Sound Overall Performance in the First Half of 2016

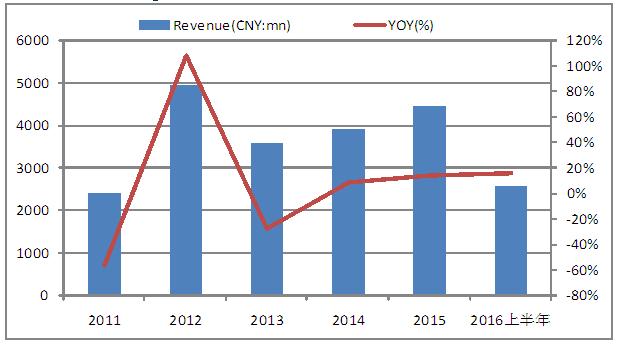

The revenue of the first half of 2016 achieved RMB2.556 billion with a year-on-year increase of 15.7%. The increase was mainly reflected by the 15% growth in orders at Q1 and Q2 trade fairs in 2016. The revenue of footwear and apparel increased by 19.1% and 8.6%, respectively, while that of accessories decreased by 43.6%. The proportion of footwear sales against the total annual revenue increased from 43.8% to 45.1%, which was mainly due to the stress on the development of footwear by the Company and the increase of footwear sales overseas.

Revenue Structure (CNY:mn)

Source: Bloomberg, Phillip Securities (HK) Research In terms of profitability, the gross profit was up to RMB1.06 billion with a Y-o-Y increase of 16.2%. The gross profit margin rose by 0.1% to 41.4%, wherein, the footwear business declined slightly by 0.3%, while those of other businesses increased. The net profit was RMB273 million with a Y-o-Y increase of 1.3%. EPS was RMB13.2 cents.

In terms of expenses, sales and distribution expenses were controlled better, wherein, the proportion of revenue was down by 0.6% Y-o-Y to 14.9%. However, the increase in administrative and financial expenses resulted in the increase of period cost ratio by 1.3% to 26.6% and followed by the decrease of the net profit margin by about 1.5% to 10.85%.

Revenue Growth performance

Source: Bloomberg, Phillip Securities (HK) Research Integration of Stores, Optimization of Retail Network

In the first half of 2016, the stores were less. 491 new stores were opened, while 846 existing ones were closed. Hence, the total number of stores is up to 6,853, decreased by 355 stores than the end of 2015. The stores were closed mainly due to urban planning and redevelopment and the influence of rainstorm in the southern part of China. 161 new junior clothing stores were opened, while 95 ones were closed. The total number of junior clothing stores reaches 2416, increased by 66 ones than the end of 2015. Some of the stores have been closed, which is beneficial for the improvement of efficiency and profitability of the other stores.

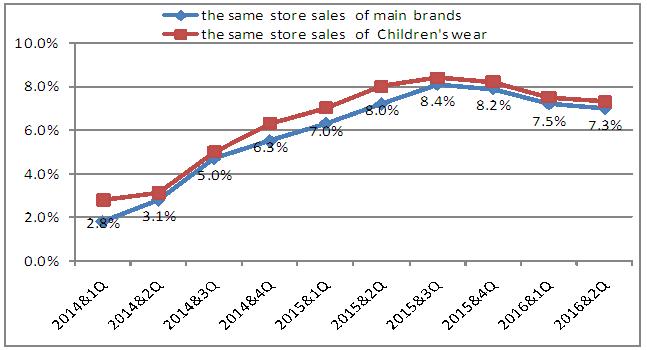

Growth of Same Store Sales Better than Peers

In Q1 and Q2 2016, the same store sales (SSS) of main brands grew by 7.2% and 7%, respectively. The SSS of 361 Degrees junior clothing stores increased by 7.5% and 7.3%, respectively. Though the month-on-month increase of SSS decreased slightly, its high single-digit increase was still better than peers. During the same period, Lining recorded a low + high single-digit SSS, while Xtep was low + moderate single-digit, and PEAK, flat + decrease.

Growth of Same Store Sales

Source: Bloomberg, Phillip Securities (HK) ResearchHigh Single-digit Growth of Orders at Trade Fairs

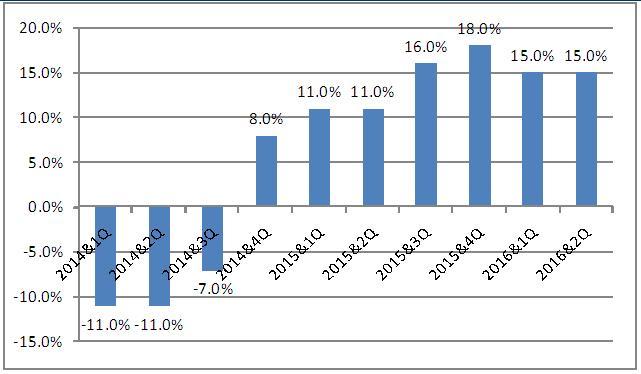

The main brand products of the Company in Q3, Q4 2016 and 2017 spring trade fairs recorded high single-digit growth, which had been improved for ten consecutive quarters. Junior brand products also recorded high single-digit growth at the trade fairs in the second half of 2016. The growth of main brand products at the trade fairs was mainly driven by the rise of quantity and price of footwear. The Company will continue to focus on footwear and promote sales accordingly.

