Side-by-side growth of water and environment

Xingrong Environment was mainly engaged in water supply and sewage treatment business after it was successful listed, and then it marched into environment protection by landfill leachate, sewage and sludge treatment, reclaimed water service, waste-to-energy, etc., forming a diversified business structure of water and environment protection. At present, the company has eight water plants with the water supply of 2,325,600 tonnes/day and thirty-one sewage treatment plants with sewage treatment capacity of 2,247,400tonnes/day. Its business has covered seven provinces of China and Pakistan.

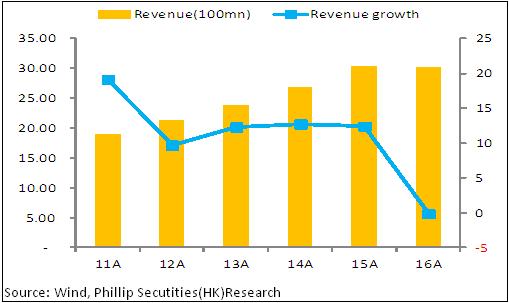

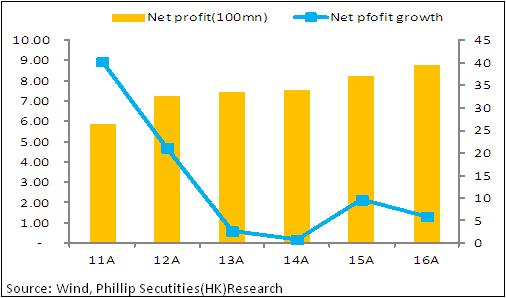

Results of 2016 rose steadily

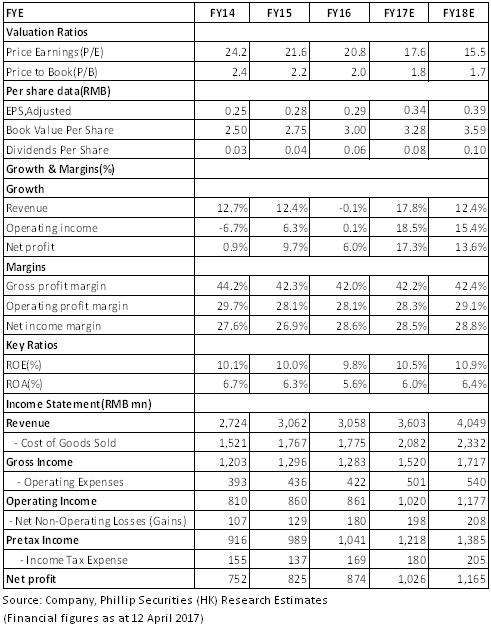

In 2016, the company recorded a revenue of RMB3.058 billion, slightly down 0.14%. To be specific, payable VAT specified by the applicable "Levy and Refund" returned RMB125 million which influenced part of the income. The net profit attributable to the shareholders reached RMB871 million, up 6% yoy. With respect to revenue structure, the income of water supply was RMB1.916billion(up 6.67%) and that of sewage treatment service was RMB915million(down 14.98%), total contributing 92.6%(93.82 in 2015). The income of landfill leachate and sludge treatment was RMB226million(up 19.7%).

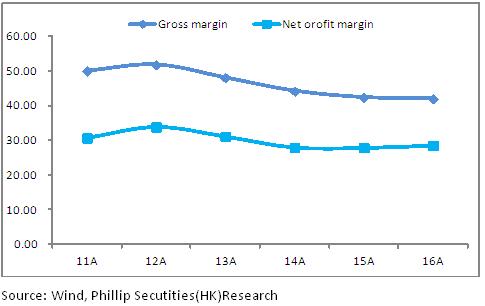

With respect to profitability, the company's gross profit margin was 41.95%, basically remaining unchanged. Its net profit margin was 28.5%, increased by 0.67 ppts yoy. With respect to cutting expenses, period expense ratio was down by 1.1 ppts to 12.38 ppts. In general, the company remained healthy development, with steady improvements in all economic indicators.

