1H16 Performance Worse than Expectation

In the first half of 2016, KPC Pharmaceuticals obtained RMB2.5 billion of revenue and RMB225 million of net profit after deduction of non-recurring gain/loss attributable to the shareholders, with an increase of 14.23% and 13.98% YOY, but lower than estimates.

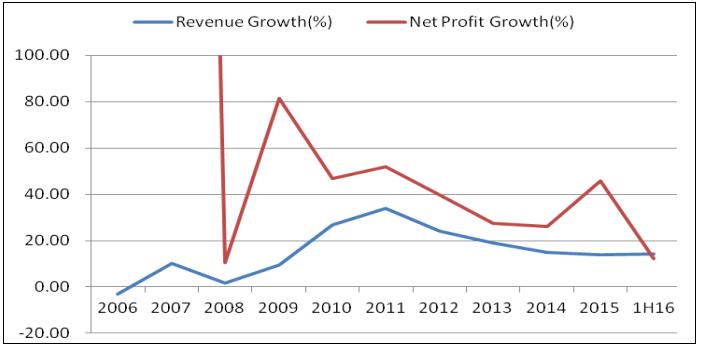

Improved Performance of KPC Pharm

Source: Company reports, Phillip Securities (HK) ResearchSpecifically, the Company achieved a steady growth of 12% for its Xuesaitong series. The sales of Xuesaitong Soft Capsules rose rapidly. The Xuesaitong Injection had practically safe and reliable curative effects. Its standardization was approved as a key national project, we believe it can gain a greater market share under the background of restricted use of TCM injections. Moreover, the revenue from synthetic drugs amounted to RMB274 million with an increase of 10.45%. The pharmaceutical business revenue jumped by 20.67%, mainly thanks to financial support and fine management.

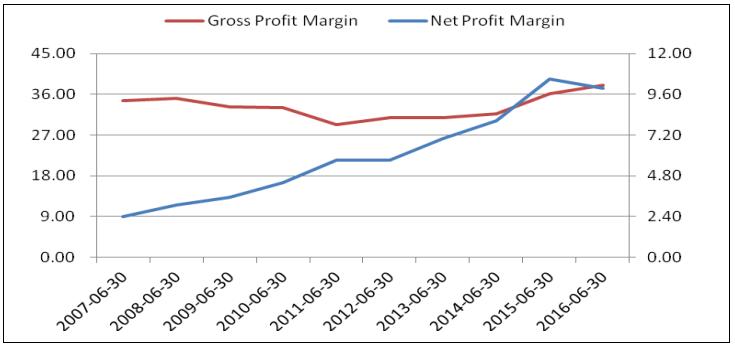

Regarding profitability, the gross profit margin reached 37.8% with a year-on-year increase of 1.5 percentage points, which mainly resulted from the gross profit margin of botanical drugs elevated by 9.6 percentage points to 74.5% as well as the drug wholesale and retail gross profit margin raised by 0.2 percentage points. However, the corporate marketing channels penetrated into the grassroots and the market promotion expenses increased, so the marketing expense ratio also rose by about 2 percentage points to 20.7%. As a result, the net profit margin dropped by 0.5 percentage points to 10%.

Improved earning capabilities

Source: Company reports, Phillip Securities (HK) ResearchRapid Growth Still Expectable

During the past ten years, the operating results of the company have basically maintained a high growth rate of over 20%, except in 2008 and 2014 when the growth rate went below 20%. Though the result was not as good as expected in 1H16, we keep optimistic about the mid- and long-term development of the company.

Firstly, the company has continuously pushed forward its refined marketing reform, set up new business departments like OTC, increased investment in the marketing business line integration and channel penetration, and strengthened incentives for frontline personnel. The Company's marketing advantages are expected to be intensified.

Secondly, upon the changes in the controllers of Zhongheng Group, the core product Xuesaitong Injection of KPC Pharmaceuticals may face the competition pattern reconstruction and its sales can increase steadily each year of 5-10% in the mid-term. While its exclusive products Xuesaitong Soft Capsules are estimated to embrace a high growth rate of around 30% exactly by virtue of the dramatically strengthened safety of oral preparations.

Furthermore, Tianxuanqing series are primarily used for neurological diseases with remarkable competitive advantages. Gastrodin Injection features high quality and competitive price. Acetagastrodin Tablets are exclusively owned by the Company. Besides, the Company plans to release "Liver-Soothing Granules and Xiangsha Pingwei Granules" as the golden prescription drugs and "Banlan Qingre Granules, Shenling Jianpiwei Granules, and Qingfei Huatan Pills" as the golden OTC drugs. Resources will be pooled to make a breakthrough in the sales volume of these five golden products and further drive the speedy increase in the botanical drug series.

