Investment Summary

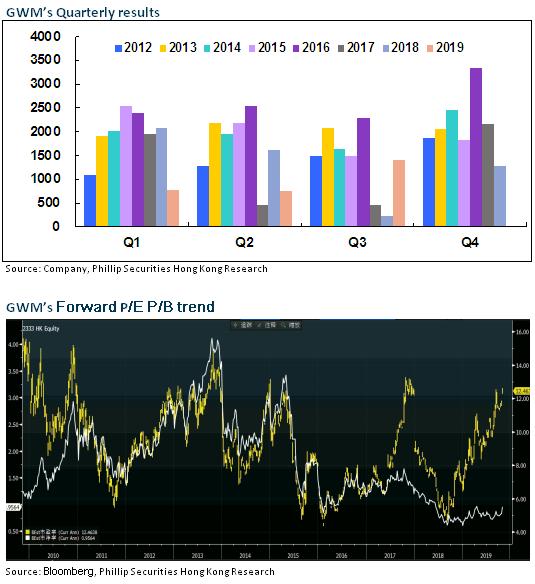

Q3 Profits Increased by near 90% QoQ Significantly

Great Wall Motors recorded the revenue of RMB21.2 billion in Q3, up 18% yoy and 13% qoq. The net profit attributable to stockholders reached RMB1.4 billion, up 507% yoy and 88% qoq. The accumulated revenue in the first three quarters reached RMB62.58 billion, down 6.1% yoy, a sharp decrease from -15% in the semi-annual report. The net profit attributable to stockholders reached RMB2,917 million, down 25.7% yoy, down 59% in the semi-annual report.

ASP Rebounded and Sales Volume Increase Pushed Profitability to Rebound Rapidly

Great Wall Motors was at the forefront of the industry in terms of ASP. Benefiting from the reduction of discounts after the switch of the China V/VI vehicle emission standards and the increase in the proportion of F-series with high selling prices, the average price of single vehicles of the Company in the first three quarters of 2019 was approximately RMB79,700, RMB89,400 and RMB91,900, respectively, showing a trend of increasing quarter by quarter. However, Great Wall Motors sharply reduced its inventory in the same period of last year, and the average price of single vehicles in the first three quarters of last year was RMB103,500, RMB102,000 and RMB87,600, respectively.

In terms of sales volume, the Company recorded sales volume of 230,000 vehicles in Q3, up 12.4% yoy, far better than the industry average decline of 5.5%, and the market share expanded by 0.61 ppts against the trend. In the first three quarters, a total of 724,000 vehicles were sold, up 7% yoy, reaching 68% of the annual objective of 1.07 million vehicles, with a good grasp of the annual objective.

The good performance of increase in sales volume and price pushed the gross margin in Q3 to rebound sharply to 18.49% from 13.65% in the same period last year, a sharp increase of 4.93 ppts qoq and 4.84 ppts yoy, compared with the gross margin of 13.72% in Q1 and 13.56% in Q2.

In terms of expenses: In Q3, the sales expense rate decreased by 1.25 ppts yoy and increased by 1.9 ppts qoq. Administration expense rate was basically the same yoy with a slight decrease of 0.2 ppts qoq. The R&D expense rate increased by 1.8 ppts yoy, which was basically the same qoq. The Company continued to promote the R&D investment in new products, new technologies and new platforms. The new platforms will simultaneously support fuel, PHEV and EV power modes. The hydrogen energy technology centre had also been built.

Good Momentum is Expected to Continue in Q4

Sales of passenger vehicle industry in China continued to improve in October. Considering the gradual dissipation of the overdraft effect of the switch to China VI vehicle emission standards and the low inventory, and combined with high season effect and low base factor, it is expected that the retail sales in the industry in Q4 will become positive yoy. As the leader of SUV industry, the overall performance of the Company was better than that of the industry, and the sales volume is expected to continue to increase in the future as the industry recovers. After the new platform is put into production in 2020, it will make up for the shortcomings of the Company's products in lightweight and provide a richer engine power allocation system. The two new SUV models built on this platform will be expected to come into market next year. A brand new electric vehicle will also be launched in terms of new energy brand Euler. The first hydrogen fuel cell vehicle is expected to be officially launched in 2022.

It is worth mentioning that the overseas business of the Company is gradually improving. In the first three quarters, exports increased by 41% to 50,000 vehicles yoy. The monthly sales volume of Russian factories had exceeded 1,000 vehicles. In the future, the Company will radiate to the Eastern European market and prepare for its entry into the international market again.

Investment Thesis

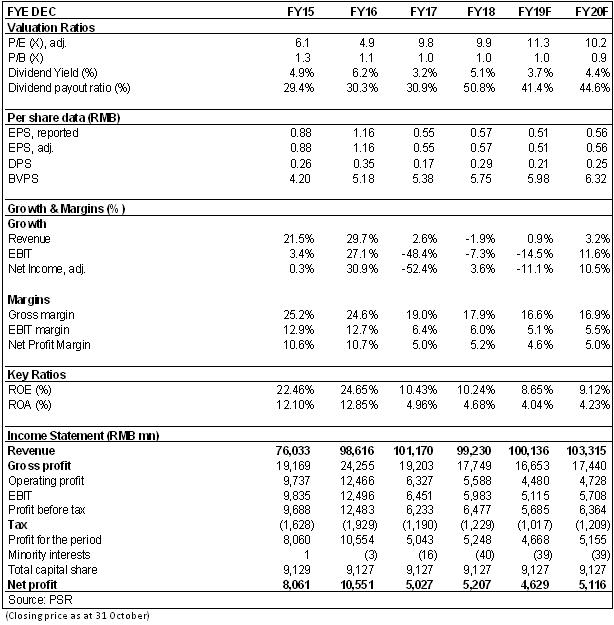

In terms of valuation, we adjust our target price to HK$6.5, equivalent to 11.5/10.4 P/E and 1.0/0.9 P/B ratio in 2019/2020. We give the rating of ¡§Hold¡¨. (Closing price as at 31 October)

Risk

New vehicle sales fall short of expectations

The SUV market dramatically worsens

The progress of new energy vehicle project is poorer than expectations

Financials

Click Here for PDF format...