Annual Increase of Profit by 35.6%

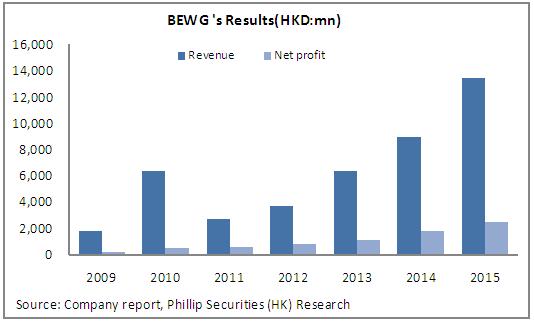

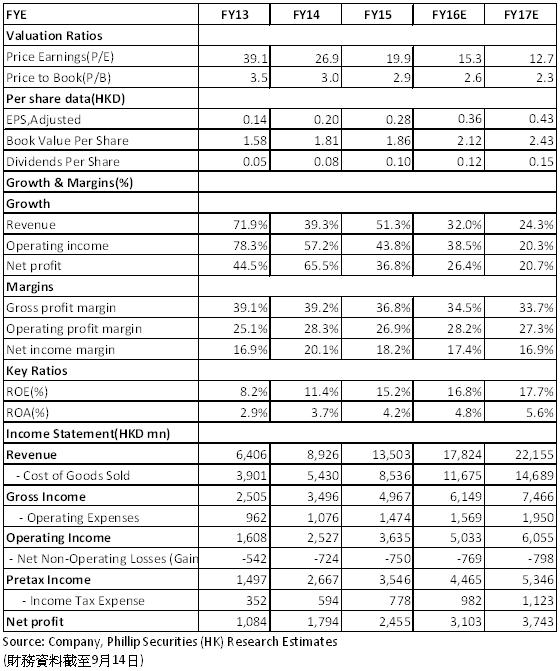

In H12016, BEWG's revenue amounted to HKD7.85 billion, representing a year-on-year growth of 36.2%, which is mainly attributable to comprehensive water environmental renovation projects and BOT construction service. The gross profit stood at HKD2.702 billion, soaring by 19.7% Y-o-Y. Profit attributable to shareholders was HKD1.574 billion, increasing by 35.6% over the previous year. Besides, EPS was 18.08 HK cents, while the interim dividend per share was 5.9 HK cents. Excluding the returns on derivatives, the dividend pay-out ratio reached 37.6%. The management expects continuous and steady growth of net profit by 30-35%.

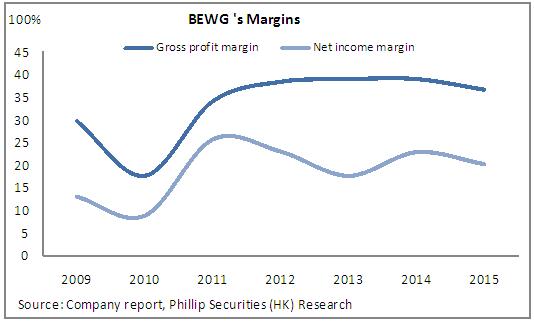

In respect of profitability, the gross profit margin fell by 5% to 34% Y-o-Y, mainly affected by the decline of that of water treatment service. Along with rapid expansion of business operations, the company performed well in cost control. The management expense ratio and financial expense ratio recorded a Y-o-Y decrease by 0.93% and 1.79%, respectively. In general, the company realized a net profit margin of 20.04% that basically remained the same as that of the last year.

Surge of Revenue of Construction Service

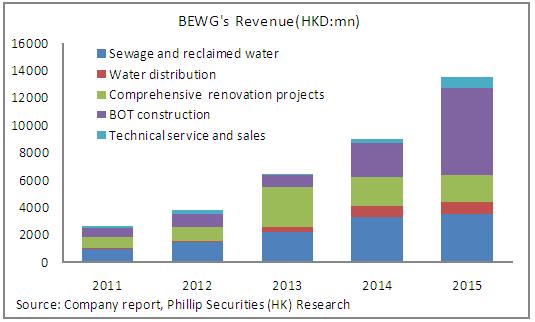

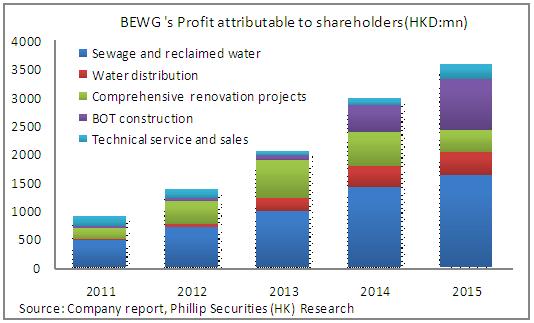

In terms of water treatment service, sewage and reclaimed water treatment recorded a Y-o-Y decrease by 10% to HKD1.635 billion. The gross profit margin fell by 7% to 60% mainly due to the adjustment of VAT. Water distribution revenue was HKD598 million, rose by 52% Y-o-Y, while the gross profit margin declined by 7%, mainly because of the low gross profit margin of the newly acquired project.

With respect to the renovation and construction of water environment, the revenue of comprehensive water environmental renovation projects was HKD1.8 billion, rocketing by 97% Y-o-Y. The gross profit margin increased by 7% to 24%. BOT construction gained HKD3.438 billion revenue, representing a Y-o-Y increase of 43%. The gross profit margin maintained at 24%. The company seizes the opportunities brought about by PPP. Currently, the company has established three PPP industrial funds for PPP projects, which are expected to drive the rapid growth of revenue and profit in terms of renovation and construction service of water environment.

Maintaining the Target of New Processing Capacity for the Whole Year

The new daily processing capacity was approximately 1.873 million tons. 72% of the newly added capacity came from PPP projects, while the rest was from TOT and BOT projects. The daily processing capacity completed was 347,000 tons. The net growth of daily processing capacity stood at 1.525 million tons. The company is confident to achieve the target of new processing capacity at no less than 3 million tons. As of the end of June 2016, the gross daily processing capacity was 24.94 million tons, wherein that yet to be operated was 10.36 million tons. According to the target of 40 million tons of DPC by the year 2018, the compound growth rate is expected to reach 26.5%.

Debt Burden Expected to Drop

Cash on hand of the company was HKD5.5 billion, decreased by HKD830 million than that at the end of 2015. The increase of expenditure mainly was used in acquisition and the construction of multiple water projects. Due to the increase of debts from bank and other borrowings and corporate bonds, the net debt-to-asset ratio rose to 145% from 122% in last year. The company intends to reduce its debt burden. It started to establish PPP funds to promote the asset-light operations. The company is also expected to take additional measures to further decrease its net debt ratio.

Investment Rating

As a national leading company in water service, its strength in winning PPP contracts and the favourable returns on PPP projects guarantee the quality growth of performance. We remain optimistic about its fast growth of performance. So we give the company an estimation of target price of HKD7.20, equivalent to 20X expected P/E in 2016. Also, the "Buy" rating is maintained. (Closing price as at 14 September 2016)

Catalyst

Continuous expansion of the production capacity of water treatment service

Rapid growth of water environmental renovation projects

New progress of PPP funds

Risk factors

The growth of production capacity and new projects failed to meet expectations.

Financials

Click Here for PDF format...