Results in Q1 Fell Short of Expectation

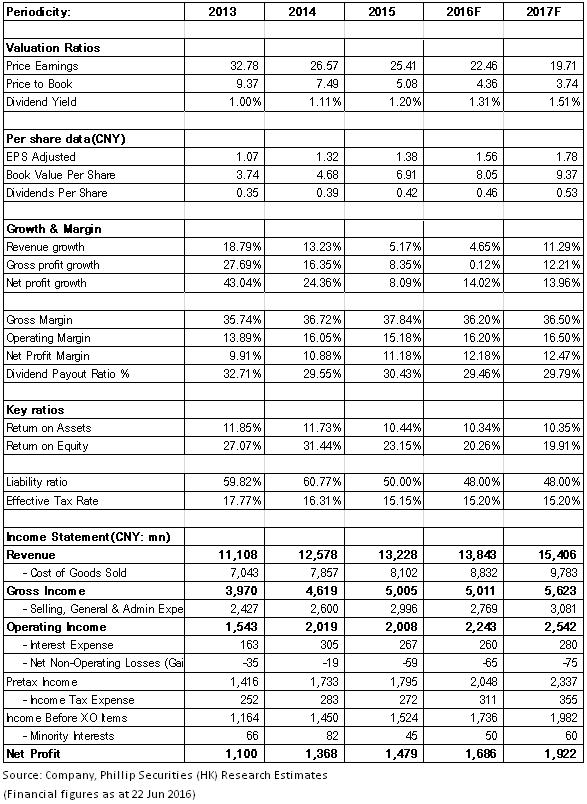

In Q1 2016, Tasly recorded a revenue of RMB3.15 billion, up 2.3% year-on-year; net profit excluding non-recurring items was RMB270 million, representing a YoY decrease of 19.3%, which was lower than estimate.

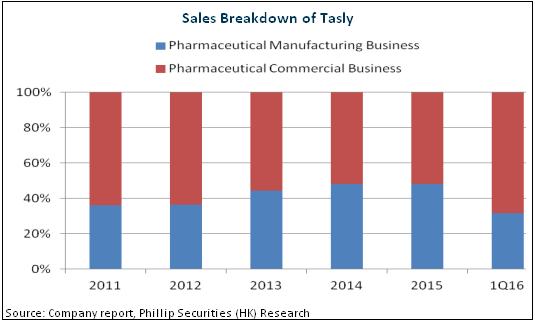

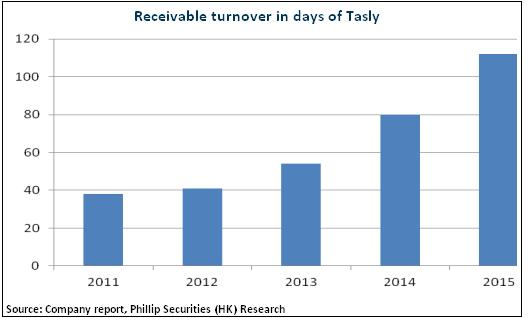

Despite a significant increase of 34.2% in the pharmaceutical commercial revenue, the pharmaceutical manufacturing business revenue decreased by 28.90%, which was probably affected by bidding price drop and medical expenditure control. In addition, in order to adapt to new policies including the two-invoice system, the company enhanced management of accounts receivable, which also burdened the growth of pharmaceutical manufacturing revenue. From 2011 to 2015, the company has extended the accounts receivable turnover from 38 days to 112 days.

In terms of profitability, despite a decrease of 6.4% in opex ratio due to change in sales breakdown, it failed to set off the decline of gross profit margin by 9.1%, leading to the slump of performance. However, the control over the accounts receivable improved the collection of accounts receivable, and net operating cash flow increased by RMB162 million, or 657.6%. The debt-to-asset ratio fell from 50% to 48%.

Short-term Performance Decline Would Not Affect Long-term competitiveness

In the short term, enhanced management of accounts receivable by the company will create negative effect on the business development. However, the company relentless insists on the principle of "Big market, big terminal, big category, big brand and wide coverage", and gives a full play to the advantages of Compound Danshen Dripping Pills (CSDP) as a low-price, essential drug. The product is expected to keep its competitiveness in the long term by expanding market shares in the counties and grass-root communities.

The FDA phase III clinical trial of Compound Danshen Dripping Pills has been completed in March. It is expected to be approved by FDA in 2017 and become the first Chinese patent drug present in American market. It would not only be a milestone event for the internationalization of traditional Chinese medicine (TCM), but also a star product for the company which features long-term safety and low tolerance. And it is expected to embrace a third round of rapid growth.

Furthermore, the achievements the company has made in international drug administration regulations, research application and marketing have paved way for the development of the company's subsequent products. In the meantime, the company is offering international CRO services for companies under the Traditional Chinese Medicine Association. At present, the company has begun strategic partnership with Guangdong Taiantang, Yiling Pharmaceutical, Guizhou Bailing. The long-term cooperation with these companies in FDA certification of their products demonstrates the leading role of the company in the international TCM market.

Valuation

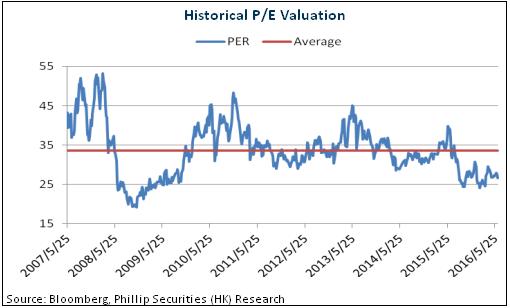

In conclusion, the company, as one of the leading international TCM enterprises, bears operating pressure in the short term. However, obtaining the overseas certification for CSDP is highly possible, and is also a major event in the industry as well as a significant catalyst for the company. Besides, sound product portfolio and exceptional channeling capacity will fuel the company's growth. On top of it, its external M&A is also something we can look forward to. We give an estimation of 30x EPS in 2016 and the target price is RMB46.8. Also, the "Buy" rating is maintained. (Closing price as at 22 Jun 2016)

Risks

Drop of main products;

Slowdown of the internationalization process of Compound Danshen Dripping Pills;

Marketing of new product falls short of expectation.

Financials

Click Here for PDF format...