|

|

|

*Advertisement* |

|

|

|

|

|

24 Aug, 2016 (Wednesday) |

|

|

Yunnan Water(6839)

Analysis¡G

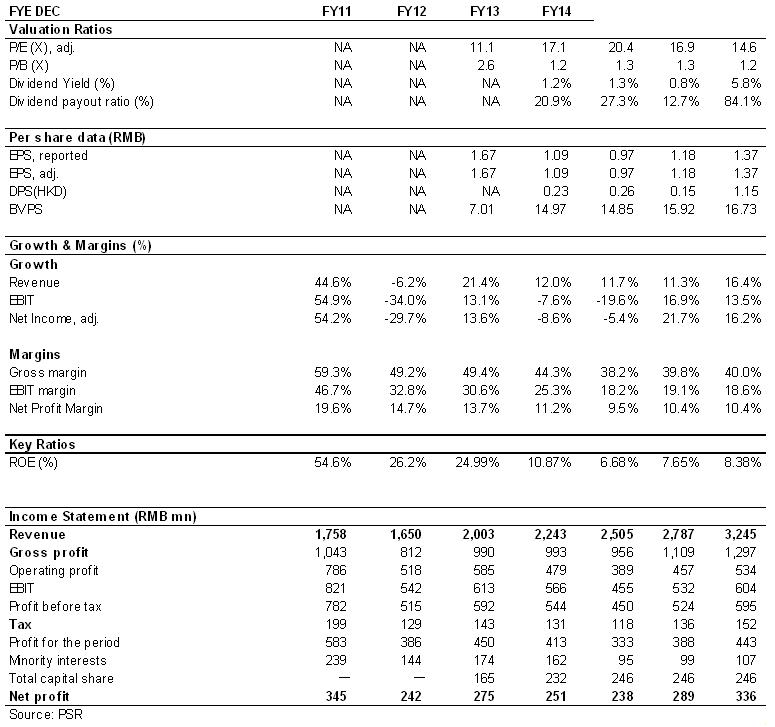

In 2015, the business revenue of Yunnan Water reached RMB1.56 billion, up by 41.6% as compared to 2014. Major contribution came from several businesses, including: The sewage treatment business achieved 9.5% growth and reached RMB420 million thanks to the fact that some sewage treatment facilities raised their service unit price and that some previously acquired projects of sewage treatment facility generated profits; water supply business went up by 110.5% to RMB450 million, due to profits generated by previously acquired projects; construction and equipment sales business grew by 27%, amounting to RMB600 million. In 2015, the company, for the first time, extended to solid waste treatment business through the acquisition of Ningde and Fu`an waste-to-power projects, as well as hazardous waste projects like Shandong Tengyue and Zhengxiao Environmental Protection. Yunnan Water will continue to carry out mergers and acquisitions and strategic cooperation, speeding up the layout in water and solid waste treatment business. Its core strengths lie in its sophisticated membrane technology and rich experience in the PPP model. We give the company 12-month target price of HK$5.70, equivalent to 14 X 2016EPS.

