- Soar of 60% in Earnings of H1 2017

- Growth in Q2 Decreased

- Both Independent & Joint Venture Continually Pushed the Company's profitability

Investment Thesis and Valuation

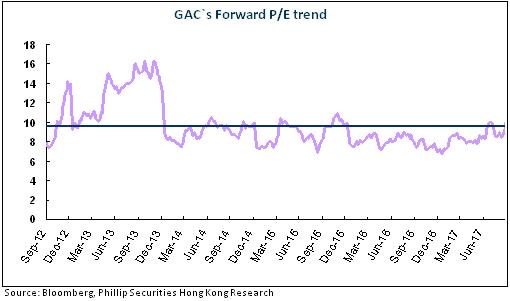

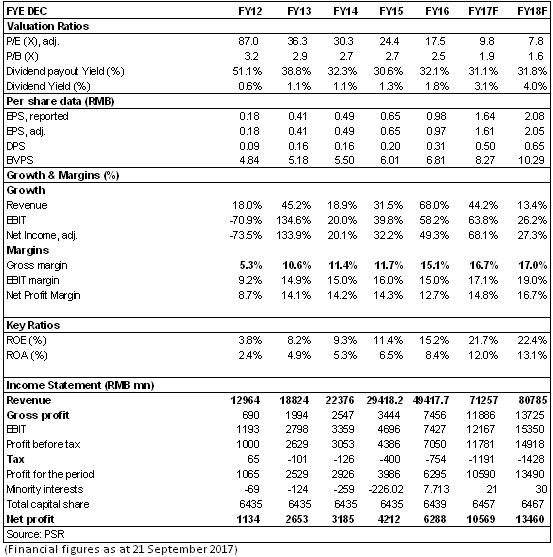

We believe that the excellent sales result has set the tone of high-growth result for GAC in this year, and so we adjust the estimate of the company's EPS to RMB 1.64/2.08 in 2017/2018, and target price to HKD 24.65, equivalent to 12.7/10x P/E ratio in2017/2018, and the "Buy" rating. (Closing price as at 21 Sep 2017)

Soar of 60% in Earnings of H1 2017

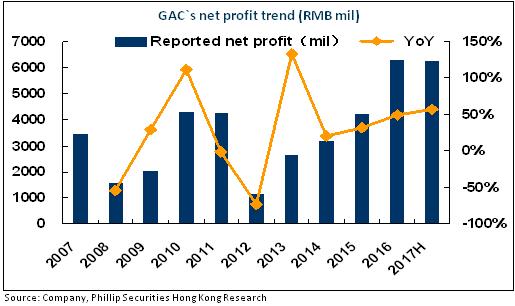

According to the report of H1 2017, GAC's general income in H1 was RMB34.765 billion, with a yoy increase of 62.2%; the net profit attributable to shareholders amounted to RMB6.27 billion, with a yoy increase of 57%; the EPS was RMB0.97, compared with RMB0.62 in the same period last year; the interim dividend payout was RMB0.10 per share, compared with RMB0.08 last year, with the dividend payout ratio decreasing 3 ppts to 10%.

Growth in Q2 Decreased

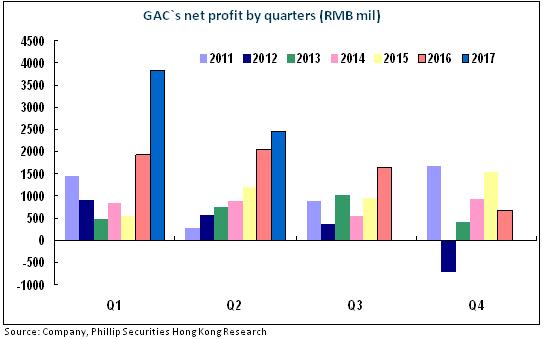

In accordance with the Generally Accepted Accounting Principles (GAAP) in China, the net profit in Q2 was RMB2.437 billion, up 18.5% yoy compared to a doubling of Q1, down 36% qoq compared with the net profit of RMB3.83 billion in Q1. Except for a high base, there are two main reasons:

1) In the second quarter, the growth of the domestic auto market slowed down. Under the pressure from price-off promotions of rivals, the Company actively took actions, enhancing advertising and promotions of its blockbuster brand Trumpchi and increasing promotion cost, recording the cost of sales of Q2 of RMB1.114billion, surging 39% yoy, up 24% qoq.

2) In the second quarter, the Company set aside RMB930 million for asset impairment on the basis of prudence, compared to only RMB230 million in the same period last year.

