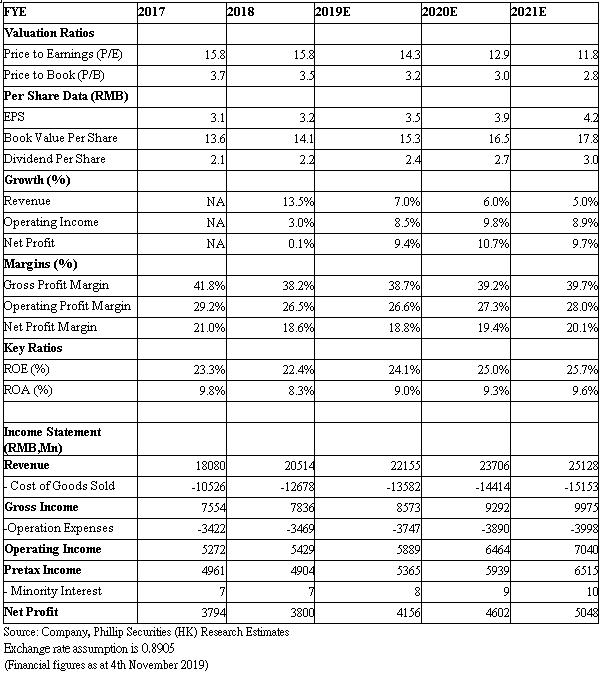

Hengan (1044.HK) - Sanitary napkin business is expected to improve in 2H, e-commerce and other businesses grow fast

Investment SummaryInvestment Highlights Its interim revenue of FY2019 increased by 6.3% y.o.y., mainly driven by tissue paper and the other businesses. The sanitary napkin business was down 4.6% due to the impact of traditional channel reform, which is in line with our expectations. Traditional channel accounted for over 60% of sanitary napkin revenue. During the period, the company increased its efforts to transform the traditional sales channels, encourage small sales team to sell products directly to retailers and provide upgraded and premium products. Although the reform has brought about an adjustment period to the sanitary napkin business, it is beneficial to business in the long run. At the same time, the business will be repositioned as feminine care product business, the new product line including cotton pads and makeup remover will be launched in the near future, and the mask will also be launched in 2H of this yea. During the period, GPM decreased by 2.3 ppt y.o.y. to 37.3%, mainly due to the increase in percentage share of other business, which is with lower GPM, by 3.7 ppt to 13.8%. Thanked to the fall in the price of wood pulp, GPM of the tissue paper business was only slightly reduced by 0.8 ppt y.o.y. to 25%. We expect that the price of wood pulp will continue to fall and be at a low level in 2H of the year, and Hengan will continue to optimize the product mix and increase the proportion of high-margin products, offsetting the negative impact of increased market competition and potential depreciation of the RMB. We expect that GPM of the tissue paper business will improve significantly in 2H of the year. During the period, brand promotion was intensified, resulting in an increase of the percentage share of distribution costs and administrative expenses by 1.6 ppt y.o.y. to 18.8%. The management team still maintains the guidance of mid-to-high single digit growth in revenue and tissue paper business this year. It also expects as the price of wood pulp falls, the price war of low-priced products such as roll paper will be more intense to seize market share in 2H. It plans not to directly reduce the product price, but will launch promotion activities. In 1H, sales of e-commerce platforms for paper towels and disposable diapers were strong, driving the former's revenue grew by 7.4%, and the latter's decline narrowed to 7.4%. E-commerce platform accounted for over 40% of the sales of disposable diapers, and sales of e-commerce channel increased by more than 10% y.o.y. The overall e-commerce business revenue increased by more than 50% y.o.y., and the contribution to overall revenue increased by 6.1 ppt. to 19.4%. We maintain Buy rating with a target P/E of 18x and a target price of 70.6. (current price as of November 4, 2019) Investment Thesis, Valuation & RiskWe maintain Buy rating with a target P/E of 18x and a target price of 70.6. The risks that need to be watched include top-line growth rate missing from expectation, wood pulp prices fluctuating sharply, industry competition increasing significantly, and Ameba units missing sales target. (current price as of 4th November, 2019)

Financials

Click Here for PDF format...

| Recommendation on 7-11-2019 | | Recommendation | Buy | | Price on Recommendation Date | $ 56.000 | | Suggested purchase price | N/A | | Target Price | $ 70.600 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|