Strategy¡G

Buy-in Price: $4.5, target Price: $5.7, Cut Loss Price: $3.75

|

| |

|

Poly Culture (3636.HK)-Recovery of the Auction Business

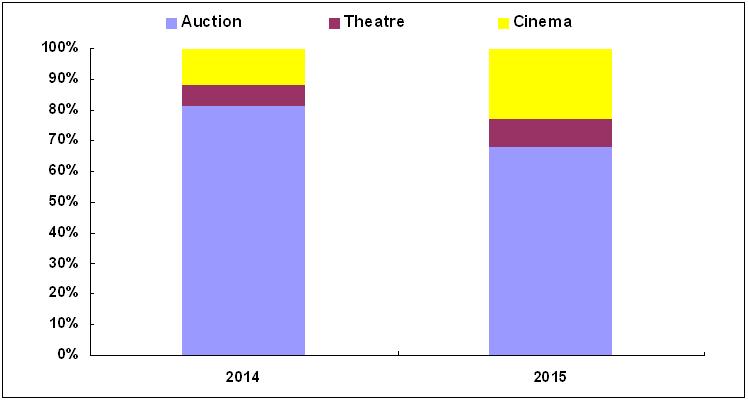

2016H1 Profit expected to grow by 60%-80%Poly Culture recently made a positive announcement and estimated that as of the end of June, the company is expected to see a 60% to 80% YoY increase in net profit in 2016H1. As the net profit recorded for 2015H1 was approximately RMB 71 million and the one for 2014H1 was RMB 123 million, the profit for 2016H1 is estimated to be between RMB 100 million to RMB 130 million, close to that in 2014H1. This significant increase is mainly attributable to the fact that the settlement progress of artworks auction business is on the turn compared to the same period of the previous year. Affected by the settlement progress, the company's performance in 2015 presented a from-down-to-up trend, with the EPS for the first and latter halves of the year being RMB 0.29 and RMB 0.68, respectively. Fluctuations were also seen in gross profit margin because of the changes in business structure. For the first and latter halves of the year, it was 33.8% and 41.4%, respectively. Recovery of the Auction BusinessOne of the company's major businesses, auction, is seeing recovery in recent days. Total sales on the 2016 Poly spring auction achieved good results, with the sales on Poly spring auction in Beijing and Hong Kong reaching RMB 2.85 billion and RMB 1.27 billion, respectively. Further increase was also seen in the company's share in the domestic market. Fu Baoshi's `God of Cloud and Great Lord of Fate`, among them, set a new record with a winning bid of RMB 230 million, showing a strong demand on the high-end market. We believe that this recovery in the auction, with its high gross profits, will help enhance the company's performance and profitability. Active Promotion of New BusinessesOn the basis of the three major culture & media businesses, the company is working actively to explore and develop new business models in such service sectors as education, finance and tourism, which is worth noting in the future.As for art education, the company established Beijing Poly Music Art in 2015 and officially launched the Poly Music Education Project with a strategic cooperation with Central Conservatory of Music. Its first school has started the student enrolment work. Poly Music Education Project represents the first attempt of the company to combine culture with education, and for the next step, the company plans to expand such integrative development to performance art, visual art, artwork appreciation and practice to consolidate and establish a unified brand of "Poly Culture and Art Academy", aiming to become the most influential comprehensive art education platform in China.As for cultural finance, the company's artworks financial services business will officially begin operating shortly. In 2015, Poly Culture's subsidiary in Hong Kong was granted the Money Lenders Licence. Meanwhile, in order to facilitate the company to leap forward in cultural financing, the company is duly studying the issue of establishing Poly Cultural Industry Fund, and intending to collaborate with relative professional institutes to bring in capital from the society, absorb art industry resources, and carry out project investment as well as entrepreneur mergers and acquisitions cross various cultural areas.Apart from the aforesaid, riding on its own brand advantages, the company will actively explore the development of innovation and integration of culture industry into tourism and other industries. We believe that these active efforts to integrate supporting industries on the basis of its brand advantages could create new business models and stimulate business profit growth points in the future. Investment ThesisFor the latest financial estimate, we accordingly gave the target price to HK$23.5, respectively 1.3/1.2x P/B for 2016/2017. "Accumulate" rating. RiskArtwork has the qualities of luxury and may be affected by economic downturn and fight against corruption. Due to the relatively intense competition of domestic theatres and cinemas business, the popularity of the products launched is greatly affected by contingency factors. Main profit breakdown

Source: Company, Phillip Securities Hong Kong ResearchFinancials

(Financial figures as at 22 August 2016)Click Here for PDF format...

| Recommendation on 24-8-2016 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 19.840 | | Suggested purchase price | N/A | | Target Price | $ 23.500 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

| Phillip Research - Hong Kong ½÷¥ß¬ã¨s³¡ ¡V »´ä¤Î¤¤°ê |

| Company |

Stock Code |

Last Update |

Suggestion |

Target Price |

Price on Recom |

| | 2333 | 18/08/2016 | Accumulate | 9.24 | 8.13 | | GWM | 2333 | 17/08/2016 | Accumulate | 9.24 | 8.13 | | | | Wisdom Sports Group | 1661 | 11/07/2016 | Buy | 3.3 | 2.18 | | NetDragon | 777 | 16/06/2016 | Buy | 28.4 | 22.9 | | | Jumpcan Pharma | 600566 | 19/08/2016 | Accumulate | 34.3 | 28.97 | | Fosun Pharma | 2196 | 16/08/2016 | Buy | 23.6 | 19 | | | Shanghai Haohai Biological Technology | 6826 | 06/06/2016 | Buy | 48.18 | 39.55 | | Hengrui Medicine | 600276 | 10/05/2016 | BUY | 56.5 | 46.92 | | | Yunnan Water | 6839 | 23/05/2016 | Buy | 5.7 | 3.94 | | Grandblue ENV | 600323 | 20/04/2016 | Buy | 17.5 | 13.11 | | | Poly Culture | 3636 | 24/08/2016 | Accumulate | 23.50 | 0.000 | | Peak Sport | 1968 | 13/05/2016 | Buy | 2.25 | 1.83 | | | Byaa Interactive | 434 | 05/07/2016 | Accumulate | 3 | 2.71 | | Kingsoft Corporation Limited | 3888 | 28/06/2016 | Buy | 19.1 | 14.86 | | | Fortune REIT | 778 | 23/08/2016 | No Rating | | 9.65 | | Fortune REIT | 778 | 22/08/2016 | No Rating | | 9.65 | | | Jingneng Clean Energy | 579 | 12/08/2016 | Buy | 3.2 | 2.44 | | Canvest Environmental Protection Group Co., Ltd. | 1381 | 21/07/2016 | Buy | 4.7 | 3.4 | | | Goldpac Group | 3315 | 18/02/2015 | N/A | | 4.77 | | IGG | 8002 | 21/11/2014 | Accumulate | 3.95 | 3.44 | | | Jinjiang Hotels | 2006 | 08/07/2016 | Accumulate | 2.98 | 2.49 | | CUTC | 600358 | 08/03/2016 | N/A | | 10.41 |

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2016 Phillip Securities (HK) Ltd. All Rights Reserved.

|