Investment Summary

Minth's 2019H result lower than forecast, but the increasing trend of the oversea business is still to continued. In the near future, Minth's production structure are expected to continue improving, triggered by increased investment on technology upgrades and product optimization We maintain the opinion that Minth's existing businesses indicate a robust growth momentum, while great potential boom lies before the new ones, on the base of more input on R&D etc. We gave target price of HK$ 32 and Accumulate rating. (Closing price as at 17 October)

Revenue Increased by 2.3% in H1 and Net Profit Decreased by 10%

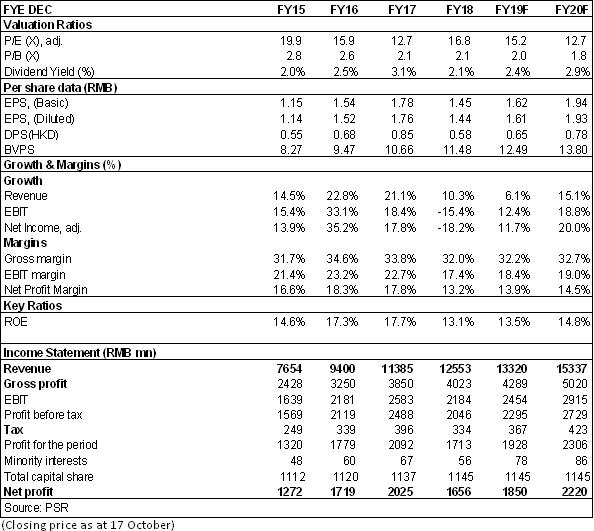

In H1 2019, MINTH GROUP recorded a turnover of RMB6.13 billion, up 2.3% yoy, mainly due to the decline of business in China adversely affected by the industry environment, while business in Europe and North America maintained growth. The net profit was RMB670 million, down 10% yoy, up 32% from H2 of last year; and the EPS was RMB0.78.

Minimize the Negative Impact of China-US Trade War

Affected by the China-US trade war, the upstream vehicle industry is facing a grim situation, with tariffs increasing, and the profitability of the Company's domestic products and exports of US products from Mainland China is under pressure. However, the Company was able to keep the adverse effects to a minimum by optimizing the global layout and adopting quick response and positive countermeasures. For example, some export products were transferred to local production to improve the capacity and production efficiency of US/Thailand/Mexico factories, resulting in an improvement in gross margin and net profit margin in H1.

The overall gross margin in H1 was 32.4%, down by 1 ppts yoy and up by 1.6 ppts hoh. This was mainly due to the performance of factories in the United States, Mexico and Thailand. The gross margin in North America and the Asia-Pacific region improved significantly from the same period of last year, partially offsetting the decline in gross margin caused by the decline in domestic capacity utilization rate. The revenue in Europe and North America increased by 35.8% and 12.7% yoy, respectively, accounting for 18.2% and 22% of the total revenue, up by 4.5 and 2.1 ppts, respectively. The revenue from Mainland China decreased by 7.7% yoy, accounting for 61.5% of the total revenue, up by 6 ppts.

Cost Rate Increased Slightly Due to Certain Inertia and Capital Expenditure Decreased

Due to business adjustment, increased expenditure on overseas transfer warehouse, increased cost of overseas talent introduction and increased share option fees, the Company's sales cost rate and management fee rate in H1 2019 were 4.2% and 7.5%, respectively, up by 0.3 and 0.5 ppts, respectively. In order to maintain market competitiveness and sustainable development, the Company's expenditure on talent introduction and new project investment increased, and the R&D cost rate increased by 0.6 ppts to 4.9%. Capital expenditure decreased to RMB746 million from RMB1.12 billion in the same period of last year, mainly due to the reduction in traditional line investment of heavy assets.

New Businesses began shoot and scores

The Company has made an earlier layout in the strategic business fields supporting long-term development. Apart from the traditional decorative strips/decorative pieces/body structure pieces/framework/luggage rack, the Company has made every effort to promote new products, new materials and new technologies in the Client during the period. It has continuously promoted the market development of new products such as aluminum door frames, battery boxes, adaptive cruise system signs (ACC signs) and active air intake grilles, and has obtained multiple orders. The Company has fully passed the Japanese-series ACC certification, and has obtained new orders for battery boxes of 15 European-series, Japanese-series and China-series new energy vehicles.

With the completion of several production bases in China approaching, the first aluminum battery box will be mass produced. In addition, the Company has successively started the construction of aluminum production lines in Serbia, Britain and the United States to meet the demand of customers around the world for nearby supplies and further strengthen and improve the Company's competitiveness in global layout. We believe that the average price of single vehicles for emerging businesses is much higher than that for traditional businesses (4000 Vs 400), and the new energy vehicle market facing is also different from the stock market of traditional vehicles. Early layout of emerging strategic businesses is conducive to pushing the Company's performance back to a healthy track of increasing volume and price.

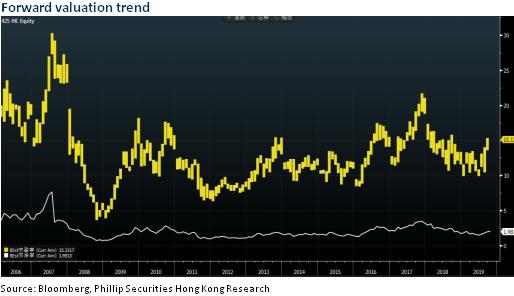

Valuation

The Company has a solid financial condition, with near 4.4 billion cash in hand. Besides, its operating net cash flow has increased to 1.22 billion. It is believed that the high dividend payout ratio will maintain. We believe that it is reasonable to give the company a valuation of 17.8/14.8x P/E in 2019/2020, equivalent to target price of HK$ 32 and Accumulate rating. (Closing price as at 17 October)

Financials

Click Here for PDF format...