Independent & Joint Venture Continually Pushed Sales to Increase by 30% in H1

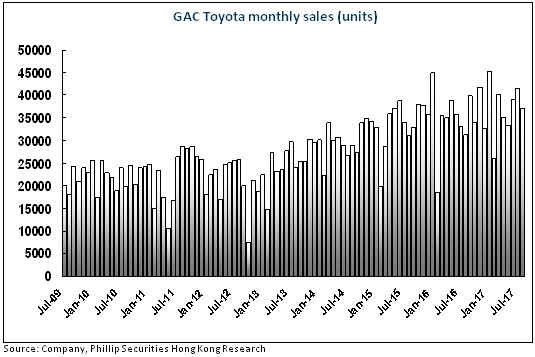

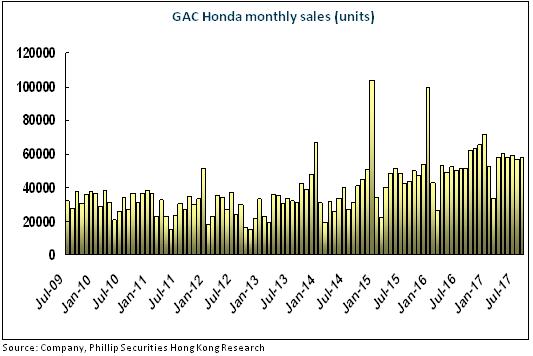

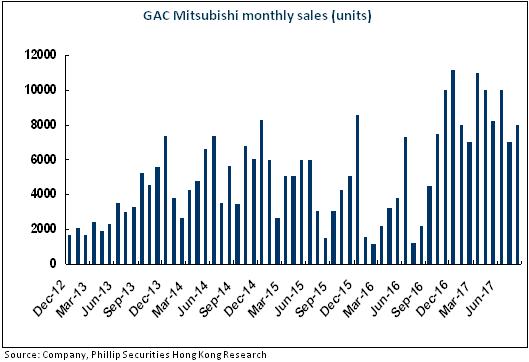

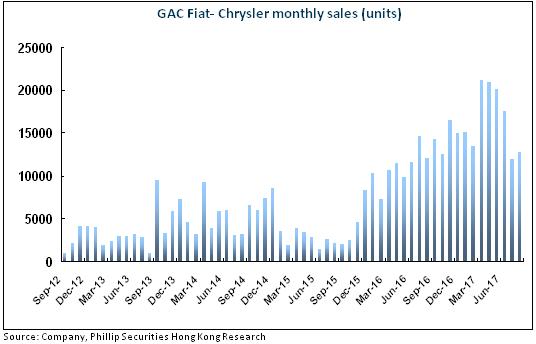

The Company sold 964,000 vehicles in H1, up 31.7% yoy. Among other things, the five major increment contributors were GAC's self-owned brand (+91586), GAC Honda (+47297), GAC Fait (+47229), GAC Mitsubishi (+34969), GAC Toyota (+10704), by increment contribution, respectively, among which, GAC Mitsubishi rose by 182% yoy, GAC Fait 77% yoy, GAC's self-developed brands 57% yoy, GAC Honda 17% yoy, and 5% yoy GAC Toyota.

GAC's self-owned brand sold 251,000 vehicles, up 57% yoy. Trumpchi achieved an excellent result, relying on the hot sales of GS4/GS8 in SUV market of the self-owned brand, with a monthly sales volume of GS4 of over 30,000 vehicles on average. In the joint venture brands, the sales of GAC Honda and GAC Toyota increased by 17.3% and 5.1% yoy, respectively; GAC Mitsubishi increased by 182% yoy, relying on the hot sales of Outlander; GAC Fiat increased by 77.21% yoy, with the new models Compass and Jeep Renegade contributing to the sales volume. In the second half, the new models of the Company include the small-sized SUVSG3, MPVGM8, and the mid-sized SUVGS7, continuing to expand the existing SUV layout. GAC Toyota will launch a new generation of Camry. Honda Advancier and Toyota Highlander are in short supply. We expect that under the protection of a variety of strong models, the Company's profitability still has a large upwards elastic space.

Investment Thesis and Valuation

We believe that the excellent sales result has set the tone of high-growth result for GAC in this year, and so we adjust the estimate of the company's EPS to RMB 1.64/2.08 in 2017/2018, and target price to HKD 24.65, equivalent to 12.7/10x P/E ratio in2017/2018, and the "Buy" rating.

Financials

Click Here for PDF format...