Mid-term Performances below Expectations

In 1H 2016, Kangda International Environmental Company Limited realized a revenue of RMB902 million, up by 15% from RMB785 million over the same period last year. Specifically, the revenue from construction was the main driving force of the revenue growth. First, as more BOT projects were implemented, the revenue from which increased by RMB116 million YoY to RMB433 million. Second, financial revenue increased slightly by RMB36 million YoY to RMB205 million, while the revenue from operations dropped by RMB35 billion YoY to RMB263 million, offsetting a part of the growth. The net profit growth was lower than expectations, dropped by 13.76% YoY to RMB122 million. The EPS decreased by 17.9% YoY to RMB0.0546, mainly attributable to the decrease in gross profit margin and the rapid growth in expenses over the period.

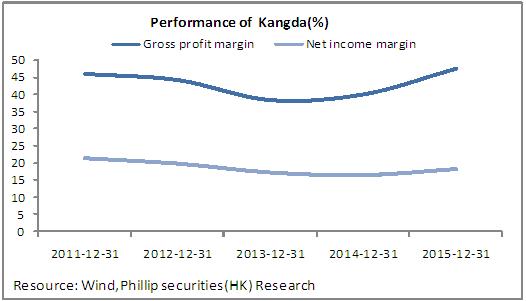

In respect of profitability, the gross profit margin fell by 5% to 42% YoY, mainly affected by "replacing the business tax with a value-added tax". In respect of costs, administrative expenses increased significantly by 25.8% YoY to RMB105 million, while financial expenses increased by 10% YoY to RMB130 million. Taken together, the net profit margin reached 13.52%, representing a YoY decrease of 4.5%.

PPP Projects Speed Up to Boost Performance

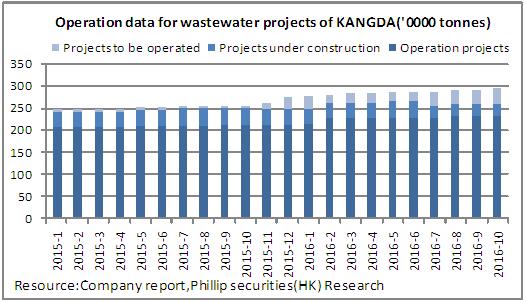

In 2016, the company's traditional water treatment capacity began to resume growth. As of the end of October, the company's total daily sewage treatment capacity reached 2.969 million tons, up by approximately 16.3% YoY, with an added treatment capacity of 192,500 tons/day; and sewage treatment capacity in operation reached 2.309 million tons, up by about 9.1% YoY. In addition, the company was further involved in the sludge treatment industry, adding a sludge treatment capacity of 400 tons per day within the period, which is expected to work with sewage treatment projects to enhance the company's competitiveness.

The company seized the opportunities brought by the PPP model and gradually transferred its business focus from the traditional water projects to the PPP projects. Up to now, the company has newly added three PPP order items (Guangdong Yunan PPP Project, Shandong Rushan PPP Project and Henan Hebi PPP project), with a total investment of RMB3.15 billion. Moreover, the company also gained more than 10 BOT and TOT projects, with a total investment of RMB1 to 2 billion. Benefiting from favourable policies, the company actively involved itself in transformation and PPP projects. With years of experience in the water markets of second- or third-tier cities, the company is expected to acquire and complete more PPP projects, boosting future performance with great rate of return.

Significant Revenue Growth from Investment after Buying into Zhongyuan Asset Management Co., Ltd.

On September 1, the company acquired 15% equity of Zhongyuan Asset Management Co., Ltd. for RMB450 million in cash. Zhongyuan Asset, the only local asset management platform in Henan Province, signed a strategic cooperation agreement on finance and eco protection with some municipal and county-level governments in Henan Province (for example, Xinxiang City, Hebi City and Jiaozuo City). The agreement is expected to bring more PPP projects to further consolidate the company's first-mover advantage in the number and project promotion.

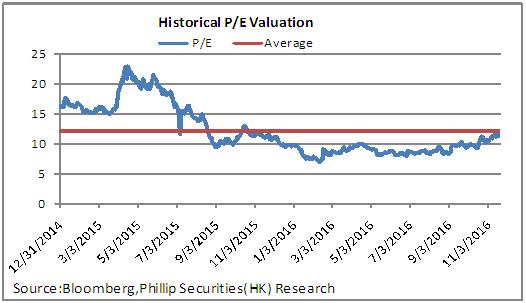

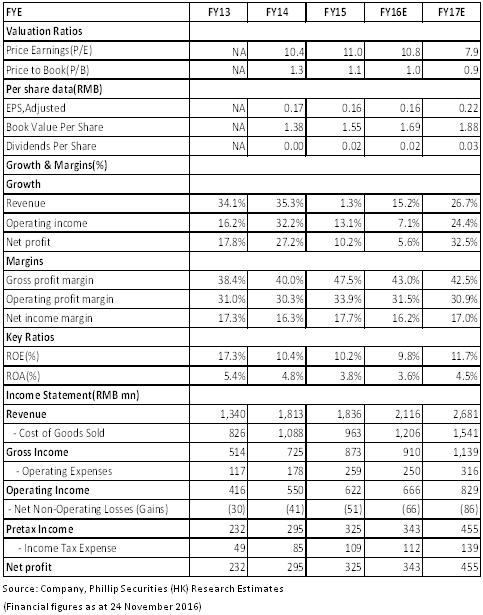

Overall, although the company's performance growth is lower than expectations in 1H, we are confident about the rapid growth in the performance for the next two years. With the PPP projects gradually yielding results, the company's performance is expected to usher in the turning point. Therefore, we give the company an estimation of 12.5x PE in 2017 and the target price is HK$2.38. Also, the "Buy" rating is maintained. (Closing price at 24 November 2016)

Risk Warnings

New projects fell short of expectations;

Yield rate of PPP projects fell short of expectations;

Continued depreciation of the RMB;

Financials

Click Here for PDF format...