The Water Industry: On the Up

The company's major businesses include tap-water manufacturing and selling, engineering installation and related water treatment business. 1) Water supply is a sustained and stable industry: Disparities between water supply and demand has been highlighted by continuous growth of water consumption driven by economic development and urbanization, residents` demand for high-quality, healthy drinking water, as well as water shortage aggravated by increased water pollution. China's water fee is inexpensive relative to that in the world, currently accounting for a mere 1.2% of personal income as contrasted with the international level of around 4%. There is still substantial room for rise. 2) The sewage treatment industry is booming with stronger policy support: The new Environmental Protection Law of PRC, "Water Pollution Control Action Plan", Construction Planning of National Urban Sewage Treatment and Recycling Facilities in the "Thirteenth Five-Year" Period and other policies have been issued. In the ൕth five-year" period, the upgrading and reconstruction of urban sewage treatment facilities will present huge market for investment, with the total investment in construction reaching approximately RMB582.9 billion, higher than in the ൔth five-year" period by 35.6%. Driven by intensive policies, the huge market volume in the market segments needs to be released soon.

Sound Growth in Water-Supply Strength and Rapid Growth in Engineering Installation

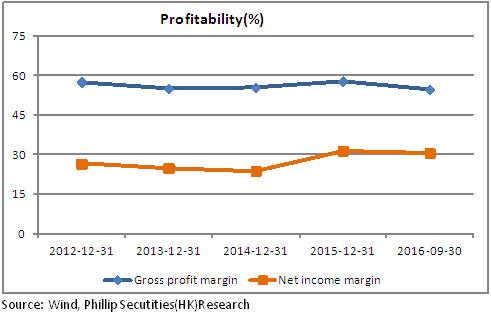

The tap-water business recorded a revenue of RMB231 million in 1H 2016, representing an increase of 4.1% yoy and accounting for 40.2% of total revenue, with a gross margin of around 50%. As of 2015, the company owes four ground water plants with a total designed capacity of 1.16 million ton/day. Its source of tap water, drawn from the Yangtze River belonging to surface water category II, has apparent edge in quality. In addition to the concession to operate water supply in Jiangyin city, it also owns a complete water-supply chain covering water intaking from sources, tap-water purification, sales and after-sales service. The ladder-like fee for water for residential use in Jiangyin has been implemented since January 1, 2016, and the company has also been accelerating the transformation of rural water supply pipe network for integrated development of urban and rural water supply and improvement of the principal water-supply services.

The wholly-owned subsidiary Municipal Engineering Company is mainly responsible for the engineering business, and is the only enterprise in Jiangyin that can independently undertake mid- and large-scale installation and construction of tap-water pipes. In 1H 2016, the revenue and profit from external engineering business recorded an upsurge, which can be attributed to constant expansion of the business. Among them, the revenue rocketed by 146.6% yoy to RMB328 million, the net profit soared by 127.3% yoy, and the gross margin stood at 56.88%, contributing to total-profit growth by more than 50%.

New Progress Made in Extension of Industrial Chain

Gratifying progress has been made in extension of water industrial chain and sewage treatment business. In mid-term 2016, the Huangtang sewage treatment plant signed contract on sewage treatment with 141 companies with the contract amount rising by 25% yoy; the Nanzha sewage treatment plant undertook the construction of internal sewage pipe network of another 16 companies. The preliminary work of solid waste disposal business layout has launched. Jinxiu Jiangnan Environmental Development Company has launched the preliminary work of Jiangyin Qinwang Mountain Comprehensive Utilization of Industrial Waste Project, and the work is running smoothly.

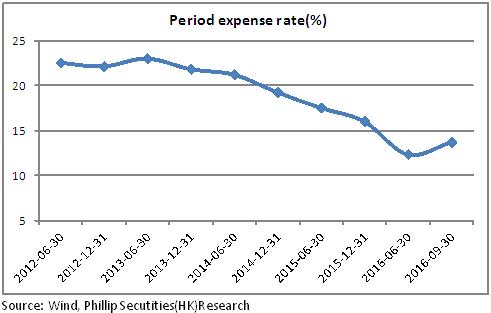

Financial Stability Maintains

The company's cash flow is abundant and stable, with the book amount ranging from RMB1 to 1.4 billion. At the same time, it has low debt burden, with the liquidity ratio and the quick ratio standing at 2.5/2.2, respectively, and the asset-liability ratio kept below 45%, less than the industry average of 50%. The abundant capital and sound finance will benefit business expansion. Moreover, during the period the company was also involved in initiating the industrial fund regarding investment and operation of environmental industry projects, which is expected to expand the investment channels, reduce the financial risks and enhance the income from investment.

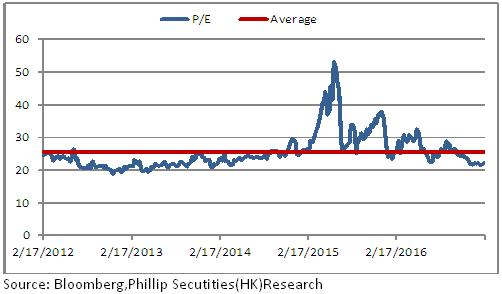

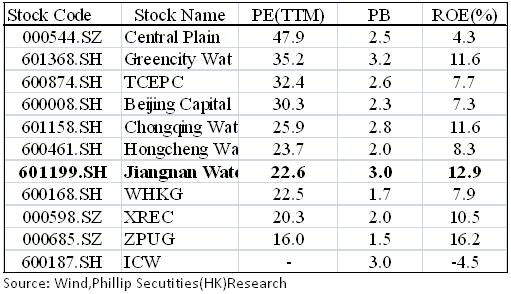

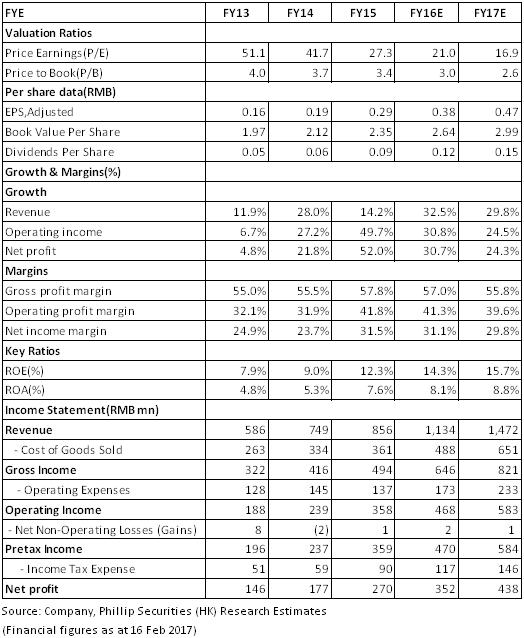

Valuation and Rating

1)The company's valuation is relatively low relative to the valuation of listed companies in the same field, and in recent years it has maintained a payout ratio of more than 30%, the momentum of which is likely to continue; 2) The sustained, steady water-supply business can provide abundant and stable cash flow, and the expansion of engineering business can boost overall profitability; (3) The expansion of sewage treatment and solid waste disposal will bring great flexibility to the company's results. On this basis, we expect the 2016 and 2017 net profit attributable to the company to be 352/438 million, respectively, and EPS to be 0.38 and 0.47, respectively, and P/E ratio to be 21.0 and 16.9, respectively. The target price is 10.50,and the buy rating is given. (Closing price as at 16 Feb 2017)

Risk Warnings

Risk of fluctuations in policy;

Rapid growth in operating costs;

Great difficulty in out-of-the-region expansion and fierce competition.

Financials

Click Here for PDF format...