|

HAOHAI BIOTEC(6826)

Analysis¡G

Shanghai Haohai Biological Technology Co. (6826) principally engaged in the manufacture and sale of biologicals, medical hyaluronate, ophthalmology products, research and development of biological engineering, pharmaceutical and ophthalmology products and the provision of related services. The Group will issue not more than 17.8 million A Shares at the issue price of RMB89.23 per A Share. The Board proposed that the proceeds from the A Share Offering, upon deduction of the offering expenses, will be invested in the International Medical Industrialization Project by Shanghai Haohai Biological Technology Co., Ltd. and used to replenish working capital. The implementation of International Medical Industrialization Project by Shanghai Haohai Biological Technology Co., Ltd., will strengthen the Company`s capability of researching, developing, upgrading and producing a variety of innovative medical products which cover the Group`s four major business segments and mainly include medical sodium hyaluronate, medical chitosan and recombinant human epidermal growth factor to meet the growing market demand. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $47.50, Target Price: $52.00, Cut Loss Price: $45.50

|

FUYAO GLASS(3606)

Analysis¡G

Fuyao Glass announced to acquire the German Company SAM for EUR58.85 million. The Company started to set about consolidation from March 1 and set foot in the automotive aluminum trim strip industry. After the integration, it is expected to achieve integrated supply of aluminum trim strips and automotive glass, improve the added value of products and expand the customer base. Looking ahead, as the North American business steps on the right track, the Russian business has bottomed out and recovered, and the domestic market share continues to increase, we are optimistic that the Company`s overall performance will maintain a stable growth in the future.

Strategy¡G

Buy-in Price: $22.00, Target Price: $24.60, Cut Loss Price: $19.00

Weathernews Inc (4825)

Established in 1986. Company collects data on various natural phenomena, including weather data, together with customers, and then processes the data and provides countermeasure content. Provides support to corporations in the area of weather forecasts, and also provides information for individuals.For 1Q (Jun-Aug) results of FY2020/5 announced on 7/10, net sales increased by 4.1% to 4.102 billion yen compared to the same period the previous year, and operating income decreased by 22.1% to 192 million yen. Corporate land-based weather information and personal mobile internet weather information had contributed to increase in sales. However, operating income had decreased due to increase in investments for growth, such as aggressive recruitment of human resources and increased investment in advertising.For its full year plan, net sales is expected to increase by 7.3% to 18.3 billion yen compared to the previous year, and operating income to increase by 2.7% to 2.1 billion yen. Following the United Nations Climate Change Summit held on 23/9, there is a growing sense of crisis regarding climate change. It is therefore expected that there will be a move to obligate disclosure of financial information related to this risk. Although the burden of investing in AIbased data technology will increase costs in the short term, the value of weather information collected and processed by the company is expected to increase in the future.Target Price : 3,440 yenBuy Price : 3,210 yenCut-Loss : 3,100 yen

|

|

|

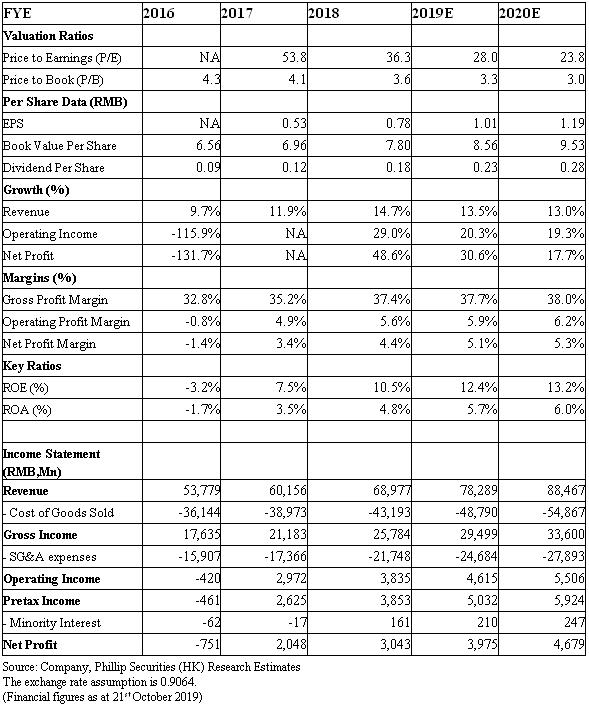

Mengniu (2319.HK) - Acquisition of Bellamy helping milk powder business development; maintaining whole financial year's guidelines

