|

SITC(1308)

Analysis¡G

SITC International Holdings (1308) is one of Asia`s leading shipping logistics companies that provides integrated transportation and logistics solutions. Its businesses include container shipping and logistics business, dry bulk and other business. The Group`s container shipping and logistics business focuses exclusively on the intra-Asia market as the Group believes that the intra-Asia trade market will continue to experience healthy growth. As of 30 June 2019, the Group operated 63 trade lanes that cover 66 major ports in the Mainland China, Japan, Korea, Taiwan, Hong Kong, Vietnam, Thailand, the Philippines, Cambodia, Indonesia, Singapore, Malaysia and Brunei. The Group`s fleet comprises 80 vessels with a total capacity of 112,583 TEU. With the Group`s continuous business expansion, the Group will continue to optimize its unique business model and expand its intra-Asia service network, striving to be the first choice of its customers. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $8.30, Target Price: $9.00, Cut Loss Price: $7.90

|

PUJIANG INTL(2060)

Analysis¡G

It is the largest provider of bridge cables for the construction of super-long-span bridges in China and the third largest prestressed materials manufacturer in China. Revenue of 2018 increased by 5% y.o.y. Interim revenue of FY2019 increased by 22.5% to RMB756million. The adjusted profit increased by 77.1% to RMB94.6 million which was mainly due to an increased in gross profit as a result of increased sales of bridge cables from cable business. During the period between 2013 and 2017, the CAGR of total fixed assets for transportation infrastructure in China was 9%, while the CAGR of investment in fixed assets for tunnel and bridge construction in China was 11.5%. It is expected to grow at CAGR of 5.5% and 10.4% respectively until 2022. It is expected that with the introduction of various new government policies in relation to infrastructure development, such as the 13th Five Year Plan and the Belt and Road Initiative, more bridges will be built and significant investment will be deployed in the transportation sector.

Strategy¡G

Buy-in Price: $4.27, Target Price: $5.00, Cut Loss Price: $3.80

Aeon Mall Co., Ltd (8905)

Established in 1911 as Gifu Kenshi. Became a member of JASCO Group in 1970. Core company responsible for Aeon Group's developer business, leasing stores in malls to various companies within the Aeon Group, and to Aeon Retail which is operating general tenants and general merchandise stores. Has 203 malls (175 malls within Japan, and 28 malls overseas).For 1H (Mar-Aug) results of FY2020/2 announced on 8/10, operating revenue increased by 4.2% to 161.07 billion yen compared to the same period the previous year, operating income increased by 18.3% to 29.212 billion yen, and net income increased by 9.0% to 17.043 billion yen. Operating revenue and various profits had exceeded company plans. In Japan, specialty store sales were firm. Overseas, China and ASEAN achieved operating profits.For its full year plan, operating revenue is expected to increase by 4.2% to 326.0 billion yen compared to the previous year, operating income to increase by 17.0% to 62.0 billion yen, and current income to increase by 0.5% to 33.7 billion yen. For its medium-term plan from 2017‐2019, company plans to open 26 stores. With the number of overseas stores expected to exceed that of domestic stores, company's shift of business overseas will be in full swing. Aims to achieve an annual average growth rate of 11.3% in operating income.Target Price : 1,810 yenBuy Price : 1,620 yenCut-Loss : 1,560 yen

|

|

|

SINOPHARM ACCORD (000028.SZ) - Results in line with expectations, revenue remains high growth

