Land Tender Summary

- Second project is won in Hong Kong, signaling a good progress on the geographical portfolio diversification by KWG Property

- The Kai Tak project will have good transportation infrastructure linking the residential site to the central business district in Hong Kong, via the Sha Tin to Central Link rail services scheduled for operation in 2019

- High demand and solid sales progress achieved by other developers in the Kai Tak area, such as One Kai Tak and K City

Overview

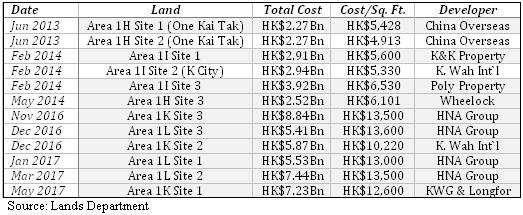

KWG Property won the second project in Hong Kong: After winning the land tender for a land in Ap Lei Chau with Logan Property, KWG Property has taken a step further by winning a second piece of land in Hong Kong. On 15/5/2017, the consortium of KWG Property and Longfor Property won the land tender for the land Area 1K Site 1 in Kai Tak, which has a site area of 104,600 square foot and a GFA of 575,500 square foot. KWG Property and Longfor Property submitted a bid and successfully acquired the land at a consideration of HK$7.23Bn, equivalent to a cost per square foot of HK$12,563. The market valuation for the Kai Tak land is between HK$6.33Bn and HK$7.48Bn, equivalent to a cost per square foot of HK$11,000 and HK$13,000 respectively, implying that the acquisition cost of KWG Property on the Kai Tak land is in line with market expectation.

KWG Property's first project in Kai Tak: The land Area 1K Site 1 is the last land in Area 1K and Area 1L for residential use in Kai Tak and is next to the land obtained by K. Wah International (Area 1K Site 2) and HNA Group (Area 1L Site 1 and Area 1L Site 2 via its subsidiary Hong Kong International Construction Investment Management). The acquisition cost paid by KWG Property and Longfor Property is lower than those paid by HNA Group and its subsidiary but could still be considered relatively high given that the land is located at the inland portion of the Kai Tak development area, which some of the view to the harbor may be blocked by other development projects. However, Kai Tak development area is one of the very limited development projects in the central part of Hong Kong with well-planned transport infrastructure, i.e. rail services, thus providing a solid assurance sales price in its properties.

Good progress on geographical diversification: In late February 2017, KWG Property and Logan Property formed a consortium and successfully obtained the land in Ap Lei Chau at a record-breaking consideration of HK$16.86Bn. The land is located by the seashore and has a spectacular view on the harbour, which is very rare at the centre of Hong Kong. Moreover, the additional land obtained in Kai Tak will enable the company to further establish its strategic positioning in Hong Kong and will become the foundation for the company's geographical diversification.

The primary benefit for the company to establish its strategic footprint overseas can be summarized as follow:

- Property projects in Hong Kong allows the company to establish a hedge against the possible depreciation of Renminbi by having currency exposure in HKD.

- The land obtained through public tendering and auction in China is expensive because of the aggressive land bidding strategy adopted by the Chinese property developer, eating away the profitability of developer. Engaging overseas can reduce the risk of deteriorating profit margin.

- Regulation in both the financing channels in purchasing land by developer and purchasing homes by Chinese citizens are tightened, increasing the difficulty Chinese property developer faces in operation. Engaging overseas can avoid the difficulties in obtaining finance for property development project.

In addition to the above benefits, the international diversification strategy will provide an intangible benefit of enhancing the brand name of KWG Property. Being able to operate in Hong Kong and overseas, both of which have stricter control in terms of regulations, and large number of investors who have high expectation on the quality of property, will enable the company to improve its brand name in China, thus allowing KWG Property to have more pricing power in its property projects in the future.

Investment Thesis & Valuation

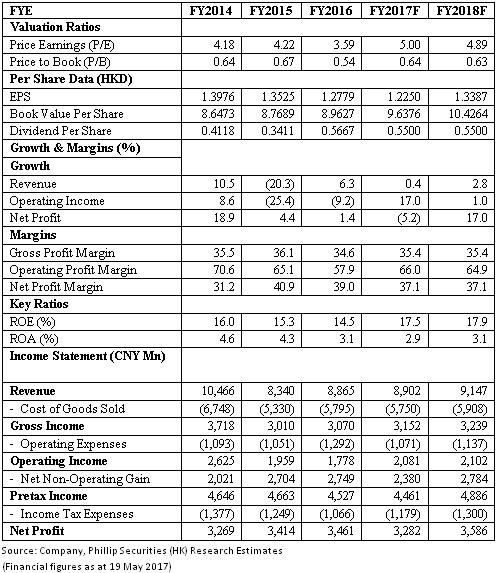

We will maintain our target price at HK$6.55: The two successful land acquisitions in Hong Kong signal the company's march towards the international property market. We believe KWG Property will have further acquisition internationally because of, but not limited to the abovementioned benefit. Therefore, we will stay tuned to its further action and will maintain our current expectation. The target price of HK$6.55 and the rating of `Accumulate` will be maintained. (Closing price as at 19 May 2017)

Financials

Click Here for PDF format...