Investment SummaryMengniu announced that it intends to acquire Bellamy's Australia at a price of no more than AUD1.46 billion (HKD7.86 billion), with a planned share of AUD12.65 per share. Bellamy's net profit after tax is AUD21.7 million in FY2019. The P/E ratio is 67 times. Bellamy is Australia's first organic milk powder brand. It is listed on the ASX. It is a global recognised brand and has operations in Australia, New Zealand, China and Southeast Asia.We believe that the acquisition will be highly complementary to Mengniu's existing infant formula business, which will help Mengniu expand China and overseas markets. Organic IMF enjoys significantly faster growth and higher margins compared to the overall IMF market. Bellamy's gross profit margin of FY 2019 reached 43.5%, and the EBITDA rate reached 17.6%, both higher than Mengniu. Bellamy's FY 2018/2019 revenue fell 19% y.o.y. to AUD266 million, mainly due to the slower-than-expected approval of China's milk powder formula registration, and the e-commerce law. Mengniu said that after the acquisition, it will closely communicate with the relevant departments to assist Bellamy to accelerate the registration approval. Mengniu's revenue in 1H of FY2019 increased by 15.6% y.o.y., if excluding Junlebao, the growth rate was 13%. Up to 9.5% of revenue growth came from sales volume growth, and the rest was the increase in ASP, mainly due to faster growth of basic products. The management team still maintains the guidance of the whole year, with low double-digit growth in revenue (including Junlebao, which will be finished disposal in 2H. Operating profit margin improved by 50 points in 1H and is expected to be maintained in 2H. Gross profit margin decreased by 0.1 ppt y.o.y. to 39.1%, while GPM was flat excluding Junlebao. Raw milk price rose by 5 to 6%, higher than management team's expectation. But thanked for the product mix optimization, the high-end milk business is growing rapidly. The prices of other raw materials fell, and the tax rate has also had a positive impact, which led to an improvement in operating profit margins. After the announcement of the interim results, the stock price was under pressure. The market worried that the price of raw milk would remain high, and the market competition continued, which put pressure on operating profit. We believe the increase of raw milk price will help the performance of Modern Dairy (1117.hk) to resume. Mengniu's product mix will continue to be optimized, and it is expected that GPM can be maintained. After the completion of the disposal of Junlebao, profit margin can be improved. In 1H, the liquid milk business, which accounted for 83% of total revenue, increased by 14.4% y.o.y., the milk powder business increased by 43.8%, and ice cream decreased by 2.4%. For the liquid milk business, the market share of UHT products and chilled yogurt increased compared with the same period of last year. The former increased by 0.5 ppt to 28.5%, and continued to rank the second in the market. The latter increased by 1.3 ppt to 34.5%, and continued to be the market leader. For the e-commerce liquid milk category, the market share increased by 0.9 ppt to 24.6%, which also ranked the first in the market. During the period, the income of Milk Deluxe and Just Yoghurt which belong to the room temperature product business increased by 20% and 24% respectively, and Fruit Milk Drink also recorded double-digit growth, while the basic white milk business increased by 19%. During the period, Milk Deluxe had been launched fully revamped packaging, Just Yoghurt had been launched new flavor products, Fruit Milk Drink had been launched high-end products. The chilled product business has also introduced new packaging and a variety of new products. We give a forecast PE of 31 times and target price of HKD34.6. (current price as of 21st October, 2019) Valuation and riskWe are optimistic about the industry and the company's prospects, thus give forecast PE ratio of 31 times and target price of HKD34.6. Potential risks include failure to meet revenue growth, lower profit margins than expected, and huge fluctuations in raw milk prices. (current price as of 21st October 2019)

Financials

Click Here for PDF format...

| Recommendation on 25-10-2019 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 31.200 | | Suggested purchase price | N/A | | Target Price | $ 34.600 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|