We had a conference call with Goldpac Group's management to conduct research on the company.

Investment Summary

- The company will strengthen core business competitiveness. The company has a long history with stable business development and will further enhance operational automation, systematization and optimize the product mix.

- The company will accelerate diversified business and innovation development and continue to accelerate the smart wearables market.

- The company has sufficient cash on hand and has been increasing the dividend payout ratio in recent years. The dividend payout ratio may reach 61% in 2016.

- Overseas business has growth potential.

- The company's future M&A activities are worth anticipating.

Company Business

The business of the company includes embedded software and secure payment products segment and platform and service segment.

Embedded Software and Secure Payment Products: The company develops hardware and software for security payment products, in which the security and payment softwares loaded into the chips and the operating system development are the core technology. This segment also includes the card design, technology development, manufacturing and so on.

Platform and Service: Provision of personalisation service, system platforms and other solutions for customers in a wide business range including financial, government, healthcare, transportation and retails by leveraging innovative Fintech.

Platform and service segment includes:

Personalisation Service: After the hardware and software development and the manufacturing of the cards, the company encrypts the cardholders` account data and personal information into the cards and sends them to the cardholders from the data centre.

Card Issuance System Solutions: The business includes mobile financial services in temporary places such as airports, shopping malls, clubs and communities. The company provides on-site card issuance terminals, software development, security systems and data systems.

FY2016 Results

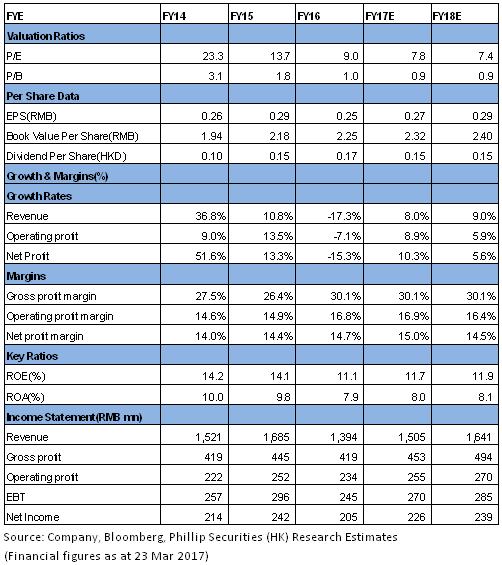

In FY2016 the Group recorded a turnover and a net profit of approximately RMB1,393.7 million and RMB204.9 million, representing a YoY decrease of 17.3% and 15.3% respectively. The Group's performance in 2H2016 is better than 1H2016. Compared to 1H2016, the Group's turnover and net profit for 2H2016 achieved an increase of 4.5% and 14.8% respectively.

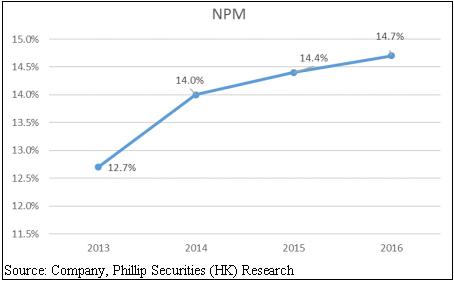

The gross profit margin and net profit margin were approximately 30.1% and 14.7%, representing an increase of 3.7 percentage points and 0.3 percentage points respectively as compared to the preceding year. The improvement is mainly attributed to the growing innovative product business and improving product portfolio. The following chart demonstrates the NPM from 2013 to 2016.

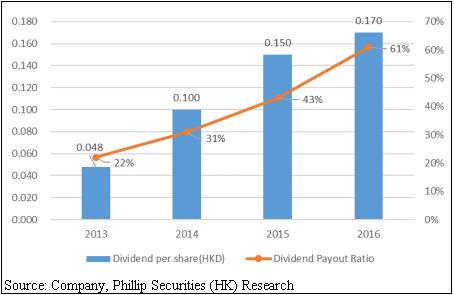

As at 31 Dec 2016, the cash available for use is RMB 1,763 million. Net cash per share is RMB2.11. The Board proposed to declare a final dividend of HK7.0 cents per ordinary share and a special dividend of HK6.0 cents per ordinary share. Including the interim dividend of HK4.0 cents, the dividend payout ratio of FY2016 will be 61%. The following chart shows the dividend per share and dividend payout ratio in recent years.