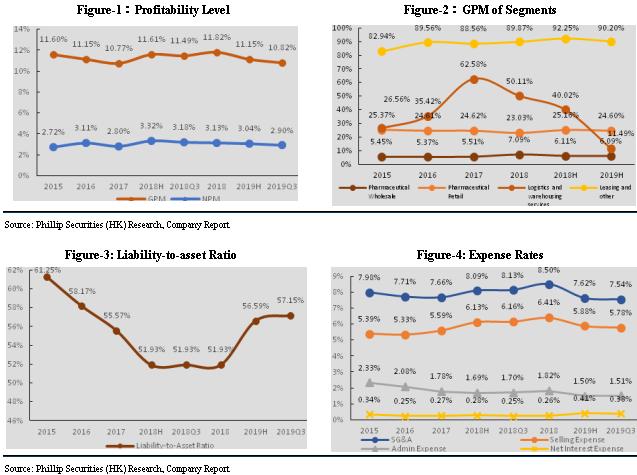

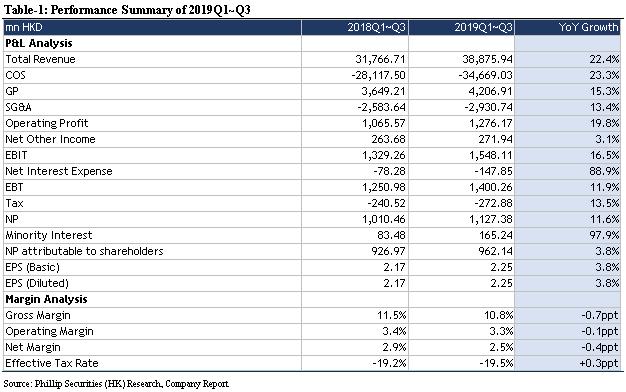

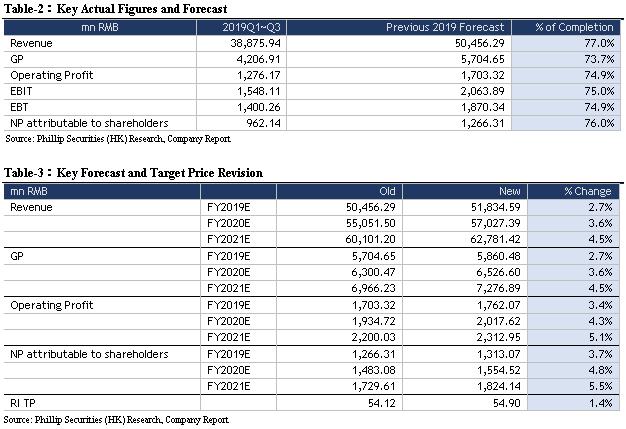

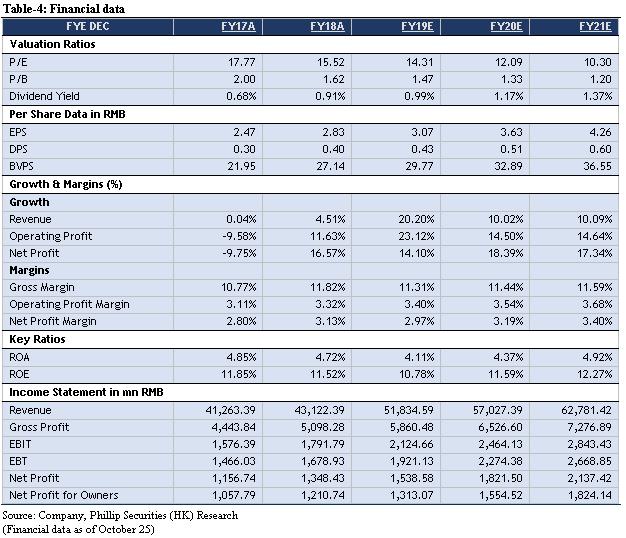

Company UpdateAs of 30 September 2019, the company's revenue was RMB 38.876 billion, representing an increase of 22.38% YoY; net profit attributable to shareholders was RMB 962 million, with a YoY increase of 3.79%; net profit attributable to shareholders excluding non-recurring profit and loss was RMB 943 million, with a YoY increase of 4.14%. In the third quarter, the income was RMB 13.648 billion, showing a YoY increase of 24.21%; net profit attributable to shareholders was RMB 311 million, showing a YoY increase of 9.14%; net profit attributable to shareholders excluding non-recurring profit and loss was RMB 303 million, showing a YoY increase of 7.45%. Business revenue growth continued to accelerate, the reason for which was that business income increased for the good business performance in the period. The profit growth rate is lower than the income growth rate, it is mainly because the company implements new leasing standards, the finance cost increased by RMB 69.57 million (a YoY increase of 88.87%); and the company's subsidiary Guoda Drugstore introduced strategic investors WBA in 2H2018, leading to a YoY increase in minority shareholders` equity of RMB 81.76 million (a YoY growth rate of 97.93%). The company's performance of core business is basically consistent with our forecast, and the revenue and net profit attributable to shareholders slightly exceeded our expectations. The company expanded the scale, and growth rate was better than the overall level of the industry, and related performance increase in total revenue was mainly contributed by the acceleration of the Wholesale and Retail Integration, better performance of distribution business and expansion of store network layout. Businesses sustained recovery, Wholesale and Retail Integration showed early resultsIn the first three quarters of 2019, the company's business continued to recover. The gross profit margin of sales was 10.82%, decreasing 0.67ppt YoY. We expect that this was mainly due to the adjustment of business income structure and the further enhancement of distribution business. With the gradual weakening of the influence of the introduction of strategic investors on minority shareholders` interests, the retail business continues to expand and the ¡§Guoda¡¨ brand upgrades to ¡§Guozhi¡¨ brand integration plan continues to advance, we expect the company will further increase profitability next year. In the first three quarters of 2019, the company's expense level was further reduced to 7.54%, decreasing 0.59ppt YoY; the selling expense rate was 5.78%, decreasing 0.38ppt YoY; the administration expense rate was 1.51%, decreasing 0.2ppt YoY; we expect it is mainly because the influence of the "two-invoice system" has gradually been reflected, and the company promotes "integration of wholesale and retail" to effectively control costs and reduce the period expense. The company's finance cost rate was 0.38%, showing an increase of 0.13ppt YoY. This was mainly due to the implementation of the new leasing standards, during the lease terms, interest expenses shall be calculated according to the discount rate forlease liabilities. The net interest