Investment Summary

Xtep is placed as a brand management company with a clear brand image focusing on professional running that distinguishes it from the industry. Transforming from a fashion sportswear company to a Chinese runners` favorite brand, Xtep continued to rank first among all domestic brands and fourth among all global sports brands in international class marathons held in Beijing, Shanghai, Guangzhou and Xiamen, with the market share ranging from 10% to 20% in 2018. The plan, named "Outline for Building a Leading Sports Nation", was released recently by the State Council, aimed at helping accelerate China's overall sports development. According to the outline, by 2035, 45 percent of the population is expected to get involved in medium intensity exercise three times a week, up from 33.9 percent in 2018. The country is also developing a robust sports industry bolstered by sports-related consumption, production of sports goods and sports leisure and tourism into a strong pillar of economic growth by 2050, according to the plan. According to Frost & Sullivan, China became the world's second largest sports footwear and apparel retail market after the U.S. in terms of total retail sales value in 2018, and it is also among the fastest growing major markets in the world. The total retail sales value of China's sports footwear and apparel retail market increased at a CAGR of 12.8% from 2014 to 2018, and is expected to grow at a CAGR of 10.2% until 2023.

Xtep's interim revenue increased by23%,mainly driven by sales volume, ASP increased by 3% to 5%. It is expected that with the upgrading of products, ASP will grow by 3 to 5% every year in the future. From July to August, retail sales growth followed the trend of the 1H. It slowed down slightly in September. The management team believe that it was due to the warm weather. As the weather turns cooler, sales will pick up. It still maintains the annual core brand revenue growth target of 20%, next year is a double digit. After the announcement of the interim results, Xtep's share price dropped, mainly due to the RMB100 million expenses incurred by the K-Swiss and Palladium acquisition projects, which will be reflected in 2H. In fact, RMB40 million is for the relevant administrative, legal and auditing costs involved in the acquisition, and the rest is the one-off expenses for the employee's contingency expenses and inventory impairment which will be involved in the termination of the loss business.

Although Xtep's multi-brand strategy will increase the operating expenses in the short term, it will put pressure on the profit margin. However, in the long run, sources of income can be diversified. Xtep currently focuses on the second- and third-tier cities or below. The new brands business can help the company to open up high-end first-tier market. The new brand K-Swiss business still record a loss. It is expected to take 18 to 24 months to consolidate and will be re-launched to the market in 202. Most of this business is wholesale business, and Xtep will increase apparel business` percentage share to the total revenue, and improve product quality. Palladium has distributors and stores in China and the company plans to continue this model.

For Saucony and Memell, which are operated through joint venture, will expand network through distributors after two to three years. Merrell will have new stores being opened in the second half of next year, and Saucony in the second quarter of 2020. The two brands will retain 30% of their original design products. 70% will be the products that are redesigned for the China market. We give accumulate rating, target price-earnings ratio 18 times, target price HKD5.15. (current price as of October 9, 2019)

Business Overview

About the company

The company was founded in 2002 and listed on the Hong Kong Stock Exchange in 2008. The company completed a three-year strategic transformation in 2018, with revenue increasing by 24.8% y.o.y.in 2018. The same-store sales of its retail network also recorded 1 double-digit growth during the year.

Its multi-brand strategy started with the joint venture with Wolverine, which owns multiple outdoor, sportswear and casual wear brands, to develop, market and distribute Merrell and Saucony's apparel and accessories in China, Hong Kong and Macau.

It entered into the stock purchase agreement to acquire E-Land Footwear USA, for a cash consideration of US$260,000,000. is principally engaged in the design, development and marketing of footwear, apparel and accessories for athletic, high performance sports, adventures for all terrains and fitness activities and casual wear under three internationally recognised brands, including K-Swiss, Palladium and Supra as well as two sub-brands, namely PLDM and KR3W. Its revenue of 2018 recorded US$210,000,000, K-Swiss and Palladium were the two main income sources. Adjusted EBITDA turned into a profit of US$1,668,000. Net losses after taxation was narrowed to US$14,850,000.

The company believes that the transaction is an attractive opportunity to invest in a portfolio of global renowned sportswear and lifestyle brands targeting the high-end market segment. K-Swiss and Palladium, each with distinct brand positioning and different target customers, are highly complementary to the company's current brand portfolio and will enable the company to transform into a global sportswear player serving diverse customer needs.

Interim results of FY2019

Its interim revenue increased by 23% to RMB3.36 billion. GPM increased by 0.9ppt to 44.6%, which was mainly contributed by the sale of higher-ASP functional apparel products. The company also maintain effective cost control throughout the supply chain by utilizing both in-house and outsourced production, such that the increase in material costs and manufacturing costs was full absorbed by the increase in ASP.

For the period, the percentage share of selling and distribution expenses to revenue increased by 1.4ppt to 19%, which was mainly due to the increase in advertising and promotional costs. The percentage share of general and administration expenses decreased and thus the overall SG&A expenses stands at 27.3%. Net profit increased by 23.4% y.o.y. to RMB463million, with a interim dividend of HK12.5 cents. The interim dividend payout ratio for the period is 59.3%.

Same-store sales in the second quarter recorded low double-digit growth, while retail sell-through growth, including online and offline channels, increased by more than 20% y.o.y, retail discounts ranged from 20% to 25%, and inventory turnover days were approximately four months. The business performance was similar to that of the first quarter. The first quarter was affected by the promotion during the Lunar New Year period. The discount level was as low as 25%.

Investment Thesis & Valuation

We give accumulate rating, target price-earnings ratio 18 times, target price HKD5.15. Potential investment risks include new brand performance missing expectations, and industry competition intensifying. (current price as of October 9, 2019)

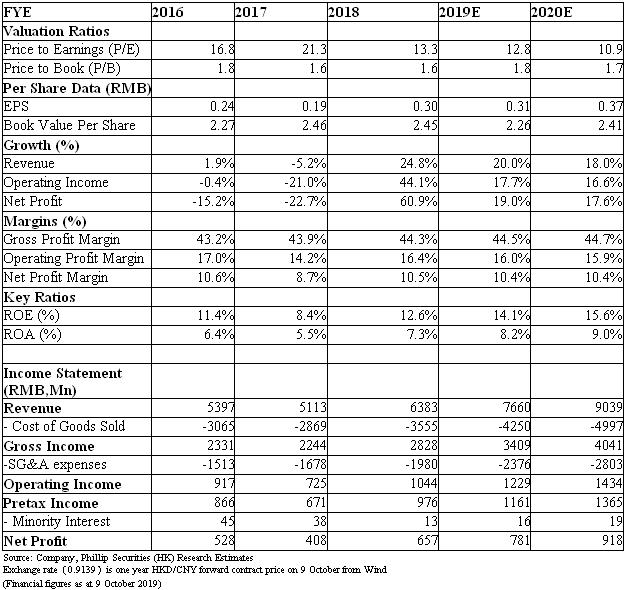

�Financials

Click Here for PDF format...