Industry Opportunities

In June 2016 PBoC issued the "PBoC's notice on further strengthening the risk management of bank cards", requiring shutting down the magnetic stripe transactions of chip magnetic stripe composite cards from 1 May 2017. The notice also asked commercial banks to speed up the replacement of magnetic stripe card with the financial IC card.

From 2012 to 2015, due to the changing demand from magnetic stripe card to card with chips, the industry profit increased fast. The revenue and net profit of the company increased by 149% and 110% from 2012 to 2015. In 2016 the industry began to enter the stock replacement stage. In addition, the product replacement cycle of cards with trips is 3-5 years, the industry scale will develop more stably in the future.

New credit card policies implemented by PBoC on 1 Jan 2017 will aid in the promotion of the credit card market, lifting limits associated with interest-free payment periods and minimum payment. There policies are expected to help push forward the diversification and differentiation of credit card products and services. China's credit card market develops relatively slowly, which is related to the perfect degree of the credit system and risk management, but credit card has security advantage. Credit card industry may develop faster in the next few years and credit card products are expected to face refinement competition.

In 2015 Chinese government announced the opening of the RMB clearing market. Visa, MasterCard and other card organizations are expected to enter China market to promote their own branded financial businesses earliest at the end of 2017 or at the beginning of 2018, and this will bring new incremental demand for China credit card market.

Industry Challenges

Although the mobile payment needs to bind the bank card account and this does not affect the issuance demand of the bank card as a bank account certificate, the bank card payment still faces the competition of mobile phone payment such as Alipay and WeChat Pay.

In addition, the government's regulation of on-line finance and third-party payment services is more and more strict, and the shipment volume of the company decreased in 1H2016. The main purpose of the regulation and control of the financial industry is to control financial risks. Although it will bring periodical pressure to the whole industry, it will have positive impact in the long run. With the regulation of the financial market being more and more strict, the market will become more and more standardized and will slowly return to a rational state, which is conducive to the financial system's main force¡X¡Xthe banks and may benefit the company in the long run.

Diversified Procurement of Domestic and Foreign Chips

The chip is currently the main procurement cost of IC card. In 2016 the company's procurement costs of chips decreased. In 2017 the company will continue to control procurement costs. Procurement will also become more and more diversified. The competition pattern of chip market has changed.

The policies are tilting towards domestic chips and other imported chip brands are also entering China market. The company's bargaining power for suppliers is also increasing.

Product Mix Optimization and Further Development of Automation

The company promotes product diversification and product structure optimization and also promotes high value-added and high-margin products to help ease the pressure on prices. Guided by Industry 4.0, the company will enhance operational digitization and informatization to improve the company's operational efficiency.

Diversified Business Development and M&A Anticipation

In the future the company will strengthen the core financial card business as well as diversify the product mix. It will develop diversified industry products such as cards on livelihood for smart city and intelligent transportation development and high-end retail cards (such as Starbucks Card). In 2017 the innovative development will focus on the GCaaS platform, intelligent security equipments, system solutions and provide the financial institutions with more comprehensive financial services.

The company has healthy financial situation and has sufficient cash on hand. The future M&A activities are worth anticipating.

Overseas Business Has Growth Potential

The company is actively promoting the global business expansion strategy and the overseas layout is developing steadily. Accompanied with China UnionPay's international development and overseas EMV chip replacement demands, the company is developing localized products and platforms and sees the potential of Southeast Asian market. The proportion of overseas business is expected to increase in the future.

Valuation

Buy Rating is given with TP of HK$3.00. We expect net profit growth of 10.3%/5.6% in FY2017/FY2018, driven by 8.0%/9.0% revenue growth. Our TP of HK$3.00 represents 9.8/9.3x FY2017E/FY2018E P/E. (Closing price as at 23 March 2017)

Risk

The competition of mobile phone payment such as Alipay and WeChat Pay;

The development of overseas business is below expectation.

Financials

Click Here for PDF format...