Speed up PPP+ "One Belt and One Road (OBOR) initiative"

During the period, the company recorded significant breakthroughs in developing domestic and foreign markets. In 2016, the company won the bid for PPP project of water supply in Pei County, Jiangsu and comprehensive utilization of water in Ning Dong town, Ningxia. Both projects were demonstration projects of the Ministry of Finance, with the total investment reaching RMB2.7 billion. In April, 2017, the company won another bid for the first phase of PPP project of drainage infrastructure in Wenzhou, with the total investment reaching RMB1.09 billion. Besides, the company also actively expanded international water markets such as India, Pakistan, the United States, Thailand, etc., establishing joint venture to accelerate the project of waste incineration for power generation in Lahore, Pakistan in accordance with laws by joint investment with China Enfei Engineering Technology Co., Ltd. and MCCT. We believe that based on PPP projects and opportunities of environment protection along the One Belt and One Road (OBOR) initiative, the company would accelerate the expansion of business. In the future, the gradual implementation of these projects will also bring great flexibility to the company's results.

Significant progress was made in financing capacity

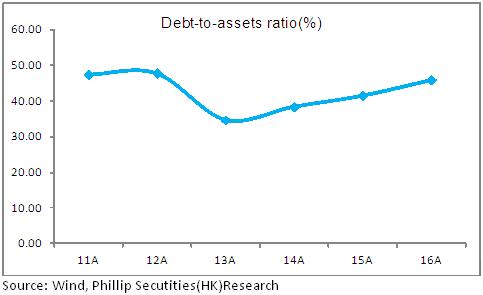

Due to the increasing investment in projects under construction and the repayment of ultra-short-term commercial paper, in 2016, money funds of the company dropped by RMB815 million YoY to RMB1.67 billion, the debt-to-asset ratio increased by 4.45 ppts yoy to 45.9%, liquidity ratio and the quick ratio continued to decline as in 2015. However, thanks to the contribution of supply and drainage business, the company boasted consistent and steady cash flow for operating activities. In 2016, the company recorded RMB1.42 billion cash flow for operating activities, up 6.4% yoy. The fast funds recovery enables total solvency risks to remain controllable.

Besides, the company is also actively expanding its financing channels. During the period, the company issued corporate bonds worth RMB1.1 billion with a coupon rate of 2.95% and ultra-short-term commercial paper worth RMB0.5 billion with a coupon rate of 2.93%. At the same time, the company earned the top AAA credit rating and the bank's credit, with its credit limit reaching as much as 13.2 billion. We believe that under the trend of water and environment protection capitalization, the company will constantly improve its financing capacity and its brilliant credit level will help optimizing its financial structure, offering powerful financial strength for business expansion.

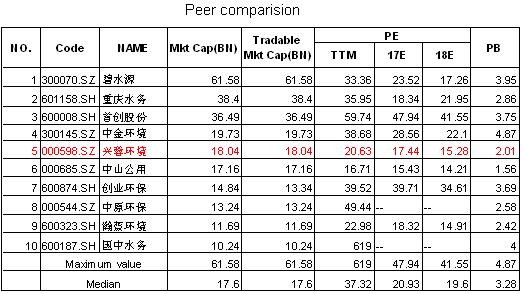

Valuation and rating

1)Compared with A share counterparts, the valuation of the company is low and its current stock prices correspond to 21x PE, 2xPB, with a higher margin of safety. 2) The company's water supply and drainage business remain robust with a stable cash flow. Meanwhile, its PPP project and the "One Belt and One Road" market expansion have provided momentum for its long-term development. Therefore we expect its robust future performance. We expect the net profit attributed to the company to be RMB1.026/1.165billion, a 0.34/0.39EPS, a 17.6/15.5PE corresponding to its current stock prices in 2017-2018. We give a target price of RMB7.31 and a rating of Buy for the first coverage. (Closing price as at 12 April 2017)

Risk warnings

PPP implementation is below expectation.

International market expansion is slow.

Market competition is fierce and expansion in non-local markets is impeded.

Financials

Click Here for PDF format...