Interim Net Profit Soared by 161%

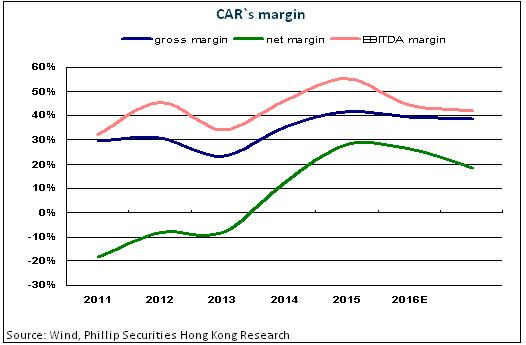

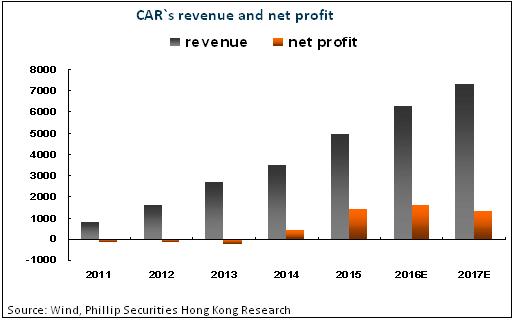

CAR announced the interim results as of June 30, 2016. Its net profit amounted to RMB 1.062 billion (same below), representing a YoY soar of 160.73%. EPS was RMB 0.444, as compared with RMB 0.172 in 2015H. No interim dividends. During the reporting period, turnover stood at RMB 2.969 billion, increasing by 28.67% year on year. Gross profit was RMB 1.103 billion, up 13.27% over the previous year, while the gross profit margin dropped from 49.1% to 45%, which mainly results from the increase in depreciation and increase in the costs of the new business of B2C second-hand vehicles.

Significant reasons for soar in profit are as follows: The fair value gains derived from the equities in UCAR Technology (China) Limited stood at RMB 827 million, and the unrealized foreign exchange losses of some dollar-denominated liabilities amounted to RMB 116 million. If such impact is excluded, the actual net profit increased by around 12% as compared with the same period last year.

Growth in the Fleet Size Continued to Decrease

In the early stage, the Company has decided to make adjustment in its development strategies, slow down the pace of expansion and change from extensive growth to giving priority to efficiency. As of the end of June, the Company's total fleet size reached 99,727 units, rising by 17.7% over last year, and growing by 9.4% as compared with the end of 2015. The fleet size stood at 87,585 units, increasing by 8.6% over the previous year but only by 5.3% as compared with the end of 2015. The Company's capital expenditure in H1 2016 amounted to RMB 1.26 billion, representing a YoY plunge of 70% but a MoM increase of 19.5%. In the second quarter, the Company sped up the phase-out of old models and the upgrade of new models in order to enhance the customer experience, while actively promoting free car delivery services to consolidate its competitive edge.

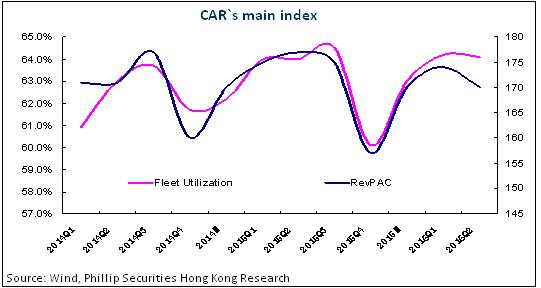

Cooperated with UCAR Inc. to Boost the Fleet's Operational Efficiency

The Company's short-term rental income surged by 16% over 2015 to RMB 1.7 billion, which is basically consistent with the increase of the total fleet. Besides, its long-term rental income skyrocketed by 57% over the previous year to RMB 722 million, which is primarily attributable to the growth in the fleet of UCAR Inc. Approximately 10,000 long-term rental vehicles and 20,000 short-term rental vehicles of the Company were rented to UCAR Inc. By means of cooperating with UCAR Inc., the Company optimized the management of dynamic fleet sharing in low and high seasons, boosted the utilization efficiency of the fleet which moderately increased by 0.2 percentage points to 64.1% and offset some negative impact of a 2.5% drop in the average daily rent.

Free Cash Flow Turned from Outflow to Inflow

Benefiting from the decline in capital expenditure on rental vehicles and the rise in cash flow from operation, the Company's free cash flow improved from last year's outflow of RMB 3.76 billion to this year's inflow of RMB 784 million.

Formal Promulgation of New Ride-hailing Policy Contributed to Indirect Benefits

At the end of July, the government formally promulgated the new ride-hailing policy. We believe that this policy produces more significant adverse effect on major competitors of UCAR Inc. and will prevent the C2C platform's exorbitant expensive, thereby lowering the price pressure faced by UCAR Inc. and indirectly benefiting the long-term development of the Company's future business.

Investment Thesis

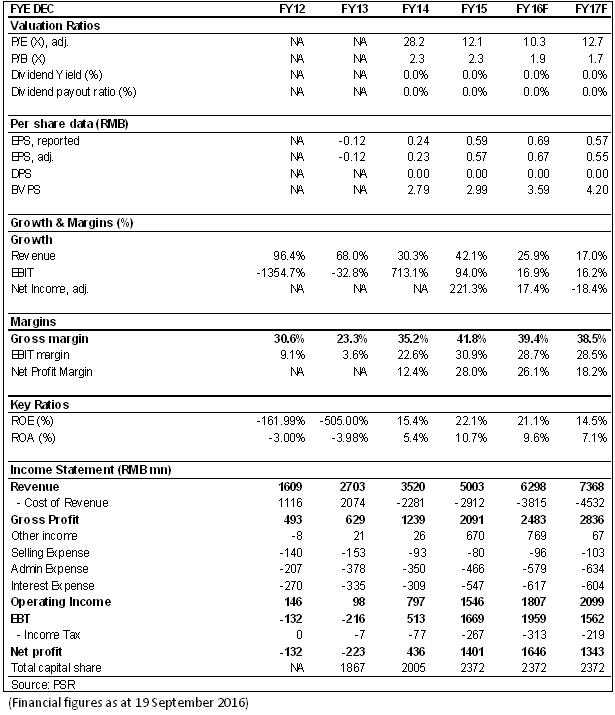

We adjusted the earnings per share to RMB0.69/0.57 in 2016/2017. The company's current valuation has relatively great safety margin, and we still believe that the innovation and strong power of execution of the company will enable us to face future challenges. We give a target price of HKD9.61, equivalent to the 12/14.7 x P/E ratio in 2016/2017. The accumulate rating was reaffirmed. (Closing price as at 19 Sep 2016)

Financials

Click Here for PDF format...