expense increased by RMB 69.5683 million, the growth rate was 88.87%. In addition, the net cash flows from operating activities increased RMB 509 million on a YoY basis with growth rate of 90.24%. We expect it is mainly due to the increase in revenue, the improvement of operation efficiency and GPO policy, and also due to the implementation of new leasing standards in the period, the rents paid in the period are reckoned into cash paid with other financing activity concerned. In the first half of 2019, the distribution launched the logistics planning of wholesale and retail integration, the hospital direct selling market distributed in 30 cities at prefecture level and above in Guangdong and Guangxi ranked the top three; the distribution of customers was mainly including retail medical treatment, grass-root medical institutions, and small-scale social medical services: 1,804 medical institutions at the first level or above, 3,783 primary care customers (excluding 836 first-level hospitals), and 1,587 retail terminal customers (chain drugstores, single tores). In the pharmaceutical retail field, Guoda Drugstore is a pharmaceutical retail enterprise that ranks the first in the sales volume throughout the country, and is one of the few enterprises in China with national direct sales drug retail network. As of the end of June 2019, Guoda Drugstore had established 28 regional chain enterprises, had 4,593 stores, covering 19 provinces, autonomous regions, and municipalities directly under the central government, which formed a network of pharmacies covering the urban agglomerations of East China, North China, and coastal region of South China, and gradually spread into the Northwest, Central Plains, and inland city clusters; 3,470 direct-operated stores, 1,123 franchise stores. In addition, Guoda Drugstore built an Internet + medical e-commerce model, improved the value-added service system, optimized the self-operated OTO platforms such as WeChat Mall and APP, created a pharmacy + Internet O2O model, enhanced the front-end customer experience, and launched the e-commerce national customer service. In the first half of 2019, the number of effective members nationwide was 11.436 million, an increase of 8% YoY. Financial Forecast and ValuationWe adjust the company's revenue in FY19/FY20/FY21 to be RMB 51.8/57.0/62.8 billion, representing increases of 20.20%/10.02%/10.09% YoY; gross profit will be RMB 5.9/6.5/7.3 billion, representing increases of 14.95%/11.37%/11.50% YoY; net profit attributable to shareholders will be RMB 1.3/1.6/1.8 billion, representing increases of 8.45%/18.39%/17.34% YoY; corresponding EPSs are RMB 3.067/3.631/4.261. Based on our residual income valuation model, we adjust a TP of RMB 54.90, corresponding to FY19/FY20/FY21 17.90x/15.12x/12.89x PE with a +25.06% potential upside compared with CP of RMB 43.90 as of October 25, 2019, we upgrade from ¡§ACCUMULATE¡¨ to ¡§BUY¡¨ investment rating.

RiskIndustry policy risk; Guoda Drugstore's business fails expectations; Distribution business transformation fails expectations. Financials

Click Here for PDF format...

| Recommendation on 30-10-2019 | | Recommendation | BUY | | Price on Recommendation Date | $ 43.900 | | Suggested purchase price | N/A | | Target Price | $ 54.900 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|