What is also worth mentioning is that the expense ratio was relatively high and the conformance assessment expense was not capitalized in 1H16, so the growth rate of operating result is expected to remain above 20% if such expense is capitalized at the end of the year.

Further Expansion of Medical Service Businesses

KPC Pharmaceuticals is actively building a management ecosystem centered on cardio-cerebral-vascular diseases and other chronic diseases. It engages in the O2O diagnosis and treatment of cardio-cerebral-vascular diseases by investing the "Orange Doctor". Recently, it also cooperatively establishes the rehabilitation hospital and expands medical service businesses on the platform of Nanjing Hongjing and based on the operation of pharmaceutical business. It adopts the model of uniting pharmaceutical enterprises, agents and hospitals, which can be quickly copied into chain operation of rehabilitation service in the future. There is also a chance that the Company will actualize a series of mergers and acquisitions across Yunnan Province in the future, which can promote the chronic disease management business continually.

Valuation

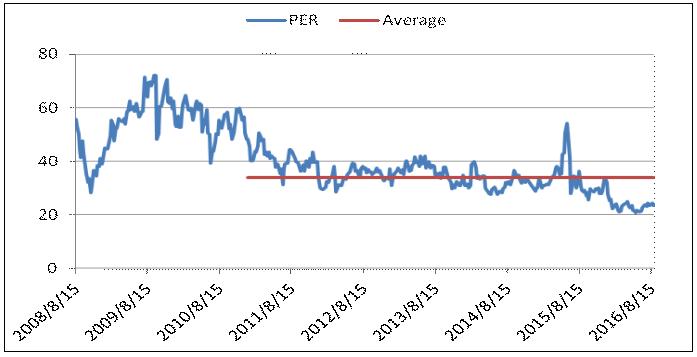

In general, there is still large space for the development of the Company's Kunming traditional Chinese medicines and Xuesaitong Soft Capsules, etc. Concurrently, the Company focuses on creating the chronic disease management system, speeds up its medical business layout and shows a strong intention to engage in epitaxial mergers. We give an estimation of 27.2x EPS in 2016 with the target price of RMB18.18, with the "Buy" rating maintained. (Closing price at 25 Aug 2016)

Historical P/E valuation

Source: Bloomberg, Phillip Securities (HK) ResearchRisks

The rising prices of traditional Chinese medicinal materials;The drug development progress slower than expectation;The progress for extensions falls short of expectation.

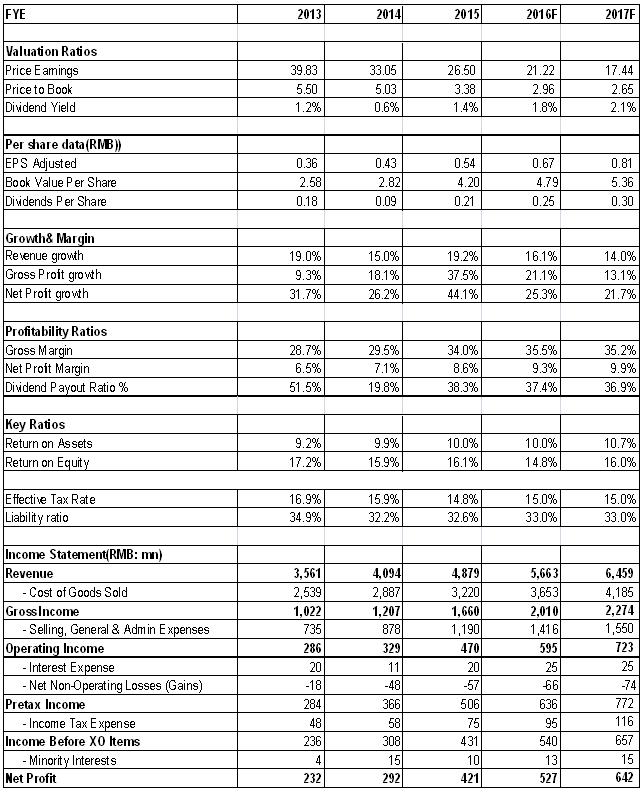

Financials

Source: Company, Phillip Securities (HK) Research Estimates(Financial figures as at 25 Aug 2016)Click Here for PDF format...