Main brand: Growth of Orders at Trade Fairs

Source: Bloomberg, Phillip Securities (HK) ResearchValuation and Rating

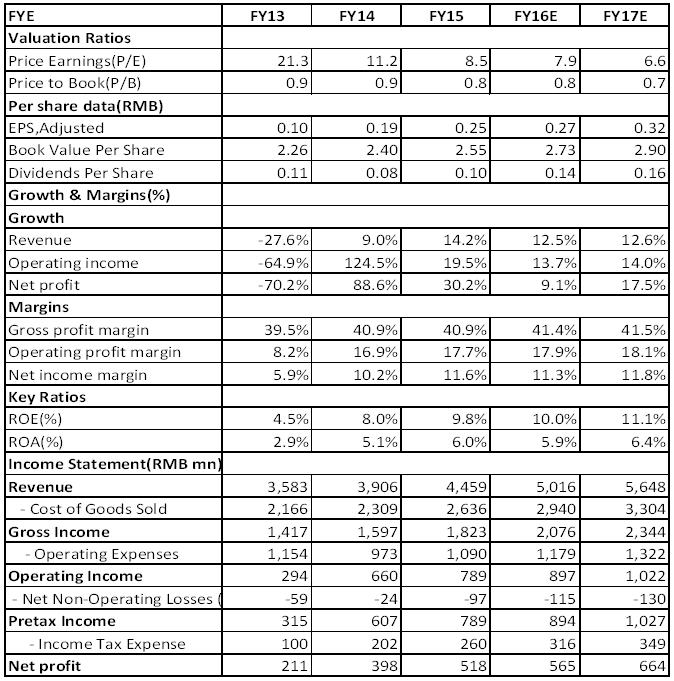

Overall speaking, the gradual recovery of the sporting goods industry is constructive for the long-term development of the businesses of the Company. The Company successfully sponsored 2016 Rio Olympics and Paralympics, which is expected to drive the significant improvement of overseas businesses for the whole year. In addition, 361 Degrees Kids and e-commerce may become important growth impetus in the future. We estimate that the EPS (earnings per share) of the Company in 2016 and 2017 will respectively be RMB 0.27 and RMB 0.32 and the target price is HKD 3.2, Also, the "Buy" rating is given. (Closing price at 24 August 2016)

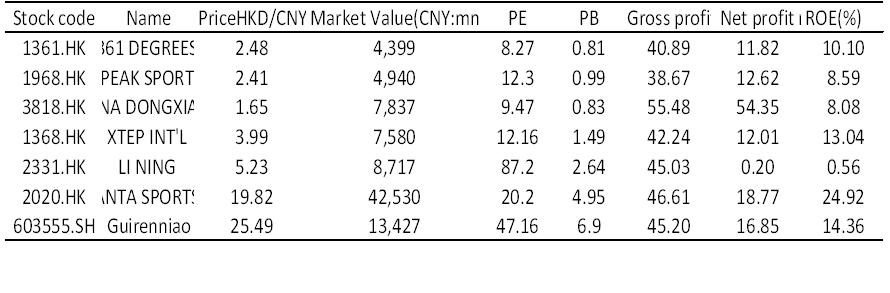

Peer comparison

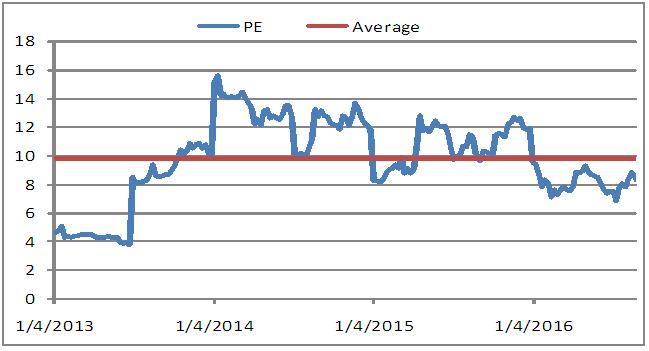

Source: Bloomberg, Phillip Securities (HK) ResearchBased on August 24, 2016 closing pricesHostorical P/E Valuation

Source: Bloomberg, Phillip Securities (HK) ResearchRisk Warnings

Downward in macroeconomic environment; Fierce market competition; Higher costs caused by marketing and promotion.

Financials

Source: Company, Phillip Securities (HK) Research Estimates(Financial figures as at 24 August 2016)Click Here for PDF format...