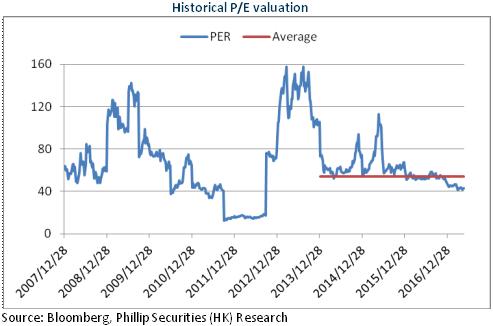

Investment Summary

Tonghua Dongbao is a domestic leading company of second-generation insulin, and its diabetes products reserves are rich. With the second generation of insulin shifting from Class B to Class A in the NDRL, plus the company's strong grassroots promotion channels, we expect it will continue to grow rapidly. The launch of third-generation insulin is expected soon, which will also inject new impetus to the growth. In addition, the company relies on chronic disease management platform, and establishes diabetes closed-loop system to consolidate its leading position. We give an estimation of 35x EPS in 2018 and the target price is RMB27.08, with the "Buy" rating initially. (Closing price as at 22 May 2017)

Results Continue to Grow Rapidly

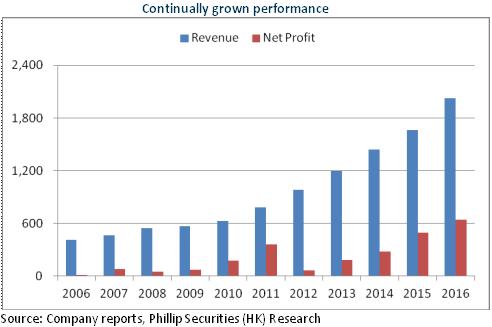

In 2016, Tonghua Dongbao recorded a revenue of RMB2.04 billion and the net profit attributable to parent company after deduction of non-recurring profit or loss stood at RMB620 million, respectively, up by 22.2% and 34.9% year-on-year. In the first quarter of 2017, the company continued to grow rapidly, with its revenue of RMB570 million, up by 25.3% year-on-year, and the net profit attributable to parent company after deduction of non-recurring profit or loss stood at RMB210 million, up by 31.2% year-on-year, basically in line with expectations.

For insulin business, the company continued to deepen the grassroots market and increase sales efforts. In 2016 its annual income reached RMB1.6 billion, up by 16.4% year-on-year, in which sales of 30/70 mixed recombinant human insulin injection rose to 1.2 billion, up by 14.6% year-on-year, sales growth of 50/50 mixed recombinant human insulin injection, recombinant human insulin injection and protamine recombinant human insulin injection stood up to 25-30%, sales of protamine recombinant human insulin injection soared 133.2% year-on-year. In addition, the medical equipment revenue in 2016 increased by 55.3% year-on-year, mainly due to the company's obtaining the franchise rights of Bionime's blood glucose test strips and other medical equipment, so that all specifications of Reiter blood sugar glucose test strips achieved a single income over 100 million, up by 200% year-on-year.

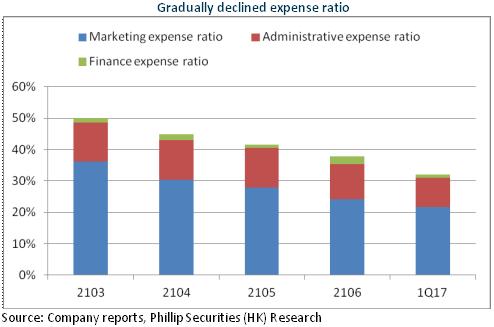

At the same time, the company's cost control was good. Since 2014 the expense ratio has decreased yearly 3-5pcts continuously, and that of 2016 was down by nearly 4pcts year-on-year, which is one of the main factors that the company's profit growth was faster than revenue growth. In the first quarter of 2017, the expense ratio continued to decrease by 4.6pcts year-on-year, of which marketing expense ratio decreased by 2.2pcts to 21.7%, administrative expense ratio decreased by 0.4pcts to 9.4%, and financial expense ratio decreased by 2pcts to 0.9%.

NDRL adjustment will support insulin products to grow rapidly

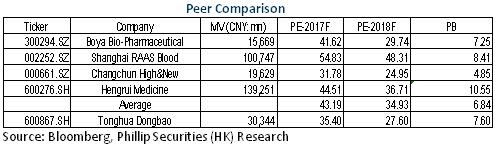

The company's insulin market share steadily increases, and its current market share of ordinary insulin is more than 20%, ranking second. Because of 2017 new National Drug Reimbursement List (NDRL) adjustment, second-generation insulin changed from the class B to class A, saving patients` annual costs by approx. RMB500-600, and is expected to further expand the grassroots market. Continued promotion of domestic grading clinics will also enhance the penetration of insulin products in the grassroots market. Moreover, compared to Novo Nordisk, Eli Lilly, the tender price of the company's products is more competitive. We believe that in the medium term the company's growth rate of second-generation insulin will remain at around 20%.

Abundant product reserve, prospective growth

The company's phase III clinical study of insulin glargine injection and aspartic insulin injection has entered the summary stage, and the former is about to apply for production, which is expected to be approved in 2018. So the company may become the third domestic insulin glargine injection manufacturer, which is only one year behind United Laboratories. Moreover, by virtue of a very close relation of cooperation with doctors and experts at grassroots level and third-grade class-A hospitals, the company is still expected to quickly occupy the market after its insulin glargine injection come to the market. In addition, the company's other insulin analogues, GLP-1 agonists, DDP-4 inhibitors and other hypoglycemic drugs echelon reserves are abundant, which will also provide support its long-term development.

Rapid promotion of diabetes chronic disease platform

The company rapidly promotes the construction of diabetes chronic disease platform, enhances the relationship between doctors and patient with the help of APP "your doctor", and achieves the integrated target of "insulin + blood glucose monitoring equipment + Dongbao diabetes platform" through the integration of drugs, equipment and mobile Internet, to help the company become a whole solution provider for diabetes patients with insulin therapy, and occupy the leading position in the field of diabetes. At present, registered doctors in APP "Your Doctor" are up to 7,000, and registered patients are more than 100,000, highlighting its rapid progress.

Risks

Expansion of second - generation insulin in grass - roots market is below expectations;

Progress of the launch of third-generations of insulin is below expectations.

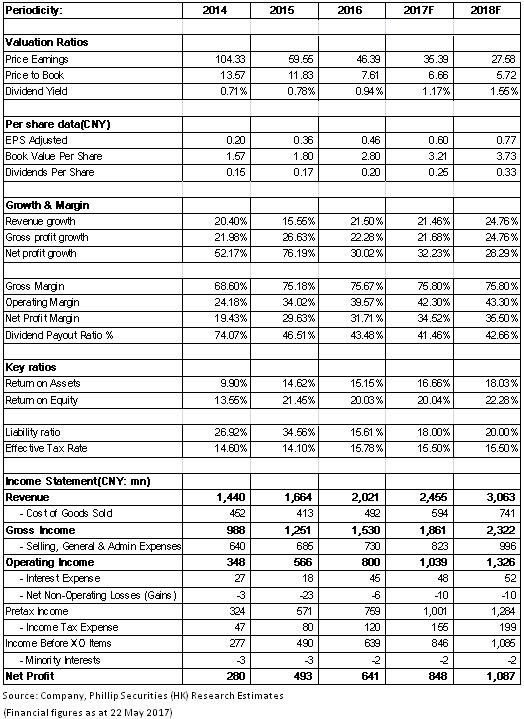

Financials

Click Here for PDF format...