Investment Summary

New medical insurance catalogue and medicine bid would definitely boost the strong growth of main products of the company. Introduction of new species is expected to bring about large trading volume. Besides, the continuous improved product echelon could support its medium and long term development. Meanwhile, principal shareholders made large subscription of directional private placement, which also reveal their confidence in the development of the company. We give an estimation of 30x EPS in 2017 and the target price is RMB112, with the "Buy" rating initially.

2016 Results Remarkably Exceeded Expectation

In 2016, Huadong Medicine recorded a revenue of RMB25.38 billion, up 16.8% year-on-year. Net profit excluding non-recurring items attributable to listed company shareholders was RMB1.41 billion, a YoY increase of 32.5%. Moreover, company planned to distribute cash dividends - RMB13.5 per 10 share (including tax) - to each shareholder and transfer every 10 capital reserves into additional 10 shares. This was the first time for company to deliver share in past ten years, which would improve its liquidity.

In detail, its pharmaceutical manufacturing business recorded a revenue of RMB5.85 billion, a YoY increase of 17.8%, gross margin at 80.5%, keeping a fast growth track. The core product Corbrin Capsule generated over RMB2 billion, with a growth rate of over 20%. Besides, Acarbose brought a revenue of over RMB1.5 billion, a growth rate of up to 30%. Three major immunosuppressive agents - Cyclosporine, Mycophenolate Mofetil, Tacrolimus - totally contributed to a revenue of approx. RMB1 billion.

The pharmaceutical commerce business generated RMB20.1 billion, a YoY growth of 16.4%, a gross margin of 7.9%, maintained at around 8%, which mainly benefited from higher concentration degree of pharmaceutical commerce business in Zhejiang province. Moreover, it is worth mentioning that the company was transferring from a traditional medicine distributor into a comprehensive health service supplier, whose subsidiary Ningbo branch was deliberately working on the field of medical cosmetology and Big-health. Its imported beauty product (the company served as an acting distributor) - YVOIRE - had maintained a 100% growth for three years in series. In 2016, its sales marked a record of over RMB400 million, net profit up to RMB149 million, a YoY growth of 62.53%.

In respect of expenses, financial expenses reached RMB90 million in 2016, a YoY decline of RMB120 million. Thanks to the directional private placement of RMB3.47 billion, its financial situation had been remarkably improved, which mainly contributed to the faster growth of performance than that of the revenue.

The adjustment of medical insurance catalogue facilitated its fast growth

According to the medical insurance catalogue of 2017, its three new kinds of medicine would be included in the catalogue. Acarbose tablet was reclassified from Class B to Class A. Furthermore, the indication limit of other three products, including Tacrolimus capsule, had been removed. Consequently, the company had become one of the beneficiaries by the courtesy of the new catalogue.

Corbrin capsule, firstly classified as tumour auxiliary medicine, now was classified as supplementary agent for Qi and Blood, which could benefit the future expansion of multi-department. Moreover, the target market of Corbrin capsule mainly focused on urban public hospitals. In the future, the promotion of tiered medical project would expand the whole market. Meanwhile, Fermented Cordyceps Powder project (Phase I), with annual yield of 1,200 ton, had successfully passed the GMP on-site examination, which could efficiently solve the capacity bottleneck problem. We believe Corbrin capsule will maintain a growth rate of over 20%.

The classification of Acarbose was changed from B to A. The enhancement of terminal paying capacity may trigger volume effect. At present, the largest manufacturer of Acarbose belongs to its original research supplier - Bayer. However, Huadong Medicine and Luye Pharma's products could enjoy the price advantage, which would not only strengthen its competitiveness in the bidding, but also help to increase its coverage in base market, overriding the original research supplier. In the future, the import substitution effect would be further enhanced, so the growth of Acarbose could maintain over 30%.

Besides, Daptomycin and Indobufen were initially included in medical insurance catalogue. Their trading volume will also be enlarged as the bidding regularly proceed in the future. Currently, Daptomycin had won the bid in Shanghai. Moreover, new catalogue had cancelled the indication limit of Tacrolimus oral agent and Cyclosporine, which could benefit their future expansion of multi-department.

Abundant product reserve

At present, in addition to the fields of enhancement of nephropathy, endocrine, immune suppression, digestive system and other specialized fields, the company also strived to expand new fields, such as anti-tumour, anti-infection of severe diseases and cardiovascular disease and so on. In 2016, the company had obtained 13 clinical approval, including Imatinib Mesylate tablet and Linezolid tablet, and 4 production approvals of Corbrin granule, Indobufen tablet, Decitabine raw material and preparation. In addition, in respect of Panlisu powder-needle, the company, as the first one that submitted ANDA application to American FDA and the submission was taken. Meanwhile, the company had started the clinical research of Tacrolimus Capsules overseas. As a result, the product echelon in pharmaceutical manufacturing business of the company will continue to provide momentum for its future development.

Risks

Price drop of major products exceeded expectation;

Marketing of products fell short of expectation;

The implementation of Two-votes system below expectation.

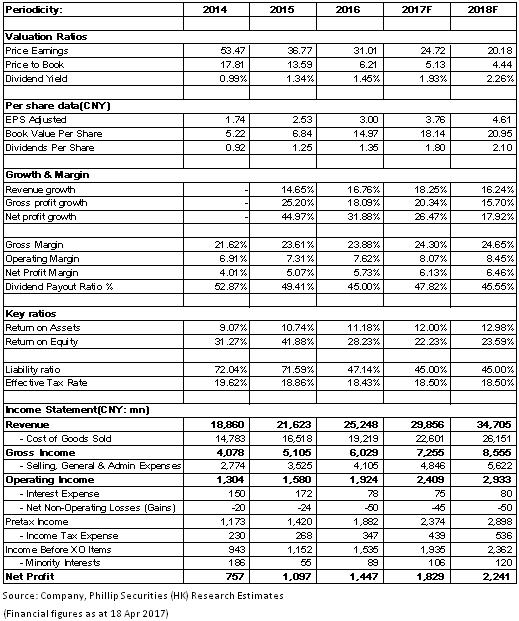

Financials

Click Here for PDF format...